COVID-19: risks and opportunities

As the WHO declares the COVID-19 outbreak a pandemic, businesses operating in all countries, not just hot spots need to be prepared.

As the WHO declares the COVID-19 outbreak a pandemic, businesses operating in all countries, not just hot spots need to be prepared.

We’ve outlined the likely economic scenarios and how to deal with them. As well as the impact on businesses across the most affected sectors. View our timeline to see the story so far.

It seems the most likely scenario is the OECD’s Downside scenario outlined below.

1. COVID-19 impact: a financial market perspective

Beyond the human tragedy of coronavirus, financial markets are down and volatile trying to anticipate its full economic impact. Those concerns are now compounded by what have been described as ‘oil-wars’ between Russia and Saudi Arabia.

1.1. Financial markets respond first and fastest to sentiment – not fundamentals

The VIX index, sometimes called the ‘fear index’, has risen to levels recently which effectively price the impact of coronavirus as second only to the Global Financial Crisis of 2008/9 with several equity markets now flirting with formal bear-market territory, down 20% from recent highs. Those falls have put UK and Euro-equity indices back to levels first seen at the end of the 1990s, making 2 ‘lost decades’ for net capital gain.

As is usual in any crisis, sentiment is the first and fastest driver of financial markets, not fundamentals, effectively following an old stock-market adage: “Sell first, ask questions later”.

1.2. The outbreak in context – how far and how fast?

We are not epidemiologists but the graphic below makes clear several things of note.

- There are three major hotspots (clusters of red circles) in China, Middle East and Europe

- The progress of the epidemic in the Rest of the World (yellow line, bottom right panel) is so far following the track of its progress in China (orange line)

- There are no major clusters (yet?) in Russia, India or the Americas

Those observations provide context for the possible economic scenarios from here.

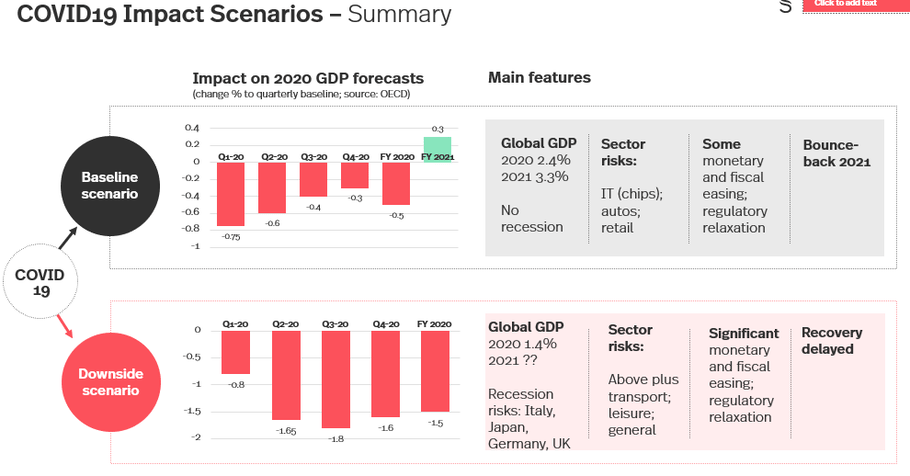

1.3. Economic Scenarios

The OECD recently updated its economic forecasts for the impact of the coronavirus epidemic under two scenarios. The following graphic summarises those and our comments as to sectors most impacted under each one. Overarching both scenarios are the existing and likely future measures to boost economic activity from interest rate cuts to relaxation of fiscal and regulatory conditions: tax cuts, increased public sector spending, time-to-pay and time-to-comply measures. The difference between the two scenarios in these areas will be one of degree.

The OECD Baseline

The OECD Baseline scenario is relatively benign with most of the impacts contained to China and to the first quarter of 2021. Subsequent hits to global GDP are progressively smaller and recession is avoided; 2021 sees a modest bounce-back as moderate fiscal and monetary easing measures work their way through the global economy.

But the progress of the virus so far, even since the OECD analysis (likely done towards the end of February ahead of publication in early March), has been rapid. If our second observation above (RoW epidemic progressing along a similar track to China) continues to hold then it might suggest a similar plateau at around 80,000 for the number of ROW cases making a global total of some 160,000 to be reached by end March/ early April.

But that is already a significant difference to the OECD Baseline which is predicated on the impact being largely contained in China. Taken together with our third observation (large populations which have still to report significant numbers) suggests a bias towards the OECD Downside case.

The OECD Downside

The OECD Downside scenario sees a sharper contraction in global GDP peaking later this year and likely running into 2021. Although the world overall avoids recession, there are individual countries at risk of recession including Italy, Japan, Germany and the UK – all of whom are projected to have sub-1% growth in 2020 under the Baseline scenario.

Under this scenario the sector risks are likely to be more widespread although, as we are seeing already, the transport and leisure sectors are likely to be particularly hard hit - as well as other so-called early cyclicals: sectors particularly sensitive to the economic cycle such as raw materials, advertising and consumer discretionary. And, of course, some up-stream oil companies may struggle with Brent crude below $40 per barrel.

The following sections from a number of our legal experts will look in more detail at the range of legal and regulatory implications include the rising risk of contract failure, use of force majeure clauses, regulatory relaxation, distressed assets, unusually large redemptions on funds, delayed corporate activity, breaches of covenant and, inevitably, rising bankruptcies.

On a modestly brighter note, although M&A activity tends to track economic downturns it is quick to recover with the first signs of upturn. Given the long gestation period of a deal that means that target identification and due diligence are likely taking place even as we go into the downturn.

For more commentary on the above, please listen to our recent webinar on the potential impact on global economies on demand here.

2. Sector impact

COVID-19 has the potential to impact to most sectors. In our key areas of focus, we are observing both risks and opportunities for businesses.

2.1. Financial institutions

The impact of COVID-19 on the financial institutions sector has been, and is expected to continue to be, multi-faceted. Given this, we think it is helpful to break these down into short term and medium/longer term considerations.

With respect to the short-term, as with any period of significant volatility, financial institutions may be experiencing increasing exposures under equity linked or secured financing structures. This may lead to an increase in the triggering of margin calls or even defaults, as certain borrowers may have insufficient assets to meet these margin calls.

Also, during periods of volatility, we may expect financial institutions to receive increased close-out/redemption requests in respect of market-facing structured products and/or wealth management/private bank clients giving orders to significantly reduce their long exposures.

In the more medium-term, the disruption to the international supply chain (particularly in respect of good/materials originating in China) may impact the ability of various categories of borrowers involved this chain to service existing debt repayments, as cashflows and normal commercial activity is impacted. A consequence of this may well be an increase in actual or potential defaults which in turn could be expected to result in an increase in restructuring and also insolvencies. It will be important for lending banks to carefully monitor their loans/debt positions with these counterparties.

The economic conditions, in particular if there is an increase in defaults, may also lead to a tightening up of credit hurdles for future lending by banks. This in turn may impact significantly leveraged sectors such as some real estate and commodities focused businesses.

These conditions however would also be expected to present a number of opportunities. For example, in times of depressed or volatile equity markets, bank clients may look to less volatile investments such as bonds and credit-linked products referencing high-quality underliers. In connection with this, it will be interesting to see whether these circumstances give rise to the first substantial test of the recently adopted narrowly tailored credit events applicable to credit-derivatives (which require a credit-deterioration in the underlying entity to occur before a failure to pay credit event can be called). Equity linked products referencing defensive strategies may also be popular (and we have already seen a number of these in the market).

Operational resilience is also an important consideration for the medium-term. The FCA by its Statement on COVID-19 on 4 March, expects all firms to have contingency plans in place to deal with major events. Alongside financial institution clients we are actively reviewing the contingency plans of a wide range of firms. This includes assessments of operational risks, the ability of firms to continue to operate effectively and the steps firms are taking to serve and support their customers.

2.2. Asset management and investment funds

In many ways fund managers worldwide are facing the same disruption to their operations as any other business and they will be continuing to monitor the impact of the COVID-19 outbreak on their employees, business travel arrangements, facilities and supply chains. However, a fund manager’s response to the coronavirus outbreak is of particular interest to financial regulators. Certainly, the FCA made it clear that it expects all firms regulated by it to have contingency plans in place to deal with this sort of major event. The FCA says it is actively reviewing these plans including assessments of operational risks, the ability of firms to continue to operate effectively and the steps firms are taking to serve and support their customers. Given the personal accountability of senior managers to the regulator for such matters, we would expect this to be very high on the agenda of firms with contingency plans being tested or, otherwise, in the course of being deployed.

In terms of the disruption to day-to-day operations, asset management firms will no doubt be considering the key person risks around specific portfolio managers and teams as well as the ability of those teams, analysist and traders to carry on as normal and meet all applicable regulatory standards. The FCA has said that it would, for example, expect firms to be able to enter orders and transactions promptly into the relevant systems, use recorded lines when trading and ensure staff has access to the compliance support they need. A number of firms are looking at testing and using their back-up sites as well as staff working from home and the FCA says that it has no objection to this approach. The important point for firms to bear in mind will be to keep their lines of communication with the regulator open and to raise any specific issues or challenges with them as the issue evolves and develops over the next few weeks.

There is also the impact on portfolios of course. We would expect managers to be watching carefully how investors respond to the situation and many managers will be reaching out to investors in order to calm any potential panic. At the forefront of the mind of many managers will be the risk of high redemptions which, when combined with falling asset values, can have the effect of increasing the levels of a fund’s portfolio invested in less liquid assets – and we all know where that can end up... Therefore, as well as contingency planning, fund managers will also be looking carefully at the composition of their portfolios and considering the adequacy of their liquidity management tool box. Having said that, it has been a requirement under MiFID product governance rules for firms to test their products and conduct scenario analysis under negative conditions for a while now so we may get to see how well prepared managers are for the impact of the coronavirus on portfolios and products.

In China, we have seen both challenges and opportunities. Challenges are mostly from a more volatile securities market and the falling of assets price in certain industries such as entertainment, catering, tourism and transportation (which are mostly adversely impacted by the spread of the virus).

On the other hand, we have also seen opportunities:

- Firstly, more policies have been formulated by the Chinese government to encourage the launch of equities fund, in order to add more liquidity to the market, boost the trading volume and enhance the investors’ confidence.

- Secondly, we have also seen opportunities arising for products dedicated to the disposal of distressed debt. In the past, the launch of private credit funds are not possible in China due to policies constraints and the regulators’ fear to blur the boundaries between an asset management product and a lending institution. Now we understand that China’s fund regulators are closely watching how the credit funds are regulated by their peers and actively working on rules to regularise credit funds, in particular NPL dedicated funds. This is also to enshrine China’s pledges to open up its NPL markets to foreign investors in the Phase I trade deal with the US.

- Thirdly, the Chinese government is in the process of introducing more favourable policies to attract foreign investment in, among others, asset management sector (which is something similar to what we saw in 2007 after SARS was over) and continue to demonstrate to the world its determination to open up China’s financial market.

- Fourthly we understand from our Chinese asset manager clients that they may start to explore more opportunities in other jurisdictions, given assets price in other places now becomes more attractive.

2.3. Healthcare and life sciences

Impact on supply chains

The risk that coronavirus poses to supply chains is keenly felt in the life sciences sector given the global nature of the industry and because the active pharmaceutical ingredients (APIs) or raw ingredients for many drugs are manufactured in Asia. Several factors can disrupt supply – as well as the potential shutdown of factories and infrastructure and restrictions on movement there is the worker quarantine issue. Even if companies could find an alternative supply there may be regulatory issues to overcome if they switch supplier, which will necessarily take time.

Pharmaceutical companies are monitoring their supply chains closely to ensure the much-feared drug shortages do not materialise. Governments are also asking companies to carry out risk assessments on the possible impact of the virus on their supply chains. So far there is little indication of a long-term supply issue unless the situation continues for many months. In that event governments could co-ordinate to help tackle the issue. What is more likely is an increase in prices, particularly for generic drugs with APIs sourced from China and India or for drugs where competitor products are hit by supply disruption.

Europe (and particularly the UK) may be better placed than the rest of the world to deal with potential shortages. Many companies were maintaining a stockpile of drugs to guard against the effects of Brexit and these stockpiles could be repurposed.

Open research

The fast-moving nature of the outbreak has also shaped the way the industry is approaching this challenge, with a focus on openness and collaboration. The industry is working together to share data and findings to make science faster in the search for effective diagnostics, treatments and vaccines. Publicly available (and free to access) databases of the latest scientific research are being compiled and updated daily by the World Health Organisation amongst others. While some worry that the speed of publication (often without formal peer review) could compromise the quality of research, most welcome the new approach. Rapid dissemination of reliable information is probably the most effective means of fighting the virus.

Faster drug development

The volume of data and technology available today makes the industry much better placed to deal with the outbreak than it has ever been. For example, the whole-genome sequence of the virus responsible for COVID-19, SARS-CoV-2, was obtained and released to the public early on in the outbreak, something which was not possible (at least at such speed) in other earlier infectious disease outbreaks. Having this information readily available should result in the speedier development of drugs and vaccines to combat the virus.

Various institutions and enterprises are in the race for new drugs (including new use of existing drugs), therapies and vaccines. While Gilead’s Remdesivir appears to be the frontrunning drug candidate, certain China pharmaceutical’s announcement of generic Remdesivir production and subsequent reprimand by the authorities raises again expectation of China’s patent linkage legislation, which has been inferred to in the US-China phase I trade deal. The relatively long cycle of drug development turn eyes toward vaccines, which are generally considered more cost-effective for contending viral outbreaks, and therapies such as recombinant antibodies.

From a China perspective, the coronavirus outbreak first demanded rapid development of diagnostic kits and production of protective gear and hospital consumables. While demands at such magnitude are unlikely to be recurring, companies that developed quality products would reap lasting benefits in their brand image and the education of the HCPs, which could be the differentiator in the fragmented IVD and sequencing subsectors.

Healthcare organisations

The potential shortage of staff in health care system facing a massive irruption of infected patients will impose an urgent rethinking of the entire health care organisation to support basic medical needs.

Big data

While the coronavirus outbreak exposed various weak links in China’s disease control, public hospital and clinical trial systems, big data and AI-based population monitoring availed unprecedented disease control measures. In addition, the suspension of offline operations feed the huge grow of telemedicine, online drug sales and other technology or internet based medical solutions. These would prompt the relatively conservative healthcare system to further embrace new technology and business models.

2.4. Technology, media and telecommunications

The origination in and spread of COVID-19 across China has impacted on the TMT sector as China is obviously a major supplier of technology components and manufacturer of technology products. Wuhan, the origin of the outbreak, is an important location of semiconductor and LCD screen production and the manufacturers there supply both domestic and international manufacturers. Any slowdown in production (and the extent of slowdown in production in China as a result of COVID-19 is currently unclear) will impact the manufacturers of many electronic devices and the “just in time” model of manufacturing that is commonly applied in the technology sector (where limited input stock is held) exacerbates the problem.

However, the extent of any impact on production is not yet clear. A number of Chinese technology manufacturers have reported that they have been able to continue production without material disruption (for instance because only R&D facilities have been affected) whilst others (such as Foxconn) have reported that they have had to shut down certain facilities.

Whatever the precise outcome it seems likely that both Chinese and non-Chinese manufacturers of electronic equipment will face a reasonable degree of supply chain disruption and production issues. This could, in turn, restrict supply of products and development and release of new products.

Data protection

Employers are facing questions about what data they can and cannot collect in relation to employee health and what employee data they can and cannot disclose to others.

For example, the question arises as to whether an employer can collect data relating to tests for COVID-19 or relevant symptoms. Can they collect and use that data to manage the health and wellbeing of that employee and other employees? The answer to that will depend on whether there is a lawful basis for collecting and using that data. From a GDPR perspective it will be necessary not just to look at the GDPR (which allows, for example, health data to be collected and used to comply with employment law related obligations like health and safety obligations) but also local legislation which can apply specific conditions to the collection and use of health data. For example, in Italy, the data protection authority has warned companies against routinely collecting health data saying that such activity must be reserved to health professionals.

Also, as employers consider business continuity planning they may want to distribute alternative contact details for employees or establish alternative means of communication (e.g. through instant messaging applications). As a result they may wish to distribute personal contact details to other employees. Again, whether this is permissible largely comes down to whether there is a lawful basis for the collection and distribution of the data. From a GDPR perspective, it should be permissible for the limited circumstances contemplated on the basis of the collection and disclosure being in the legitimate interests of the company. However, the company should take steps to try to minimise the extent of data collection and disclosure (e.g. by using corporate issued device details where possible).

The view from China

We have observed mixed impact of the COVID-19 outbreak on China’s TMT sector, including immediate focus on contract performance obligations, near-term suppression on overseas expansion plans but also opportunities for new subsectors of online and cloud-based services.

Global contracts, particularly supply contracts, are among the first to be impacted (and urgently analysed for our China clients). While governing laws of the contracts and market practices in each subsector lead to varying legal risks and practical considerations, the common theme includes timely notification, good faith effort of mitigation and preparing beyond the force majeure clauses. Now with the epidemic spreading across different continents, it is reasonably expected that overseas collaborators would on one hand be more sympathetic to the Chinese suppliers.

Global plans of some Chinese may be put on hold because of uncertain business outlook, expected stress on cash positions and logistic hurdles. While opportunity window for certain transactions may be missed, we do expect those plans well aligned with companies’ global strategy will be carried out eventually.

Similar to the SARS outbreak that boosted China’s nascent e-commerce business into its world-leading status, the COVID-19 outbreak forced nationwide remote work and education arrangements, which translate into enormous demand on services for online conferences, online education, cloud services customised for various business scenes, etc. - we witnessed millions of downloads of previously unknown Apps and exponential growth of relevant services. Extended online use by hundreds of millions users and big data applications used in disease control inevitably lead to demand for more efficient and stable connectivity, eg, 5G technology and next generation IT infrastructure. We expect similar shift of business scenes to online would occur in countries that are so far less internet-savvy, which may create business opportunities for TMT companies which solutions or services have been battle-tested in China.

3. Protecting your business in the face of COVID-19

To help businesses prepare for and react to the potential impacts we have identified some of the key concerns and issues we are advising on during this time of global uncertainty.

3.1. Commercial and Business contracts

Businesses should review key contracts for applicable termination provisions, clauses regarding delay, notice provisions and "force majeure" clauses. See our article on "force majeure" clauses and the doctrine of frustration here.

Force majeure

Many of the actions taken by governments globally to control the spread of COVID-19 are having an impact upon the performance of contractual obligations.

Whether you are facing a claim for force majeure or looking to make such a claim as a result of the disruption, you need to review your contracts in order to determine:

- What is the governing law for this contract – does it allow the application of force majeure as a matter of right (for example PRC law) or does it depend on the wording of the contract (English law and other common law contracts)? Does the Convention on the International Sale of Goods (“CISG”), which has a force majeure provision in Article 79, apply?

- What is the wording of the force majeure clause (or similarly any statutory provisions):

- Does the definition of force majeure cover COVID-19 and/or the government actions?

- What impact is required on contractual performance? If performance is required to be ‘prevented’ this is a higher threshold then if performance only needs to be ‘hindered’.

- Do the facts show a direct causal link between the force majeure event and the impact on contractual performance? If the performance issues have been caused by the general economic impact of COVID-19 rather than any specific government measure that is unlikely to be sufficient grounds for a claim.

- Are you required to mitigate the impact of the force majeure event by looking at alternative means of performance? Many clauses require that you take all reasonable steps to avoid or mitigate the effects of the event.

- What are the notice requirements? Many clauses and statutory provisions require that timely notice be given.

- What are the consequences of claiming force majeure both short and long term? Usually force majeure allows a party to suspend performance while the event persists but be aware that some clauses allow for termination of the contract if the force majeure event lasts for a certain time period.

For a more detailed review of the law on force majeure and frustration see our article here.

Other considerations

As well as reviewing your contracts, other practical steps that you should implement are:

- Centralise your communications with your counterparties through one person and make sure any communications and negotiations preserve your existing legal rights.

- Mitigate your losses. Any party looking to make a damages claim needs to mitigate its losses

- Keep a detailed record of how the COVID-19 outbreak and its knock-on effects are impacting your performance, the losses caused and any mitigation undertaken. Put in place policies to retain documents and collate supporting evidence for any future dispute.

The China Council for the Promotion of International Trade has reportedly issued thousands of force majeure certificates. These certificates are not determinative and the companies seeking to rely on these certificates will still need to prove all of the elements required in any force majeure claim. The certificates may have some evidentiary value and are sometimes required to make a claim.

3.2. Loan and credit agreements

Businesses should review any loan and credit agreements carefully, and well in advance of reporting deadlines. If terms may be breached a plan can then be formulated and advice taken. Engaging with lenders early can often lead to a better outcome than trying to ignore or deny obvious risks.

In particular:

- Covenants: Can loan covenants continue to be met? If there is likely to be a breach, lenders could demand a right to accelerated repayment. Whether the loan covenant has been breached may be open to interpretation, or the lender may have absolute discretion. Take advice on the likely interpretation of the clause. If there is a breach, consider whether the breach can be remedied or whether a waiver should be sought from your lender. Timing could be everything. If a waiver is not secured before year-end, accounts may need to reflect a change in the nature of the loan from a non-current to current liability.

- Events of Default: Check the wording of events of default clauses, including whether COVID-19 could give rise to such an event that would allow a lender to call in a loan

- Material Adverse Change: Check any Material Adverse Change clauses. MAC clauses can be found as isolated clauses or, for example, within representation, covenant or event of default clauses. Whether or not the MAC clause could be triggered by COVID-19 will be a matter of interpretation in each case.

- Representations: Check any representations made and whether there is any requirement to update representations on a continuing or periodic basis, and whether any of these representations may no longer be true and accurate as a result of COVID-19.

3.3. Insurance

The world is watching closely as the Covid-19 strain of coronavirus spreads. The effects are being felt even where there are no or few reported cases, given the nature of global business arrangements. Mounting concerns and precautionary measures disrupt markets and supply chains.

Companies and their insurers need to check carefully the wording of any contracts and any insurance policies in place. All business lines are potentially impacted and likely to see claims.

What are the key implications of a global pandemic for insurers?

Compulsory quarantine regimes are in place in some parts of the world. Elsewhere, people are being asked to self-isolate after travel to certain regions. The initial impact will be felt by travel, aviation and marine insurers, but legal disputes and insurance claims are, of course, likely to arise across many other business lines.

If the virus spreads further, businesses will face ever more severe staff and materials shortages. Businesses may find themselves simply unable to perform contractual obligations as a result. Our materials exploring the implications of the outbreak can be found here, including considerations for employers and this article on the implications of force majeure clauses and the doctrine of frustration under Hong Kong and English law. The London market is reportedly already to seeing large numbers of claims for business interruption across all lines.

Going forward, the current outbreak and its impact are likely to have an impact on policy terms and conditions. Speciality pandemic cover is likely to become a common extension to (or exclusion in) policies across many lines. Those in the course of renewal negotiations, in an already hardening market, may find themselves struggling to account for the potential impact of coronavirus in terms of presenting and pricing the risk.

The implementation of working from home strategies and self-quarantining may lead to more fundamental changes in the way we work. This will have a knock-on effect in terms of insurance terms and conditions – we may well see pandemic clauses (and exclusions) becoming an ordinary part of many insurance policies.

We have discussed some of the more immediate considerations for insurers here. These include business interruption, event and contingency cover, financial lines and D&O, professional liability, construction, cyber security and data risk.

3.4. Increased insolvency risk

Profit warnings across a broad range of sectors have been increasing steadily since 2015. Unfortunately, we anticipate this trend to continue this year and beyond.

Uncertainty surrounding Brexit and mounting global trade and growth concerns were already causing consternation even before the COVID-19 outbreak. Businesses are now reviewing how to manage widespread disruption to supply chains, and how to continue trading for example in the face of lack of availability or delays to supplies. For many businesses, already under pressure, the impact of this further disruption may be more than they can bear.

The issue goes far beyond companies with obvious links to China. Companies in all sectors are beginning to report on the negative potential financial effects of COVID-19 on first quarter revenues. Airlines, hotels and others in the travel and leisure sector are coming under particular strain. Luminous Cruise and the Fujimiso Hotel in Japan were among the first reported to file for bankruptcy as a direct result of COVID-19, while airline Flybe has been forced to enter into administration.

Do you need to seek formal or informal protection from creditors?*

A company can seek to protect itself from creditors in a number of ways. Those include informal agreements, raising additional finance, restructurings and formal insolvency procedures (including some which provide for a moratorium on claims against the company's assets). A detailed account of these different options is outside the scope of this note but our highly experienced Restructuring and Special Situations team can assist.

There’s a number of considerations for businesses and officeholders in the UK. We have discussed some of these in COVID-19 impact: Managing Insolvency Risk and Financial Reporting.

Ongoing litigation

If the company is involved in ongoing litigation, is there an increased risk that your opponent will soon become insolvent?

If you are the Defendant, consider whether you should apply for security for costs. If you do make such an application for security, or already have security in place, check what effect the order for security would have in the event of insolvency - many orders for the payment of security will not rank ahead of other unsecured creditors meaning that you may still be left with little protection on costs.

If you are the Claimant, consider carefully your enforcement strategy. Can other related parties, with a lesser risk of insolvency, be included as Defendants? Consider the terms of any after the event insurance policies and how they may be affected by the insolvency of one of the parties.

Does the current climate create an opportunity for settlement? Consider carefully with advisers whether any payment made by way of settlement could be challenged as an unlawful antecedent transaction in the event of insolvency and what protections it might be possible to put in place in any settlement agreement.

3.5. Disinformation and Reputation Management

Anti-disinformation

As new cases of the novel coronavirus disease known as COVID-19 continue to emerge, so too do reports and posts on the internet and social media platforms about it – many of which have proven to be misleading or outright false. From posts about the source of the virus and its health impact, through to the impact on basic supplies such as toilet paper, the coronavirus has brought into sharp focus the importance of being able to trust what we read online. Here we have taken an in-depth look at the state of anti-disinformation laws in Hong Kong SAR and Mainland China, as well as developments aimed at addressing the challenges of disinformation in Hong Kong SAR and Mainland China, as well as in Singapore and the UK. Key points we cover include:

- platform operator liability and enforcement in Mainland China;

- recent trends of content removal requests in Hong Kong SAR;

- recent enforcement of the Protection from Online Falsehoods and Manipulation Act in Singapore; and

- UK developments on the first online safety laws of their kind.

Reputational damage

If you feel that stories are being published which are unfairly damaging your company, our reputation management experts can help with online and print media strategies including advice on potential defamation, malicious falsehood and/or harassment claims.

3.6. Employment considerations

The COVID-19 outbreak is having a significant impact on employers globally. Many of the actions employers should take will depend upon requirements imposed by local Government and any official local guidance. See here for our country-specific advice.

More broadly, the key considerations for employers are set out below:

Practical management from a people perspective

Employers should be considering what practical measures can be taken to ensure that they fulfil any duties of health and safety or care towards their employees. Those may include:

- monitoring official travel guidance and restricting travel to known-affected areas in line with that guidance

- monitoring guidance on self-isolation and having a policy on when it is appropriate

- ensuring that employees are prepared for homeworking where necessary

- planning for operational challenges due to higher than expected absences (for example, in the UK, the FCA has published a statement setting out its expectations)

- considering other prevention measures, such as encouraging staff to maintain good hand hygiene and providing appropriate hand sanitisers etc

- communicating with employees to ensure that they are up to date with the actions being taken and latest guidance.

Self-isolation

Employers will need to monitor and follow Government guidance on self-isolating. One of the key issues is whether employee should be paid during a period of self-isolation. This may depend on whether (a) the employee is actually suffering from symptoms of coronavirus and therefore sick, (b) not actually sick but required to self-isolate due to official guidance or medical advice, or (c) simply requested to self-isolate by their employer as a precautionary measure. Whether an employee has the right to be paid will likely vary according to jurisdiction.

*Home-working

Employers should consider if and when they have the right to request that employees work from home, as well as ensuring that employees are adequately set up for remote working. On the other hand, employees may wish to work from home for fear of catching the coronavirus and request to do so. In that case, employers should listen to their concerns and consider whether this is appropriate and feasible.

School closures

We are now seeing closures of schools and universities. Employers therefore need to consider how to deal with employees who are unable to work because they need to care for their children. Options may include emergency dependant leave (whether or not this is paid is jurisdiction specific) or agreed holiday.

Travel restrictions

Restrictions on travel are a key consideration for employers with many putting new temporary travel policies into place. Of course, employers need to monitor the official travel guidance and ensure that they are compliant. Many have also implemented broader restrictions on travel to destinations which are not known-affected areas. Employers also need to consider their policies on personal travel, for example where an employee wishes to travel on holiday to a known-affected area, requirements to notify them, and the implications of self-isolation on their return.

Dealing with suspected or confirmed cases

Employers need to have procedures in place to deal with circumstances where it is suspected or confirmed that an employee has coronavirus at work. Employers also need to consider how to communicate appropriately to the rest of the workforce, whilst also complying with data protection restrictions and without creating unnecessary concern.

3.7. Risk of fraud

At times of financial strain and business disruption, the risk of fraud can increase. Auditors will be acutely aware of the present climate and difficulties that businesses are facing as a result of COVID-19. For example, there may be an increased temptation for individuals to falsify revenues to meet targets or ratios.

Businesses need to be alert to opportunistic fraud by cyber-criminals using false communications about the unfolding situation.

3.8. Trade Finance

Businesses engaged in or connected to trade finance may be impacted in a number of ways. We have discussed some of the issues arising here, which include force majeure and the law of frustration as well as implications providers of trade instruments, risk participations, trade finance loans, supply chain finance platforms, receivables financing and trade receivables financed off-balance sheet.

3.9. Tax

The tax implications of the impact of the Coronavirus on business activities may not be the primary focus for businesses at the moment, but it should not be disregarded. Where businesses have considered and prepared for the business and tax implications, they will be in a better position to deal with any adverse outcomes in the longer term.

Generally speaking, the economic impact on the economy as a whole should not be ignored. The UK economy in particular has little borrowing headroom and any further hit on productivity and growth may be significant. There is even the risk that unwelcome tax rises may need to be considered by the Government if it wishes to restrict government borrowing going forwards – at least in the short term.

Tax teams should be working with the business to address some of these issues as part of the proposed action to cope with the impact of COVID-19.

For a discussion on areas to consider, please see our overview on the potential tax considerations arising as a result of the impact of the coronavirus on business activity.

3.10. Electronic signatures

As a precautionary measure, some employers are recommending or requiring employees to work from home. This raises questions as to whether its possible to legally execute contracts and deeds using e-signature. In this article, we provide you with some frequently asked questions on the potential use of e-signatures including e-signing contracts and deeds, remote witnessing of deeds, circumstances when its not acceptable to use e-signatures and practical tips.

.png?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)