Summary

The Financial Conduct Authority (FCA) has published a consultation paper (CP25/17: Supporting consumers' pensions and investment decisions: proposals for targeted support) to address gaps in consumer support for pensions and retail investments. Two years after the introduction of the Consumer Duty (the Duty), The FCA is still concerned about the challenges consumers face in making informed financial decisions, particularly due to the complexity of pensions and investments, low engagement, and limited access to affordable financial advice.

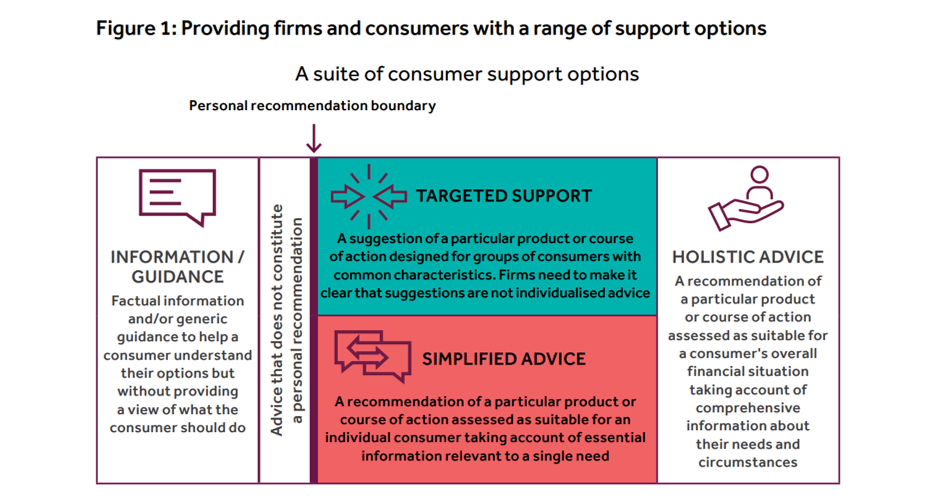

The FCA is looking to bridge the gap between generic guidance and fully personalised financial advice, enabling consumers to make better financial decisions. This builds on the UK government’s and regulators’ strategy to encourage retail investors to move money from low-yielding bank deposits into investments, with the aim of fostering greater participation in capital markets and supporting economic growth.

The consultation introduces a new regulated service called "targeted support." This new form of support will enable firms to offer ready-made suggestions tailored for groups of consumers with common characteristics and help them make informed financial decisions, without requiring the full personalisation of traditional financial advice.

This builds on previous work, including CP24/27: Advice Guidance Boundary Review – proposed targeted support reforms for pensions | FCA.

Our extensive experience of Duty implementation means we are very well placed to support firms to respond to this consultation and ultimately implement targeted support in a way which delivers good outcomes for customers and meets the long term needs of the business. Contact us to talk through what we are seeing in the market and how we can help you.

Next Steps

- Consultation period: Stakeholders are invited to provide feedback on the proposals by 29 August 2025. This is quite tight, considering there are 50 questions on the main proposals and 14 questions on the cost benefit analysis, suggesting the FCA is keen to finalise and introduce these changes quickly. The FCA will consult later this year on any consequential changes required.

- Policy Statement: The FCA aims to publish a final policy statement by the end of 2025, subject to the volume of feedback received. The FCA will consult on simplified advice in early 2026.

- Implementation: The FCA will open an authorisation gateway in March/April 2026 for firms wishing to offer targeted support and will provide further guidance on operationalising the framework.

Key implications/actions for firms

The FCA's proposals aim to fill the gap between guidance and advice, enabling more consumers to access meaningful support for their pensions and investments. Firms have an opportunity to innovate and expand their service offerings under this new framework, but they must carefully navigate the regulatory requirements to ensure compliance and good outcomes for customers.

Firms should assess whether they wish to provide the new service of “targeted support” and prepare for the authorisation / variation of permission process. Firms will also need to consider if they can meet the (fairly high) capital requirements.

Firms will need to carefully consider their pricing model for any targeted support in light of the Duty.

If firms choose to offer targeted support (or simplified advice), they will need to ensure compliance with the proposed conduct standards and consider how to integrate targeted support into their existing services. Firms might want to consider how AI could be used here.

Summary of Proposals

Targeted support

Definition

Targeted support involves providing ready-made suggestions to pre-defined groups of consumers with shared characteristics. It is not fully personalised advice but aims to deliver “better outcomes” than if targeted support had not been provided. For example, for consumers under-saving for retirement or consumers in a position to invest (who are not invested).

Scope

The framework would apply to regulated activity in relation to pensions and investments but excludes other products like mortgages and pure protection insurance.

Regulation

Targeted support will be regulated as a new activity under the Financial Services and Markets Act 2000 (Regulated Activities) Order (RAO) and will be ‘designated investment business’. Guidance would still be able to be provided without FCA authorisation (as it is now). Firms offering targeted support will need FCA authorisation and must comply with bespoke conduct standards, such as designing and delivering targeted support with due skill, care and diligence, monitoring outcomes and regularly reviewing the service.

Whilst targeted support will not be subject to the suitability rules in COBS 9 and 9A, firms must assess suitability by reference to the relevant common characteristics of consumers.

Consumer segmentation

The FCA proposes that firms must pre-define consumer segments based on common characteristics and verify that consumers are correctly aligned with these segments before offering suggestions to those consumers. Consumer segments could be consumers under-saving for retirement or consumers in a position to invest. There could also be ‘excluding characteristics’ that prevent a consumer from being aligned with a segment, which could be characteristics of vulnerability. The FCA propose that consumers can only be aligned with one consumer segment within each pre-defined situation. Firms must also consider additional information volunteered by consumers during the support journey to ensure suitability. There is some discussion around whether it would be appropriate to allow firms to make certain assumptions about consumer characteristics.

Annex 6 of the CP gives examples of targeted support use cases such as ‘under investors’ and ‘misaligned investors’ in investments or ‘under accumulators’ in pensions, and goes into detail on the characteristics of consumers in those segments.

Interaction with the Duty and existing Handbook rules

The FCA proposes that the Duty would apply to all provisions of targeted support. The FCA want to lean on the flexibility the Duty as much as possible, rather than rely on new rules. However, a firm does not need to provide targeted support in order to meet the Duty requirement to act to deliver good outcomes. When pre-defining consumer segments firms should also consider the needs of vulnerable consumers.

Current Handbook rules including product governance (PROD 3 and 4) will apply to the provision of targeted support. Other pertinent rules include conflicts of interest rules and remuneration rules in SYSC and (the majority of) the COBS framework. The certification regime would not apply (this may potentially be abolished or streamlined in the future anyway).

Ready-made suggestions

The FCA suggests that the ‘ready-made suggestions’ offered to consumer segments could be suggestions to take action in relation to an existing product or service, or new products. These suggestions would be something that is currently regulated as a personal recommendation. However, firms could not recommend a particular annuity or consolidating into or out of a particular pension product using targeted support, as the suggestions need to be ‘ready-made’. Firms could also not include any investment products subject to marketing restrictions (e.g. RMMIs) in these ready-made suggestions.

Communications

The FCA are not setting out specific rules on how targeted support communications are made (apart from them being in a durable medium), instead firms should comply with the customer understanding outcome under the Duty. There will be a specific requirement to disclose to the customer:

- the nature of the targeted support service not being individualised advice;

- the common characteristics of the consumer segment to which the consumer has been allocated;

- that the ready-made suggestion was designed for that segment; and

- any limitations on the scope of products considered by the firm.

Firms may also consider signposting consumers to different sources of support or to ‘shop around’ where appropriate (e.g. if a firm has only considered its own products). The FCA are not prescribing particular risk warnings and ask if firms want more guidance on the use of risk warnings in mainstream investment products.

Costs and charges

The FCA proposes that firms can offer targeted support free of charge or they can charge for it. Firms will need to consider the price and value outcome under the Duty and conflicts of interest when pricing. The FCA have proposed an inducements-type ban in relation to commissions for targeted support, which does not prevent cross-subsidisation.

Prudential requirements

Where a firm is only authorised to provide targeted support, it would be treated as a new form of ‘arranger’ firm and subject to Chapter 3 of IPRU-INV. The minimum capital requirement for any firm providing targeted support would be £500,000. The FCA are consulting on if a bespoke scalar should be required in addition to the £500,000 for any firm which delivers targeted support to ensure that its financial resources requirement continues to accurately reflect the specific level of risk related to growing targeted support activity.

Complaints and redress

Consumers receiving targeted support will have access to the Financial Ombudsman Service (FOS) for complaints and the Financial Services Compensation Scheme (FSCS) for redress in cases of firm failure. Firms will need to follow the same complaints handling rules that already apply for the provision of other regulated forms of investment advice.

The FCA and FOS will work together to ensure complaints about targeted support are assessed differently from those about traditional advice. They intend to do this by publishing case studies, scenarios and/or guidance.

Direct marketing rules

Firms are concerned that the direct marketing rules as currently written would hinder the roll out of targeted support. The FCA is working with government and the ICO to consider how to address this.

Approach to authorisations

Firms will either need to submit a Variation of Permission (VoP) or a New Firm Application in order to become authorised to provide targeted support. The gateway will be opened before the rules come into effect and the Pre-Application Support Service will be open. The usual types of forms and business plans etc will need to be submitted.

Use of technology and AI

The FCA encourages the use of artificial intelligence (AI) to enhance the delivery of targeted support, provided it is done responsibly and in compliance with existing regulations.

Simplified advice

The FCA also proposes to clarify and simplify rules for providing "simplified advice," which focuses on addressing a consumer's specific financial need without requiring a full assessment of their overall circumstances.

Simplified advice is distinct from targeted support and is intended for consumers with straightforward needs. It may also provide a stepping stone to the more complex holistic advice for consumers with greater wealth and more complex circumstances.

Regulation

There will not be a bespoke simplified advice regime, the FCA propose to implement this instead by simplifying the advice rules and guidance in COBS 9 and 9A to create a clearer distinction between simplified and more holistic advice.

Clarifying the advice guidance boundary

The FCA are proposing to consolidate, simplify and clarify existing guidance on the advice guidance boundary at the same time as giving perimeter guidance on targeted support. Any changes to PERG will be consulted on “in due course”, but it seems to be anticipated in 2026.

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

{kind=link}