A major function of financial markets is to price the prospects for future growth and risk. Since the nadir in March of global equity markets, investors appear to have judged that TMT in general and Technology in particular are in the vanguard of hopes for improved pandemic resilience in the post-COVID New Normal; investors appear accordingly to have concluded that TMT growth prospects outweigh their inevitable associated risks. This note looks briefly into the supporting evidence for that confidence from macro-economic and geopolitical issues to the societal challenges posed by the onset of and response to COVID-19. Our Horizon Scan of the New Normal suggests its landscape will need to feature rapid vaccine development, effective test/ trace/ isolate protocols and more remote working as well as the mitigation of environmental degradation. All of those are data/ technology heavy.

Market view

Global investors appear to believe that the TMT sectors have a bright future. After initial sharp falls, as the first wave of the pandemic broke across the world in January, the tech-heavy Nasdaq has (by early-July) recovered 125% of its initial losses and risen to new all-time highs.

By contrast the global equity benchmark has recovered only 77% of its initial losses and the headline indices of most major western countries have underperformed even that, with investor concerns focused on the success or otherwise of local efforts safely to relax lockdowns.

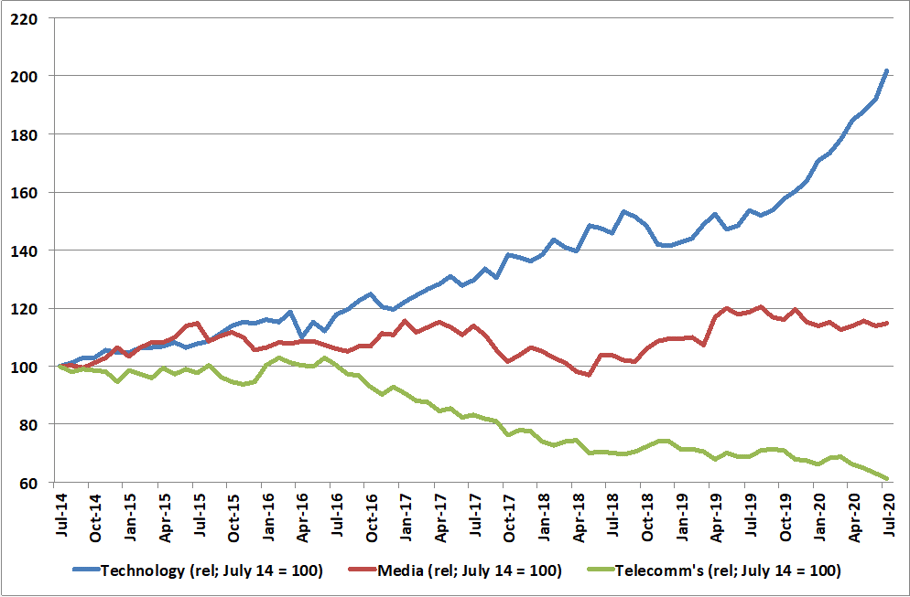

Chart 1: The performance of TMT equity sub-sectors relative to the global average

But the devil, or at least the nuancing, is in the detail. Not all TMT is created equal: the chart above shows the longer-term trends (since 2014) in the performance of the global TMT sub-sectors relative to (rel) the global average of all equities. The contrast between the two-fold outperformance of the Technology sub-sector and the 40% under-performance of the telecommunications sub-sector is stark.

Economic Outlook

The consensus view so far is for a 'V-shaped' recovery in global GDP with its nadir around Q2/Q3 of this year followed by recovery so that by the end of 2021 global GDP has recovered most if not all of its level at the end of 2019.

But that same consensus hides wide regional variations: China and other 'emerging economies' are expected to outperform their western developed counterparts by some margin. The IMF forecasts for example suggest a gap of some 7 percentage points of GDP growth between emerging (EM) and developed (DM) economies.

That regional gap suggests potentially increasing trade tensions between the two blocs that could in turn increase moves to shorten supply chains by on-shoring or re-shoring especially the manufacture of critical items for the Technology and Telecommunications sectors.

Horizon Scanning the New Normal

We recently published our Horizon Scan of the New Normal. The resulting scenario analysis highlighted two particular areas of focus that have resonated strongly with clients to whom we have presented its findings.

In the immediate term are the challenges around managing the safe return to the workplace and in the longer term the elements which flow from the single greatest imperative: the world simply cannot afford another pandemic - cannot afford for this black swan to become a flock.

Safe return and the future of work

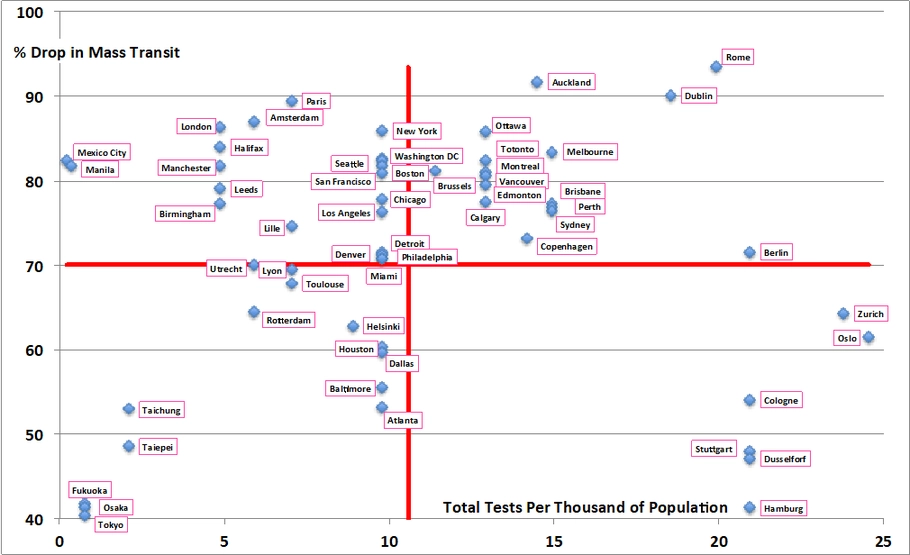

The degree of challenge in effecting a safe return to the workplace is made stark in work we did for the Horizon Scan, cross-referencing data for the integrity of lockdowns in different cities around the world with data for the degree of COVID testing in different countries.

Both elements, charted below, rely on huge volumes of data: the degree of lockdown from Apple/ Google showing changes in the number of requests for travel directions using their 'map apps' and the testing data relying on public health sources or self-reporting apps.

Chart 2: Lockdown integrity versus COVID testing protocol

Those countries which 'do well' on both counts (the top right quadrant in the chart) are those where relaxing lockdown might be viewed with greater confidence in the chances of avoiding a serious further outbreak.

This note is not the place to elaborate the findings of that exercise - simply to make the point that relaxing lockdowns safely, as being attempted in Europe, or maintaining no lockdown as in parts of Asia relies heavily on data to allow more localised responses to the almost inevitable but local further outbreaks.

Such heavy reliance on data and the algorithms/ AI systems to process it raises obvious legal and policy questions around data privacy. Could authorities find cause in preparation for or in response to a future pandemic to water down or implement a temporary suspension of privacy safeguards?

As for the future of work the most likely outcome from COVID-19 is that remote working becomes more commonplace, increasing the demand for all aspects of remote access including video-conferencing, e-signatures, broadband, distributed data and its security.

Pandemic resilience - how and who pays?

The TMT sectors, especially Technology, will be in the vanguard of the efforts to stop the COVID black swan becoming a flock. Artificial Intelligence will undoubtedly feature at the intersection between Technology and Life Sciences in the rapid and agile development of new vaccines, raising questions along the way around IP if vaccines themselves are to be treated as a 'common good'.

In the short term public-private partnerships in development of track and trace may offer the best defence against a full-blown second wave or a storm of rolling local lockdowns as the summer rolls into the winter influenza season.

Increasing pandemic resilience will also require addressing the loss of biodiversity (one of the main risk factors seen by business leaders at Davos earlier this year and that includes tackling deforestation and other encroachment on natural habitats. Geospatial data will be vital to ensure compliance.

The pandemic has also revealed the greater susceptibility of lower income groups, fuelling the debate around income inequality. Again this note is not the place to elaborate on that vast topic. But governments around the world will be looking at some point to reduce the hugely increased levels of national debt. Given OECD initiatives last year to find ways to increase national-level tax yields from global technology companies, it seems possible that TMT sectors will be in the vanguard of this move also and so play a part in a possible change to a more redistributive role for tax policy.

At a more domestic level the digital infrastructure gaps which have been laid bare by the pandemic, mapping neatly onto areas of high deprivation, are likely to be in the target zone for public policy in the New Normal. Not simply the ease of doing a Zoom call on a copper cable, but rather the life chances of thousands of children in regions or demographics with limited access to such facility.

Geopolitics

There are important policy choices ahead that will determine the pace and direction of some of the societal changes we have headlined here. The US Presidential election later this year may prove pivotal: if President Trump wins a second term the policy direction may focus more on an earlier reduction in national debt through some variation of the austerity era which followed the global financial crisis (GFC), and on the regional gap between the expected GDP growth in EM and DM economies we spoke of earlier. That in turn could feed further into the pre-COVID trends pushing back on globalisation as nationalist political agendas become more widespread.

If Mr. Biden wins in November then it may be that the focus would be greater on stimulating the economy further through major infrastructure investment and on improving pandemic resilience as we described earlier - possibly funded by something akin to a post-COVID 'war bond'.

Sitting across both of those policy agendas is the elephant that's been in the room since the GFC - the stagnation of productivity. In the 10 years prior to 2010, GDP per hour worked across the OECD grew by some 16%; in the subsequent 10 years it grew by less than half that. The jury remains out on why that gap has developed. But Technology, properly harnessed, is likely to play a major role in its solution.