Of black holes and potholes – they all need filling

We’ve written before about the black holes – the fiscal sort, not the astrophysical. So now it’s the turn of the humble pothole. They all have one thing in common – they need filling. The astrophysical variety is insatiable. The pothole is more tractable. The fiscal variety is somewhere in between – it can be filled but when your preferred filler comes in the form of economic growth it can prove stubbornly difficult; especially when productivity remains low, is revised lower but is relied upon to mitigate the impact of departmental spending cuts. Today’s Spring Statement offers a little more wiggle room than before, but at just 0.2% of GDP, it's hardly enough to cushion against the legion sources of economic volatility both domestically and abroad. In effect, it sets the stage for a potentially much more significant Autumn Budget to come – both economically and politically.

The problem – tepid growth and productivity; still high debt levels

Beyond the human consequence of today’s measures and others recently announced (the cuts to the welfare budget), our focus remains on their economic impact. Although the Spring Statement was billed as not being a fiscal event, and certainly not an “austerity Budget”, it likely has a material impact in both the human, political and economic spheres; and for the next Autumn Budget too.

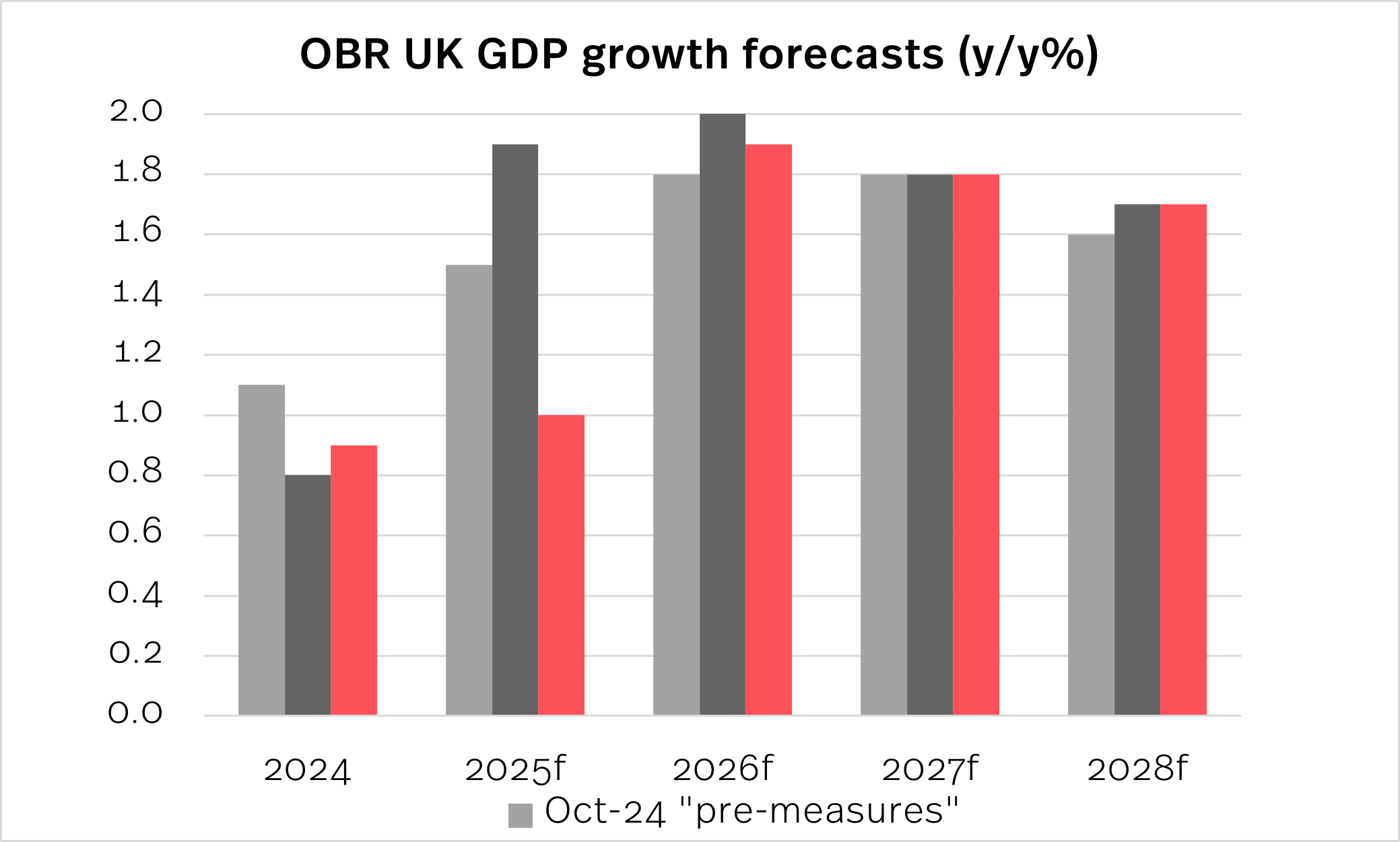

As expected the OBR has cut significantly its growth forecasts in the near-term and left them unchanged further out. The net result is shown in the chart below.

Chart: How the OBR forecasts for UK growth have changed over time

Source : OBR; Simmons & Simmons

Even those growth estimates may prove to be optimistic. As the OBR itself notes:

“The outlook has ... become more uncertain ... And recent UK population, labour force, and output data do not provide a clear signal about domestic economic prospects”

“While the Government’s planning reforms deliver a modest boost to the level of potential output of 0.2 per cent in 2029, its cumulative growth between 2023 and 2029 is still ½ a percentage point lower than we projected in October, and the level of productivity is over 1 per cent lower”

“the fiscal rules for a current balance and for net financial liabilities to be falling in 2029-30 are both met by similar small margins to October of £9.9 billion and £15.1 billion respectively. But borrowing is projected to be £3.5 billion higher and debt 0.6 per cent of GDP higher at the end of the decade than in our October forecast”

“If the projected recovery in UK productivity growth fails to materialise, and it continues to track its recent trend, then output would be 3.2 per cent lower and the current budget would be 1.4 per cent of GDP in deficit by the end of the decade”.

In other words, the risks in the forecasts seem to be skewed to the downside; and that will keep the pressure on government finances and the debate alive over new taxes, new borrowing or new cuts ahead of the Autumn Budget.

The UK productivity ‘puzzle’

Productivity is one of the most critical parameters in the generation of economic growth; another is population growth but that is another story and another headwind for the UK economy.

As the OBR noted, its forecasts are predicated on an anticipated increase in productivity – but only after cuts it made to the forecasts for productivity in 2024 and 2025.

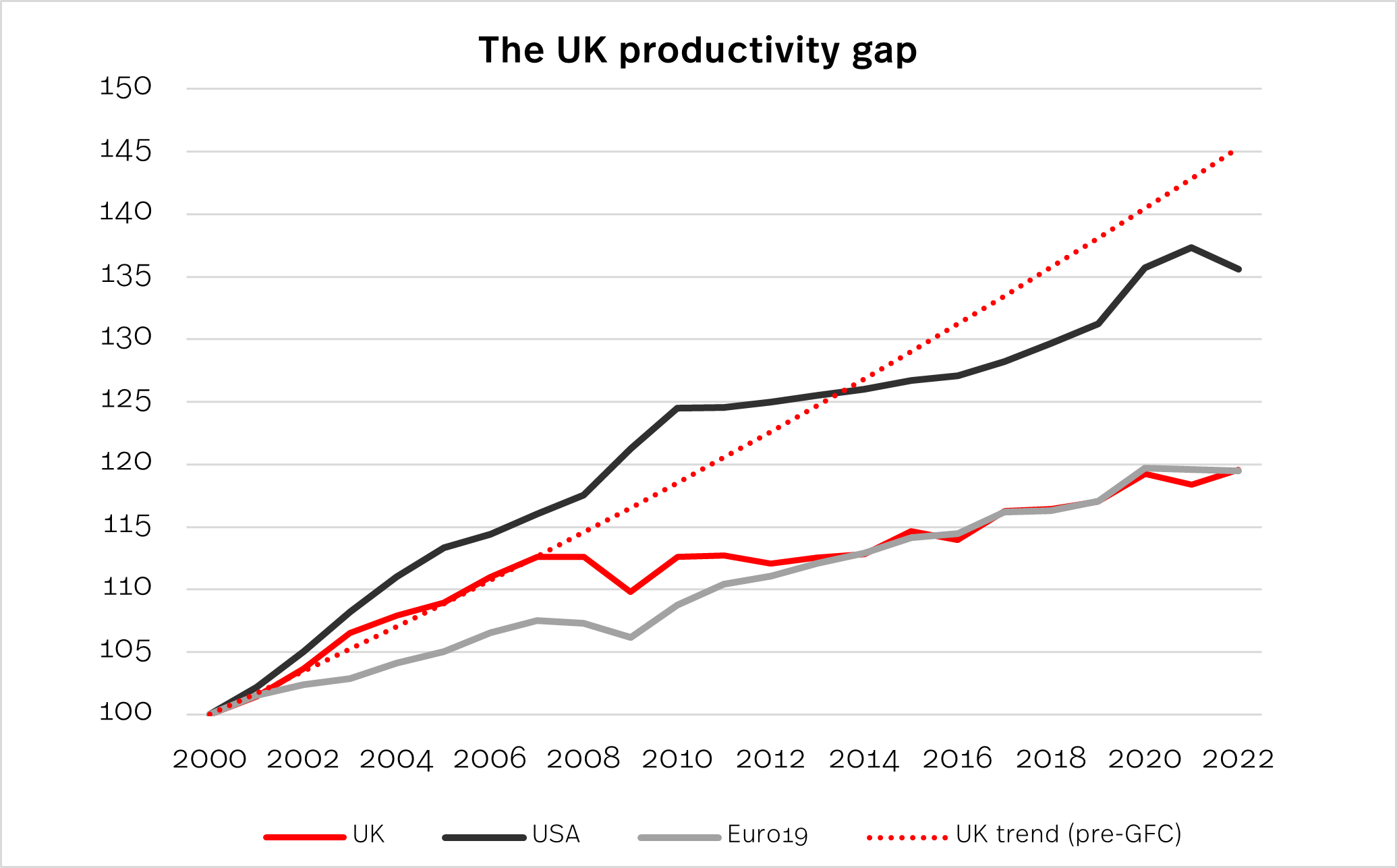

And even with the increases expected from 2026 onwards, the numbers are a long way short of the levels seen before the Global Financial Crisis (GFC). The following chart highlights the problem. It shows the progress of productivity for the UK, the USA and for the Euro Area countries (EA19).

Chart: The UK Productivity Gap

Source : OBR; Simmons & Simmons

The solid red line shows the track of UK productivity (measured as GDP per hour worked); the dotted red line shows what UK productivity might have been if it had carried on growing at its average (trend) rate before the GFC.

And therein lies the puzzle. Actual UK productivity stalled around the GFC, didn’t rise above its 2007 level until 2015 and then grew at a much lower rate albeit roughly in line with similar patterns in the Euro19 and the USA. Note that the rate for the Euro19 is similar to that pre the GFC; the UK rate is a lot lower than it was before the GFC.

Reasons for the UK slowdown in productivity since the GFC are still not conclusive but, at least as far as the UK is concerned, point to what the London School of Economics called a “chronic under-investment” in capital and skills.

Whatever the reason, its consequence is profound today and sets a large part of the backdrop to the fiscal measures characterising Chancellor Reeves’ strategy at her October Budget, today’s Spring Statement and likely throughout the current parliament at least.

For context, if UK productivity had continued to grow at its pre-GFC rate then, all else being equal, the UK economy today would be some 20+% bigger than it is now .... that’s about £500bn bigger ... enough for any Chancellor to fill any number of potholes and make fiscal black holes disappear!

Little wonder that she and the Labour government generally place such store by the productivity promise of AI.

But we are where we are: slower growth, higher debt

Absent the pre-GFC productivity rates, tepid UK GDP growth has other and material consequences for the wider political economy of the UK. In her October Budget, Chancellor Reeves unveiled her new fiscal rule - the snappily named Public Sector Net Financial Liabilities or PSNFL as a proportion of GDP. It gave her just a little more ‘headroom’ within which to accommodate the spending commitments to which the then still newish Labour government had already committed, albeit augmented by politically unpalatable choices including withdrawing the winter fuel allowance from pensioners.

But as we said at the time, that headroom was predicated on growth – the GDP in the definition of her credit limit. Having pretty much maxed-out her credit card in October, it left her vulnerable to even small disturbances or disappointments in the UK’s growth trajectory. Of those there have been several: hesitation on the part of business under the imposition of a higher National Insurance burden; an uptick in UK inflation more recently keeping interest rates higher for longer; uncertainties over President Trump’s new policy tool – general and reciprocal tariffs, so far only a threat for the UK but enough to cause a pause in some business activity. The result is not only more of the tepid growth but also lower than expected tax receipts so far this year (see the OBR commentary on 21st Feb 2025 here).

Without action, such as the reforms announced to the welfare system, she risked breaching her new fiscal rule and so losing credibility with the financial markets among others. But while that reform may square the circle for now, it leaves major questions unaddressed – most importantly the levels of government debt in the UK and elsewhere.

Persistently high debt since the GFC

The OECD Global Debt Report showed that debt service costs (interest payments) amounted to 3.3% of GDP across the OECD in 2024 – higher than most countries defence budget. In the UK, debt interest is around 3% of GDP, in the USA it’s 4%. By stark contrast, in France it’s 2% and in Germany 1% reflecting their generally lower government debt levels.

But with interest rates widely expected to be within sight of their lowest point for this cycle, the UK Chancellor (and others) cannot rely on further falls to ease significantly the fiscal bind represented by those high debt costs. Hence the pressure to reduce debt alongside investing in growth. Halving the debt interest bill in the UK could create an additional £40bn of headroom. Again, that’s a lot of potholes.

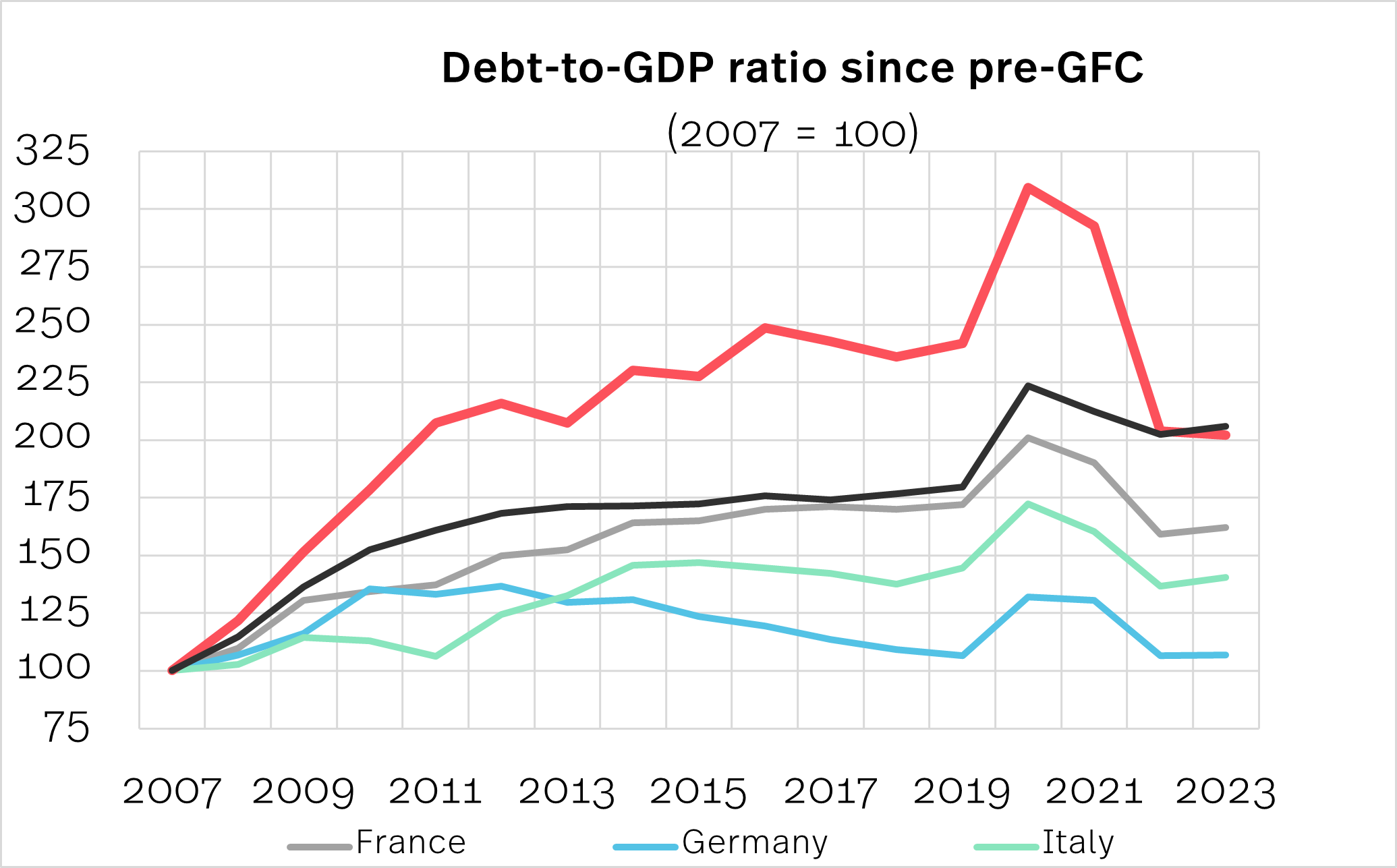

That is much more easily said than done as the following chart makes clear:

Chart: the evolution of debt-to-GDP Ratios since the GFC

Source : OBR; Simmons & Simmons

The chart takes the range of actual debt-to-GDP numbers for the countries shown and starts them all from a value of 100. Subsequent changes reflect the changes in the underlying debt-to-GDP numbers. The method makes it easier to spot common features/ trends.

Over the period of the GFC and its immediate recovery, say to 2013, most of the sample increased their debt-to-GDP by 25% to 75% mainly in the rescue of their banking systems; the UK was an outlier at the upper level – it doubled its debt-to-GDP ratio.

Thereafter, until 2019, most of the sample maintained or even cut their debt-to-GDP levels; the UK increased its level by almost a further quarter.

In the most recent period, the Covid pandemic and its immediate recovery to 2023, the UK made its most significant progress, reducing its debt-to-GDP level to around that of the USA and, along with almost all others, back to levels similar to or below (as in the case of Germany) their post-GFC level.

Welcome progress indeed by many reckonings for the UK, but high levels of debt remain and so debt interest levels will continue as part of the challenge for Chancellor Reeves as she tries to stimulate growth. But the OBR growth forecasts are hardly the stuff of ‘boom times’; enough to fill a few potholes and to create a scintilla of headroom for some of the remaining Labour Party manifesto commitments but not to silence fears of further increases in tax, borrowing or cuts to spending.

Next stop: Autumn Budget 2025; likely landmarks on the journey

The Chancellor’s pro-growth ambition will take more than mere exhortations to achieve.

On current OBR forecasts it will remain sensitive - on the downside – to:

Any US tariffs. Clearly these would be depressive for economic activity. Watch for a deal done over the Digital Sales Tax perhaps in the context of finalising a US FTA. The latter would be scrutinised in at least two areas: agreements made over imported US agricultural products and any involvement in the UK’s National Health Service.

Geopolitical flashpoints. The UK, European and other economies around the world remain to varying degrees vulnerable to events unfolding around several flashpoints including Ukraine, Israel/Gaza and China/ Taiwan/ South China Sea.

Departmental Spending Review (SR25). This government’s first, and the first by any government since October 2021, Departmental Spending Review is due to be published in June. SR25 will set the framework (called the ‘envelope’) for departmental spending on “predictable” day-to-day items, such as salaries, and on capital projects in the period from 2026/27 to 2028/29.

The Institute for Government says that “some briefings” suggest that Chancellor Reeves will cut the overall envelope and that some departments could face cuts of up to 7% in real terms between 2025/26 and 2029/30. Those would come on top of the up to 60% real term cuts in the unprotected departments during the austerity years 2010 to 2024.

If those briefings are borne out, the remainder of this parliament could become a test of Chancellor Reeves’ and Prime Minister Starmer’s confidence that any such cuts would not be a continuation of austerity but could be met by productivity improvements. See the earlier section on productivity for context.

One way lies a further depressant for growth; the other could provide a boost to productivity. At the time of writing, both possibilities exist simultaneously – a bit like Schrodinger’s Cat, simultaneously dead and alive - a metaphor perhaps for the impact of departmental cuts/productivity improvements on Labour’s subsequent popular political support in the run up to the next general Election.

And - on the upside - her pro-growth ambitions will remain sensitive to:

Defence spending. In answering the call-to-arms across Europe to increase self-sufficiency and continue to provide support to Ukraine, Chancellor Reeves took the politically unpalatable decision to reduce the overseas aid budget. In so doing she likely factored in that such funds diverted to the defence budget would result in greater capital spending than day-to-day spending and so not threaten her fiscal rule. Capital spending in the defence sector should increase its contribution to GDP in due course. The latter argues potentially for a further increase in the defence budget which some commentators believe should in any case go further if it is to provide its stated aim of self-sufficiency, including the UK’s contribution to the defence of Ukraine.

UK local elections. Due in May (although 9 such elections have been deferred to 2026 following boundary changes) and with the challenger Reform Party currently rising high in the polls, any material swing in its favour in the number of councillors elected to its ranks could prompt a more populist policy mix from the government.

If the balance of those and other factors swings against her in coming months, her Autumn Budget could become more hair shirt than gingham. And that could have profound consequence at the human, the economic and the political level.

UK interest rates. Financial markets are currently pricing two further ¼ percentage point cuts this year, in May and in August, which will clearly be helpful for the growth agenda. But the latest decision by the Bank of England was to go on ‘hold’ against a background of inflation rising since last October’s low point.

The decision itself is arguably not the most important feature – it was widely expected. Of greater significance was the dramatic shift in the voting pattern of the members of the Monetary Policy Committee (MPC) – the Bank of England body with authority to change interest rates. It has nine members and at their February meeting, against the background of still rising inflation, seven of them voted for a cut of a ¼ percentage point and two voted to go further with a ½ point cut. At the March meeting, eight voted to hold and only one voted for a cut – and that of only ¼ percentage point.

In other words, all nine members of the MPC became at least one ‘notch’ more hawkish. It may not take much to go wrong in the volatile macro-economic and geopolitical environment for that more hawkish pivot to consolidate and possibly go further.

In summary

Today’s Spring Statement and the cuts to welfare spending announced separately provide a little more wiggle room for the Chancellor than at her Autumn Budget. But at around just 0.2% of GDP, it's hardly enough to cushion against the legion sources of economic volatility both domestically and abroad. In background remains still tepid growth, weak productivity and still high debt and debt servicing charges. In effect, today’s Statement sets the stage for a potentially much more significant Autumn Budget to come – both economically and politically – and will keep alive speculation over further hikes in tax, debt and/ or cuts to public spending.

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)