What does the world look like post COVID? A scenario analysis

This scenario analysis covers two stages from where we are now: the Transition Period to the New Normal and the New Normal itself.

Beyond the human tragedy of COVID-19 lies its impact on real economies and financial markets. This scenario analysis looks at what a post-COVID world may look like under different assumptions, based on market behaviour or forecasts by other recognised and trusted sources.

Considerable uncertainty remains but already one thing seems clear: the impact of COVID-19 will be material and long-lasting on all economies - defining a New Normal for global affairs.

For us the definition of a New Normal starts from a simple observation: the world will want to take steps to improve pandemic resilience. What were once thought of as black swan events - once in a century - have already become much more frequent in other areas of natural disaster. The world cannot afford for pandemics to flock in the same way.

As we write (end April), global equity markets have (on average) recovered more than half of the value lost in their early dramatic falls boosted of course by the multi-trillion dollar fiscal and monetary support programmes and, more recently, by hopes for a treatment - but not yet a vaccine.

But progress from here, the road to the New Normal, will depend on the progress of the disease and the successful management of the ending of lockdowns, arguably the greatest collective challenge faced by governments, companies and citizens since the end of the Second World War.

Ultimately the progress for economies and financial markets will depend on the shape of the post-COVID landscape in which citizens, companies and states may find themselves forging new relationships with new priorities - particularly within the ESG agenda.

Executive Summary

This scenario analysis covers two stages from where we are now: the Transition Period to the New Normal and the New Normal itself. See also the accompanying slide deck.

The Transition Period

Several western developed economies have begun relaxing lockdown arrangements. The experience from Wuhan suggests caution in the absence of herd immunity and vaccine. The emphasis instead must be on strong test/ trace and isolate protocols.

The success or otherwise of those protocols, above all other factors, is that which distinguishes between our 3 economic scenarios - designated by letters of the alphabet: V, U and W.

The V-shaped recovery is where the broad consensus has settled with sharp contractions followed by recovery starting later this year at global level assuming no major further outbreaks and only small numbers of rolling lockdowns.

Using IMF forecasts, Global GDP on average recovers pre-COVID levels by the end of 2021 but with China and other emerging economies outperforming developed economies. We have adopted this as our baseline scenario.

The V-shape would likely be reflected also in M&A activity and in the flows out of/ back into investment funds. Further along the recovery path the pre-COVID calls for retail clients to be given access to private equity funds may gather pace along with the likely increases in infrastructure spending.

The U-shape is where the virus is not brought under control and even at the level of the global average GDP does not return to pre-COVID levels until after 2021.

W describes the possibility that COVID becomes seasonal, like regular influenza causing cycles of recovery and slowdown in the early years following 2021.

If a vaccine is developed and made available en mass by the second half of 2021 it would likely tip the balance further towards the V-shaped recovery.

Return to the workplace is arguably the single greatest challenge during the Transition Phase with likely different protocols recommended in different countries and different cities within those protocols having a different local experience of the disease. Using real-time data we help to illuminate some of those challenges.

The New Normal - 2021 onwards

Assuming the V-shaped consensus recovery has been delivered, what might the New Normal look like? Clearly many uncertainties remain but some things seem clear even now:

Not going back to business as usual pre-COVID

Mainly because unlike the Global Financial Crisis of 2008/9 the economies and financial markets this time are symptoms not causes - symptoms of a biological agent.

So while the Global Financial Crisis (GFC) brought a raft of legislation and regulation aimed at greater transparency and consumer protection the New Normal is likely to bring new or greater focus on pandemic resilience and the wider social issues related to that.

Increased focus on S and G in ESG

New Vaccines and the loss of biodiversity (think deforestation). The world will want/ will have to work out how to protect against future pandemic and its effects on global economies. That is likely to mean:

Accelerated efforts (investment) to develop new vaccines and new/ faster ways to develop them.

Tackling the loss of biodiversity. Ranked among the top 5 global risks at Davos earlier this year, various studies have linked the loss of biodiversity, of which deforestation is a part, to the outbreak of pandemics (World Economic Forum). The closer together the human and animal kingdoms are forced to live, the more likely it is that a pathogen makes the leap from animals to humans - a so-called 'zoonotic event'.

Tackling income inequality

Early data from this pandemic show higher infection/ mortality rates among lower income groups. Not only perhaps because of generally poorer health outcomes for poorer cohorts but also because they cannot do remote working as easily as some in higher income groups. See Brookings Institute research and the Breugel think-tank.

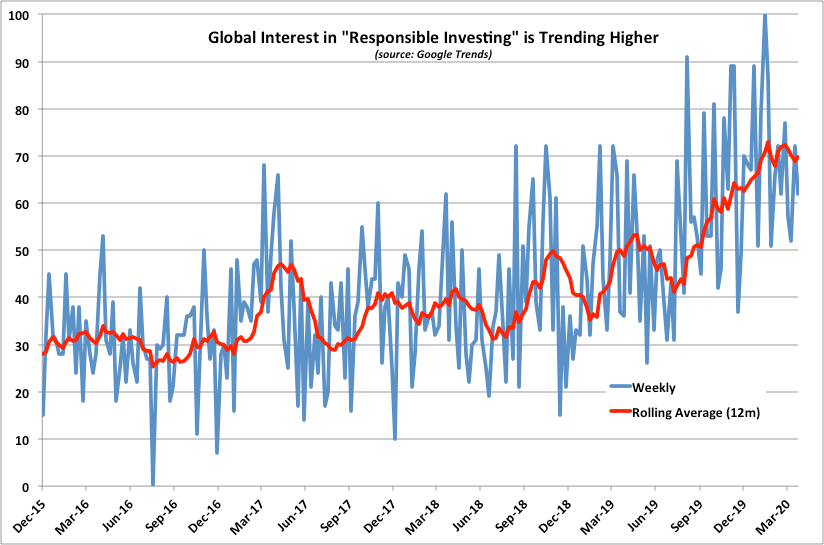

As with regulatory pressure now to suspend dividends and share buy-backs to preserve cashflow for wider societal need and shareholder activism against large executive remuneration so the push for responsible investing (see chart below) may bring calls for further rebalancing of rewards as between managers, employees and shareholders.

Remote working may become more 'sticky' if employers and employees each find advantages to a part-time version of the current arrangements when stripped of the deadly threat of the virus. If so there may be reduced demand for traditional office space and increased investment in broadband, data security. It may also bring significant changes to directors' duties in relation to a more distributed workforce and its wellbeing.

Responsible Investing

Taken together an increased focus on the Social and Governance pillars of ESG, perhaps a greater emphasis on the loss of biodiversity with the Environmental pillar, tackling income inequality and changes in the future of work resonate with calls for an increase in 'Responsible Investing'.

Those calls have gathered pace in recent years and the trend shown in the chart below may gather pace during the Transition Period and into the New Normal.

Elsewhere in our view of the New Normal:

Shorter supply chains. The pandemic has exposed the risks of extended supply chains and companies are already talking about how to mitigate those in the future through some combination of re-shoring and vertical M&A where they buy-in currently outsourced manufacturing. That may bring material changes to international trade relations including to the mechanisms for dispute resolution.

Post-COVID austerity? Levels of national debt are rising significantly as they did with the massive fiscal and monetary easing of the GFC. 2 years after that nadir came the bill - the several years of austerity. A similar pathway in this crisis might suggest governments around the world confronting major policy choices in 2022:

let national debt stay at elevated levels, potentially removing the headroom for the investment programme implied in this note;

introduce a post-COVID austerity bill to reduce national debt levels with some combination of tax increases and public spending cuts;

that would likely put greater focus on globally coordinated moves to increase the tax-take from large multi-nationals;

launch a post COVID 'war' bond to fund large infrastructure projects.

The answer is likely to be some combination of the last two; it is hard to imagine a political climate that is content simply to leave elevated debt and have no new strategic investment to shape the New Normal.

Please get in touch with your usual contact here at Simmons & Simmons for more information and to discuss further.

See our Coronavirus (COVID-19) feature for more information generally on the possible legal implications of COVID-19.

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)