With summer finally in full swing and the English weather back to normal we have a bumper edition of Payments View with both the July and August updates. If any of the below topics spark further questions, please don’t hesitate to reach out to us.

The Past and Future of Money: BoE and PSR

In case you have already jetted off on holiday accidentally forgetting your book, we wanted to kick off this edition with two interesting speeches from the BoE and PSR with both pondering on the past, present and future of money. If Kierkegaard, crypto and the foundations of safe money are your thing, then we’d recommend Andrew Bailey’s musings ‘New prospects for money’ as our suggested pool-side reading. For those who are looking for a brief history of payments then why not try James Jamieson’s speech on the changing nature of payments, which helpfully answers that crucial question of who paid for Lord Byron’s holidays…

The UK Regulatory Landscape: from Edinburgh Reforms to Mansion House

The end of last month saw the long-awaited Financial Services and Markets Bill achieving Royal Assent as the Financial Services and Markets Act 2023 (“FSMA 2023”). FSMA 2023 is one of the first main steps in the Edinburgh Reforms establishing the framework for the revocation of retained EU law, adding new objectives for regulators, and moving closer to certain stablecoins falling within the UK regulatory perimeter.

The Chancellor delivered his speech at Mansion House updating on the government’s work on improving the competitiveness of the UK financial sector. Here, HMT’s programme is intending to deliver a ‘smarter regulatory framework’ to tailor the UK position to a post-Brexit world. For those wanting more detail on future developments, see also the HMT delivery plan which sets out interesting points on the ‘new balance’ between the Government and regulators, the proposed “targeted policy changes”, as well as next steps on developments for Consumer Information Requirements in Payment Account Regulation and the continued reform of the PSRs (covered in the January edition of Payments View with the first round of ‘targeted reforms’ proposed by the end of 2023).

Of particular interest is the announcement of the Future of Payments Review 2023: Call for Input which considers “how payments are likely to be made in the future and [to] make recommendations on the steps needed to successfully deliver world leading retail payments.” This call for input will run until 1 September, following which the Chair (Joe Garner, former Nationwide Building Society CEO) will publish a report and a set of recommendations to the government. Respondents can provide input through the online response form. The PSR has put out a statement welcoming the Call for Input and highlighting the importance it sees in its work on APP fraud (see also below) in addressing this. The scope of the Call for Input is focused on the needs of modern consumers and asks, in extraordinarily succinct fashion:

- What are the most important consumer retail payment journeys both today and in the next 5 years? For example, paying a friend, paying a bill, paying businesses for goods and services, in the UK or internationally etc.

- For these journeys today, how does the UK consumer experience for individuals and businesses compare versus other leading countries? For example, the quality of experience, security or cost.

- Looking at the in-flight plans and initiatives across the payments landscape, how likely are they to deliver world leading payment journeys for UK consumers? For example, we welcome suggestions that you feel would support, or are essential to delivering, world leading payments for UK consumers.

Consultation Response to Reforming the CCA 1974: in short, everyone wants it fixed

To the surprise of absolutely nobody, the response to HMT's consultation on reforming the Consumer Credit Act 1974 ("CCA") reflects that much needed change is required and can be expected over the coming years to this area of UK regulation.

A key message of the response is that modernisation is needed to not only the form of the legislation (with proposals for it moving from legislation to the FCA handbook), but also its scope and the underlying concepts and definitions. That the CCA is noted as "increasingly under strain to deliver a 21st century customer experience" is unsurprising and the proposed reform (based on the principles of being "proportionate, aligned, forward-looking, deliverable and simplified") has been widely supported by respondents. Particularly interesting highlights from the responses include that:

- Many industry stakeholders argued that unenforceability should be removed (as a penalty / enforcement mechanism) and not replicated in FCA rules, instead suggesting that the FCA's enforcement powers and other routes to redress - such as through the FOS - provide adequate sanction and deterrence against malpractice;

- Most respondents argued that changes to definitions would help to achieve a more future-proofed regime that can better facilitate innovation and adapt to emerging products - with the distinction between Fixed Sum / Running Accounts and definitions relating to 'credit tokens' all being highlighted as a prime area for modernisation; and

- A number of stakeholders argued that the existing scope set out in the CCA relating to regulation of SME business lending should be reduced - not a view shared by certain policy makers and we expect to see more on this from industry later in the year.

The government plans to develop proposals that move the majority of the CCA into the 'FSMA model' which will involve repealing much of the CCA and recasting it in the FCA handbook. However, the Government notes that there may be specific aspects of consumer credit regulation that may warrant legislative-based provisions and that it is currently difficult to provide a specific timeline for any of these changes, considering their scope and interconnected nature. As a next step, the Government proposes to publish a second stage consultation in 2024 which we will keep a watching brief on here at Payments View.

Interestingly, the proposed reform of BNPL (covered in the February edition and one of the more advanced proposed reforms in the space) is barely mentioned in the consultation response - whether this adds any credence to the rumours of this reform being dropped is an interesting question.

Regulator Updates: new Regulatory Initiatives Grid and PSR Annual Report

Following the Royal Assent of the FSMA 2023, the Regulatory Initiatives Grid has been updated to account for this change in the regulatory frameworks, as well as the regulators' new secondary objectives. In particular:

- The FCA, PRA, BoE and PSR are already taking steps to operationalise changes to reflect new obligations and accountability mechanisms introduced by FSMA 2023.

- The PRA intends to publish a consultation paper focused on its new objectives under FSMA 2023, which will build on the September 2022 discussion paper on approach to policy.

- An FCA consultation on access to cash and a BoE consultation on the wholesale access to cash regime will be published in autumn 2023.

- The FCA and the PRA are also establishing new cost benefit analysis panels.

If you wanted similar reading, we would also point you towards the latest annual report from the PSR, which notes the positive steps by the regulator in respect of the commitments set out in its2022/23 annual plan.

APP Fraud and Quincecare Duty Updates

It has been another busy month for the PSR on one of their core regulatory developments - addressing APP frauds and implementing the mandatory reimbursement requirement to fight them. The latest development is a consultation paper (CP23/4) on the legal instruments that will implement this reimbursement requirement, which we have commented on at length.

The CP specifically covers two of the three legal instruments - a specific requirement under section 55 of the Financial Services (Banking Reform) Act 2013 and a specific direction to Pay.UK under section 54 with a further consultation on the general direction on PSPs planned for October 2023. This consultation closes on 25 August 2023.

These legal instruments will implement the policy within Faster Payments, noting that the BoE has also announced its intention that similar reimbursement requirements should apply to CHAPS following pressure from MPs. A key change to the June policy statement is that all three legal instruments are intended to be finalised in December 2023 (again following pressure from MPs) with a proposed implementation date of 2 April 2024 that the PSR acknowledges is "likely to be a challenging target for firms'. Therefore, the revised timing is:

- In August the PSR will consult on the maximum level of reimbursement and claim excess and additional guidance on the customer standard of caution (gross negligence).

- In October, the PSR will consult on the draft general direction which will be given to all payment firms, requiring reimbursement for APP scams victims.

- By the end of 2023 the PSR will publish the claim excess and maximum level of reimbursement, additional guidance on the customer standard of caution (gross negligence) and all legal instruments.

- In 2024 the new reimbursement requirement will come into force.

The consultation paper comes as the Supreme Court provides some much needed clarity on the scope of the Quincecare Duty in the case of Philipp v Barclays Bank UK plc [2023] UKSC 25 in which the claimant alleged that the bank owed her a duty under contract or at common law not to carry out her payment instructions, if the bank had reasonable grounds for believing that she was being defrauded.

In an outcome that will be welcome to banks, the court confirmed that the Quincecare Duty does not extend to APP and related scams where the customer is a natural person, rather than a corporate acting through its agents.

In response to the judgement, we hosted a 20 minute on demand webinar covering:

- Key take-aways from the Philipp judgment;

- How these interact with the introduction of mandatory reimbursement for APP fraud;

- The impact of the proposed criminal offence of failure to prevent fraud; and

- What this means in practice for banks and their customers.

HMT Statement on Freedom of Expression: account closures

Following the high profile coverage of recent bank account closures, HMT have announced measures to mitigate the potential harm caused by this in future.

Rushing forward a response to Government's statutory review of the PSR 2017 (which we covered back in January) the statement notes that most respondents felt that the current framework worked well in its current form (striking an appropriate balance between the rights of their users and account providers' capacity to manage their commercial risk freely) and that the Call for Evidence did not provide definitive evidence to confirm the suggestion that accounts were being closed for political reasons. Nevertheless, HMT intends to amend the PSRs (building on responses from "several respondents who considered they had been subject to unclear contract terminations") to require payment account providers to:

- Provide a clear and tailored explanation to a customer where their payment account contract has been terminated, except when doing so would be unlawful; and

- Provide at least 90 days' notice (up from 30) when choosing to terminate a contract, unless for a serious and uncorrected breach, such as non-payment, or other serious occurrence (noting that terms which allow termination for other matters, such as brand protection, cannot be used to "circumvent" this). Shorter termination periods will still be allowed in certain circumstances, such as where a provider is required to terminate the contract to comply with financial crime obligations.

HMT also notes concerns (unnamed and uncorroborated in this response document) that the requirements in the MLRs 2017 relating to politically exposed persons ("PEP") are being "applied disproportionately by some financial institutions" emphasising that the MLRs 2017 do not provide grounds for account closure on the basis of political views and that a consumer being a domestic PEP should not be the basis for firms refusing to provide banking services in the absence of other risk factors. The FCA is currently undertaking a review of its guidance on PEPs to clarify expectations concerning domestic PEPs.

We have recorded two podcasts on this subject which can be found here: DSARs and Debanking and Debunking Debanking.

Amendment to EMRs and PSRs to Address Post-FSMA 2023 Regulator Powers

The Electronic Money, Payment Card Interchange Fee and Payment Services (Amendment) Regulations 2023 was published this month to remove a limitation on the FCA's power to make rules in relation to EMIs, APIs and RAISPs.

Amendments also extended the FCA's existing powers to make rules for authorised persons in relation to client money, the control of information, and the appointment of auditors to these institutions, apply the Treasury's power to make recommendations to the FCA in connection with its general duties to the FCA's duties in relation to EMIs and APIs and require the FCA to have regard to the net zero emissions target as one of the regulatory principles applying to the exercise of its functions under the EMRs and PSRs - because the FCA just doesn't have enough on at the minute.

Stakeholder Input on UK-EEA Cross-Border Interchange Fee Increase

The PSR have published a summary working paper and stakeholder responses in respect of its ongoing work on UK-EEA cross border interchange fee increases. Interestingly, but not substantiated, multiple respondents considered there to be "no real rationale" for the substantial increase in interchange fees, while others proposed that fee increases provided greater incentives to attract issuers to the Mastercard and Visa schemes (against whom they could charge higher scheme and processing fees). One respondent went so far as to note that, in the absence of a cost justification, increasing IFs suggested that Mastercard and Visa potentially have anti-competitive agreements and the increases are representative of unfair pricing abuses.

More broadly, the PSR noted comments that UK to rest of the world payments may also require monitoring, and that recommended interventions included:

- Capping the fee at 0.2% and 0.3% to mirror the EU cap;

- Temporarily capping the fee to previous levels while a market review is conducted; and

- Encouraging interventions that boost competition and encouraging alternative methods for cross-border payments.

The PSR review is ongoing. The plans to publish a report setting out its interim conclusions later in 2023, and a final report before the end of the year.

Pay.UK Publishes Consultation Response on the Digital Pound

Pay.UK have published their response to the Call for Evidence on the proposed digital pound (this consultation being covered in detail in a specialFebruary edition) which makes for interesting reading in light of their position as the recognised operator and standards body for the UK's retail interbank payment systems.

The response is broadly positive towards the core points of the proposed approach to a UK CBDC - approving of the suggestions that: all holders have a direct claim on the BoE in the same way that they do for physical cash; that the privacy and data aspects would be roughly similar to those of commercial bank money used in card and interbank payments; and the BoE's conclusion that a single central ledger is likely to be the most appropriate design. The standards body does, however, highlight the following interesting, practical considerations where they believe further detail would be required, including work on:

- The degree of consumer protections, including who would set and enforce these;

- The funding model, including how the Bank and PIPs would fund the digital pound payment system in a way which is sufficient and not anti-competitive;

- The liability model, including the extent of the Bank's liabilities and accountabilities and how this would interact with liabilities in the realm of commercial bank money;

- The framework for regulating PIPs and ESIPs (in particular from a conduct perspective); and

- The extent to which the Bank could deliver relevant core services itself or would depend on third parties.

This comes as the CBDC consultation itself has reportedly received more than 50,000 responses, with the Telegraph highlighting the "huge public backlash" which the proposal appears to have generated.

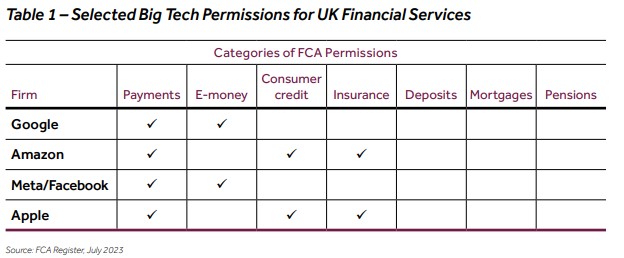

Big Tech in Financial Services - the FCA's thoughts

The FCA have published a feedback statement(FS23/4) on its discussion paper (which we covered in the November edition of Payments View) on the competition impacts of Big Tech in four retail sectors: payments, deposit taking, consumer credit and insurance. The statement makes interesting reading and, whilst at this stage does not propose any regulatory or policy change, does confirm that the FCA will issue a Call for Input on Big Tech firms as "gatekeepers" including the role of data asymmetry between Big Tech firms and financial services firms.

The FCA also intends to both review their approach to supervision of these firms and to work more closely with the Government and Digital Markets Unit to promote a pro-competition regime for digital markets.

The statement also includes a number of interesting commercial notes on the growing influence of these firms in financial services, including setting out selected Big Tech presence in the differing sectors of the industry - as set out below and at Appendix 1.

This ties in with speeches by the FCA (covering their regulatory approach to Big Tech as well as AI) and the EBA who focus specifically on AI in financial services. The FCA outlines the key findings of the above response and, in respect of AI, warns that using AI can cause imbalances and risks affecting the integrity, price discovery, transparency and fairness of markets. The FCA expects firms to accelerate investment in fraud prevention and operational and cyber resilience as AI is further adopted, but intends to open its upcoming AI sandbox to firms wanting to test the latest innovations. Whereas the EBA focused on MiCA post-implementation and that in addition to monitoring the uptake of innovative AI and machine learning (ML) techniques in financial sector use cases (including generative AI), the EBA is focusing on the use of AI for creditworthiness assessments (which the EBA expects this use case to be classified as a "high-risk" AI system).

BoE Speech on New Framework for RTGS

And from big tech to better tech, where the BoE have published a speech given by Victoria Cleland (Executive Director for Banking, Payments and Innovation) on the benefits of the new framework for the Real-Time Gross Settlement ("RTGS").

The speech sets out what the BoE sees as:

- The first phase of benefits in ISO 20022;

- The second phase of benefits in the new core settlement engine; and

- Foundations for the future, where new ways to connect to RTGS, a synchronisation interface to connect RTGS with other ledgers, and extended RTGS operating hours are all top of the list.

Payment Account Regulations, information requirements to change Jan 2024

Following on from its December 2022 consultation, HMT have published a response on Part 2 of, and Schedules 1 and 2 to, the Payment Account Regulations ("PARs"). These set out requirements for UK payment service providers who offer payment accounts to provide their personal customers with certain documents related to their account fees: the fee information document and the statement of fees, the requirements for which will be removed as HMT confirm that this will *"have a limited negative impact, and potential risks are mitigated by other rules to which industry is subject"*.

As we noted when we covered the consultation in the December edition of Payments View, whilst this aligns with the government's wider approach to delivering a smarter, more UK-centric regulatory framework, firms will still need to consider how any changes or a perceived move away from being transparent with customers will be viewed by the FCA in light of the Consumer Duty. The changes will be implemented through secondary legislation. The changes will take effect on 1 January 2024, handing over responsibility for detailed firm-facing customer information requirements to the FCA.

PSR Horizon Scanning

Last but not least, the PSR has published a speech on its horizon scanning work.

The speech notes that horizon scanning is vital to achieving the PSR's ambitions (and indeed, the latest PSR Board Meeting minutes from 17 May 2023 discuss the importance of this work) and highlights account-to-account (A2A) transactions, Web 3.0 and AI as particular areas of interest where the regulator can "identify and work with all stakeholders to understand the potential challenges and make sure there are no barriers to innovation"

News Flash

- The FCA has confirmed that the Digital Sandbox (its testing environment that enables us to support firms at the early stage of product development by enabling experimentation through proof of concepts) has been made permanent.

- More detail from the FOS on the Consumer Duty with a speech from Abby Thomas (FOS Chief Executive and Chief Ombudsman) building on the detail the body published last month (covered by Payments View) on what the regulatory change means for resolving complaints.

- More on the Consumer Duty, with the FCA highlighting via its Financial Lives survey the increasing number of people using digital banking and payments and how this impacts the FCA's expectations of firms in order to comply with the Consumer Duty.

- UK Finance has published a retrospective on Strong Customer Authentication 18 months on.

- The FCA published an updated version of its webpage on the perimeter report.

- The European Parliament's Economic and Monetary Affairs Committee (ECON) has published the report it has adopted on the European Commission's legislative proposal for a proposed Regulation amending the Single Euro Payments Area Regulation (260/2012) (SEPA Migration Regulation) and the Cross-Border Payments Regulation ((EU) 2021/1230) as regards instant credit transfers in euro.

- And if any readers were interested in taking on a new challenge, the PSR is hiring for a new Chair. https://www.psr.org.uk/media/yqhhgfk5/psr-panel-chair-advertisement-2023.pdf

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)