Top 10 things firms should know about the FCA CP21/9

Our guide on the top 10 things firms should know about the FCA's Consultation Paper 21/9.

Summary

On the 28 April 2021, the Financial Conduct Authority (the "FCA") published consultation paper "Changes to UK MiFID's conduct and organisational requirements" (CP21/9), setting out proposed changes to UK MiFID II requirements in relation to research and best execution.

The proposal follows the publication in the Official Journal of the European Commissions, MiFID II "Quick Fix" amendments, which formed part of the EU's post-COVID-19 capital markets recovery package. These amendments address concerns around the onerous nature of the MIFID II rules relating to best execution disclosures and investment research and constitute a partial relaxation of those rules.

However, in a key development, the FCA in CP21/9 has gone beyond the EU's "Quick Fix", proposing a much more extensive relaxation of the rules and thereby creating a significant instance of UK-EU divergence and potentially signifying the end of a policy approach that involves maintaining equivalence with EU conduct rules.

This guide summarises the top 10 things firms need to know about the FCA's Consultation Paper CP21/9 and what they should be considering now.

1. Why is the FCA consulting on these MiFID II reforms?

The publication of CP21/9 is the FCA’s first consultation in its work with HM Treasury on Capital Markets reform aimed at reviewing current regulation and ensuring that the UK regime is proportionate and not overly burdensome whilst still maintaining high standards of investor protection.

The changes proposed in CP21/9 were also addressed as part of the European Commissions “Quick Fix” package. However, in relation to other areas covered in the EU’s package where there is a case for UK change the FCA notes that these will be best achieved by changes to the UK MiFID Delegated Regulation (2017/565/EU) which HM Treasury will propose in due course.

2. Which firms are these changes relevant to?

The FCA's proposals set out in CP21/9 are relevant to:

- investment firms and market operators in the UK;

- banks and Collective Investment Scheme operators providing investment services;

- persons providing investment advice and reception and transmission of orders who did not opt into MiFID ("Article 3"); and

- persons providing research.

3. What are the proposed changes to the MiFID II inducement rules?

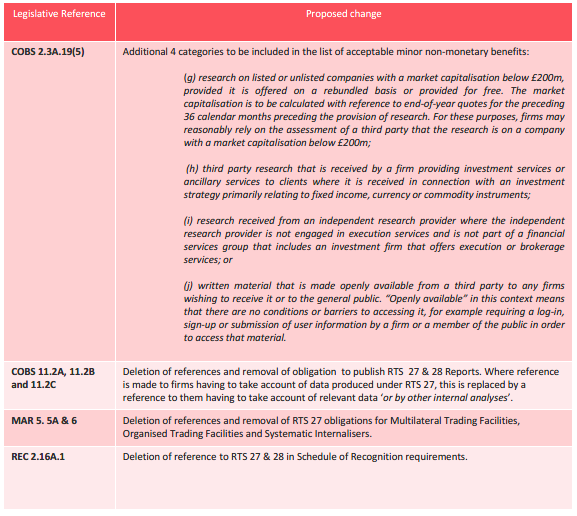

The FCA proposes to amend the inducement rules in COBS relating to research by widening the exemption of what constitutes a minor non-monetary benefit to include the following:

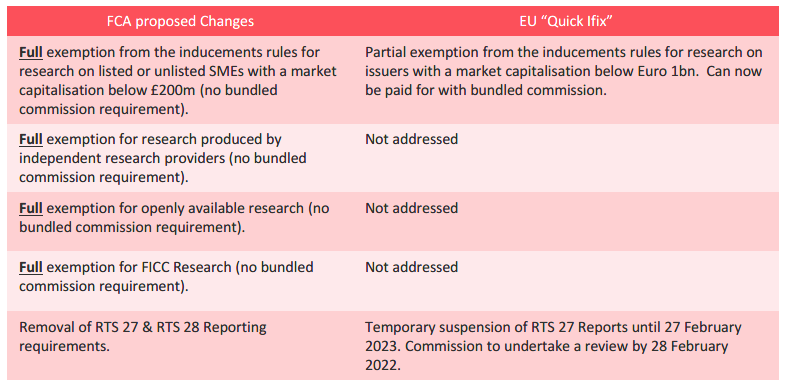

SME research - the FCA is proposing an exemption for research on listed or unlisted SMEs with a market capitalisation below £200m. Under the exemption, research on firms below the market capitalisation of £200m would constitute an acceptable minor non-monetary benefit. The £200m threshold will be assessed for the preceding 36 calendar months and the exemption will only apply if the research is provided on a rebundled basis or for free.

A key concern within the market has been the threat of decreased research and analyst coverage of the SME market as providers have been pressured to reduce their staff numbers and focus their coverage on the more valuable larger industry sectors. Coupled with the impact of COVID-19, the FCA recognises these outcomes pose a real risk to the liquidity of the SME markets and ability for SME's to raise capital.

Whilst the FCA acknowledges there are other factors that have negatively affected SME market functionality its proposal to exempt SME research from the inducement rules would make it administratively cheaper and easier for SME research providers which will in turn promote research coverage and liquidity in the market.

FICC research - the FCA proposes to create an exemption for third party research that is received by a firm providing investment services or ancillary services to clients, where it is received in connection with an investment strategy primarily relating to FICC instruments.

FICC transactions are typically not paid for by an agency commission to the broker, but instead the broker earns its revenues from the spread. Accordingly, the FCA argues the proposed exemption does not create the same opacity risks between transaction fees and research costs that arise for equity research.

Independent research providers' exemption - the FCA proposes to create an exemption for research provided by independent research providers ('IRP's'), by including in the list of minor non-monetary benefits research provided by IRP's, provided they do not engage in execution or brokerage services.

The FCA believes the risk of IRP research is small due to their independence and the fact they account for such a small proportion of the overall research market.

Openly available research - the FCA proposes to include in the list of minor non-monetary benefits written material that is made openly available from a third party to any firms wishing to receive it or to the general public. In this context, "openly available" means that there are no conditions or barriers to accessing it, for example requiring a log-in, sign up or submission of user information in order to access that material.

4. What are the proposed changes to the MiFID II best execution rules?

The FCA is proposing to amend the best execution rules in COBS to remove:

- the obligation on execution venues to publish a report on a variety of execution quality metrics to enable market participants to compare execution quality at different venues (RTS 27 reports); and

- the obligation on investment firms who execute orders to produce an annual report setting out the top 5 venues used for executing client orders and a summary of the execution outcomes achieved (RTS 28 reports).

With regards to RTS 27 reports this proposal comes as no surprise given back in March 2021 the FCA announced that it would not enforce action against trading venues that fail to produce RTS 27 reports during 2021. In the same announcement, the FCA confirmed that it would be publishing a consultation proposing to abolish such reports. However, the inclusion of RTS 28 reports in CP21/9 is a significant development here.

CP21/9 makes clear that the outcome of the FCA's review of the market indicated that RTS 27 and RTS 28 have failed in their goal of improving information and investor protection.

In particular, firms have found RTS 27 reports overly complex and often outdated and therefore irrelevant to review their best execution decisions and venue selection.

Similarly, market participants have indicated that the outputs of RTS 28 reports are equally unhelpful in deciding which brokers to use as they are too vague and not specific to their business. Instead, many find that they continue to rely on other data, such as direct feeds from exchanges, aggregators (such as Reuters, Bloomberg etc) or their own internal analysis.

Asset managers who are MiFID firms are also required to publish RTS 28 reports and the general perception is that their investors do not make any use of the published data.

5. What draft legislative changes are being proposed?

The majority of the handbook changes will be to COBS with some additional changes in MAR and REC.

In addition, the FCA intends to revoke the UK versions of:

- Commission Delegated Regulation (EU) 2017/575 (RTS 27); and

- Commission Delegated Regulation (EU) 2017/ 576 (RTS 28).

Full details are set out in Appendix 1 of CP21/9 in the following draft instruments:

The Conduct of Business Sourcebook (Amendment) Instrument 2021.

The Technical Standards (Markets in Financial Instruments Regulation) (Best Execution) Instrument 2021.

6. How do the FCA’s proposals diverge from the EU’s “Quick Fix” package of reforms?

The EU’s “Quick Fix” package proposed a number of changes to relax the rules on research and best execution and in many ways the FCA’s proposals follow on from some of those changes.

However, CP21/9 shows that the FCA is taking steps to deviate from the current EU stance and move ahead with its own UK reform to MiFID II.

Some significant EU-UK divergences under the current proposals are:

There is certainly more to come from the EU in terms of reform as part of its MiFID II review. We await the outcome of the EU's "Quick Fix " Article 5 consultation due Q3 of 2021 which will include a review on further changes to the research rules. In addition, Commissioner Mairead McGuiness indicated in a speech in February 2021 that the commission intends to publish its legislative proposals on MiFID II towards the end of 2021 which includes looking at investor protection requirements.

It may be that further EU changes fall in line with the FCA's approach in CP21/9. However, what is clear is that the FCA has taken some first definitive steps here and is showing a willingness to push ahead with UK reform in a manner that diverges from the approach taken by the EU.

What is even more remarkable is that the FCA is largely seen as the architect of the European research rules, so the UK going significantly further than the EU in its relaxation of those rules appears to be a material development. Some might argue that this development is tantamount to an abandonment of any notion of maintaining equivalence with the EU, particularly because these changes affect investor protection rules, the area that is likely to be most heavily scrutinised by the EU in the context of any equivalence decision.

7. How long do firms have to respond?

CP21/9 sets out a list of questions following each proposal in order to collect feedback on the proposed changes.

Firms have until 23 June 2021 to respond and can submit their response either using the FCA’s form via its website or in writing.

8. Next Steps for the FCA

The FCA notes it expects to publish any rules or guidance in a policy statement in Q3 of 2021.

As part of the capital markets reform, HM Treasury will publish a consultation paper looking at the broader themes which will cover a range of high-level and more detailed analysis to move towards changes to primary legislation.

The FCA will continue to align its handbook changes with any primary legislative changes proposed by HM Treasury and will revise its proposals as necessary.

In addition, the FCA expects to publish two further consultation papers during 2021. The first will consider the consequences of LIBOR transition for the MiFID II derivatives trading obligation. The second, will cover changes to markets requirements in the FCA Handbook and technical standards.

9. What should firms be thinking about?

2021 will bring a number of MiFID II reform initiatives both from the FCA and HM Treasury that firms will need to track and monitor for compliance.

Firms should make sure they closely watch these developments and start to consider:

- Conducting a gap analysis of current requirements versus future proposed changes;

- Reviewing internal systems or changes they need to implement for future compliance;

- Reviewing changes required to both internal compliance and policy documentation and external communications with customers or service providers.

10. Looking Ahead

The FCA's proposals are a sensible and positive step in dealing with some market concerns relating to aspects of MiFID II that are costly or burdensome to implement and are perceived not to be of any material benefit to the market or investors. The proposals will no doubt receive positive reception.

For many one of the changes, in particular, may seem like a long time coming. As far back in 2019, Andrew Bailey in his keynote speech to the European Independent Research Providers Association recognised the call from independent research providers to be carved out of the inducements regime.

CP21/9 suggests that the FCA is moving towards a more proportionate approach to regulation in the UK. It also calls into question whether the FCA has abandoned its original position to remain in line with EU conduct rules or whether it will continue to push ahead with UK reform and lead the way for further change.

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)