Today’s Budget was billed as the most consequential for many years – and in many ways it was: a stated £40bn of additional taxes, the same again for additional borrowing. All delivered without great disturbance to the financial markets, notably the gilt market. But while the “black hole” may have been filled it appears to have been done by moving the goalposts on the ‘fiscal rule’ to allow that greater borrowing rather than by applying the hoped-for rocket boosters to the UK growth trajectory. More ‘damp squib’ than Titan. And even that may soon get tested if the US Presidential Election produces another round of protectionism.

Moving the Goalposts: an inevitable change to the ‘fiscal rule’

Something had to give. In the end - and with just days to spare – Chancellor Reeves bowed to what many had seen as inevitable and announced that she would change the basis of the so-called ‘fiscal rule’. That’s the ‘rule’, already a variation on a long-standing theme, by which the UK government reassures the debt markets that it will ensure that its policies deliver a fall in national debt as a proportion of GDP by some point in the future: in this case by the end of the current parliament.

The inevitability of the change – a relaxation – was largely cast even before the Labour Government came to power. The carefully costed plans of its manifesto were modelled by the Institute for Fiscal Studies (IFS) among many others. It showed (ahead of the Election) not only that “public sector net debt” as a percentage of national income would indeed fall (modestly!) by 2028/29 but also that the outcome would be virtually identical to that of the Conservative Party’s manifesto. So too the outcomes for the tax burden (expected to rise to 37%) and for investment spending as a percentage of UK national income (expected to fall to below 2%).

The congruence between Labour and Conservative Party manifestoes created two problems: it meant that the Labour Party could not deliver large parts of its bold vision on its own – it needed capital from the corporate sector; and it left pretty much zero ‘wiggle room’ to deal with the unforeseen if they got into power – like a lurking black hole.

Bowing then to the inevitable, Chancellor Reeves today publicly adopted a different measure of national debt to be used in calculating her ’fiscal rule’ called the Public Sector Net Financial Liabilities (PSNFL). Compared to the previously used Public Sector Net Debt (PSND), PSNFL is a broader measure both of the range in type of the country’s liabilities but also of its assets. It is, however, typically lower than PSND because the additional assets accounted for in its calculation are greater than the additional liabilities that are included.

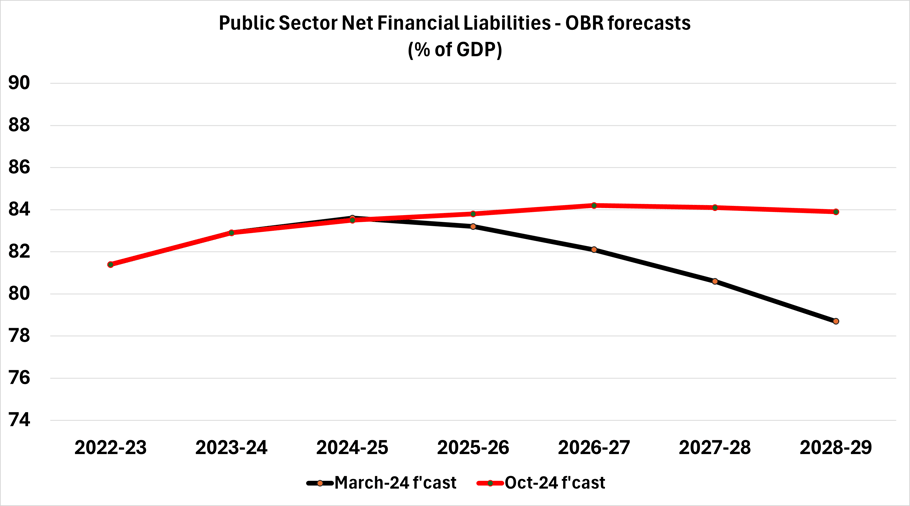

The following chart shows how Ms. Reeves has used her new tool:

Notice how the latest OBR forecast shows this new measure of national debt falling – however faintly – by the end of this parliament and so meeting the (new) fiscal rule. But it remains considerably higher for the majority of that period than the forecast made by the OBR back in March 2024.

That difference – about 5 percentage points of GDP – creates considerable ‘headroom’ for additional borrowing, a bit like widening the goalposts to make it easier for a penalty taker to score.

How to fill a black hole without spooking markets and investors

But “debt is debt” is already a common refrain among the Chancellor’s critics and to a large extent they are right: even if you change the measurement system relative to GDP if it walks like a gilt issue and talks like a gilt issue “then - by golly - it is” an increase in national debt. The OBR estimates that borrowing in 2028/29 in cash terms will be £79.1bn compared to £39.4bn at the time of its last forecast. And this comes on top of an OBR-estimated (modest) rise in the tax burden from 37.1% in 2028-29 to 38.2%. So how did the financial markets react?

In the run-up to the Election – specifically when Reeves confirmed (on 24 October) she would change the definition of the fiscal rule, the cost of borrowing in the global debt markets edged upwards in anticipation of an increased borrowing requirement to be announced in the Budget.

But that increase in cost was:

Tiny. One measure for isolating the impact of specific UK policy measures on its debt markets is to look at the spread (the difference) between the yield (interest rate) on a UK debt instrument and that of an equivalent for the US and German markets (the latter a proxy for the euro area). Against both of those equivalents the yield on UK 10-year gilts rose by 4 one-hundredths of a percent (referred to in financial markets as 4 basis points or 4bps).

While no increase is welcome, 4bps is a lot smaller than the 100bps spike over the ill-starred ‘mini-budget’ of Kwasi Kwarteng in 2022 and a likely tribute both to the sense of inevitability among investors and some ‘pitch-rolling’ by anonymous government sources giving background briefings and studiously not denying speculation that there would be a change.

Chancellor Reeves may judge her subsequent telling off by Speaker Hoyle to be a small price to pay for such a muted response from the financial markets.

Set against a backdrop of generally rising bond yields. Since mid-September the yields on 10-year government bonds in the USA, Germany and the UK have risen between 35 (Germany) and 60 (USA) basis points with the UK in between. In other words, there’s a general trend towards higher borrowing costs in western developed economies – but that’s a story for another day.

Among the investor community, Mohammed El-Erian, former IMF Deputy Director and currently Chief Economic Advisor at Allianz, said that the change in the fiscal rule “makes economic sense”, is an improvement on the current fiscal rule and allows Reeves more room for investment to improve productivity and growth. The Chancellor has also proposed tests that operate as guardrails within which proposed investment can be assessed against those criteria.

On the day (today) the yield on the benchmark 10-year UK gilt was largely unchanged while the Chancellor delivered her first Budget – and that muted response was likely a tribute to the pre-Budget ‘pitch-rolling’ for which she will probably consider her admonition by today’s Deputy Speaker a small price to pay for avoiding the fate of her predecessor-but-one when he spooked the same gilt market.

But that sanguine response did not last long: since the full details of all the Budget measures were announced – after she finished speaking – gilt yields have jumped by some 0.2 percentage points. The extra headroom she created for borrowing has some force after all.

Which brings us to growth - the dog that didn’t bark (much) in today’s Budget...

No rocket boosters for growth

Underpinning the Labour Party’s manifesto during the Election and its endorsement by leading members of the investment community such as Mohammed El-Erian (see earlier) was its “plan to change Britain” - predicated on the actions it would take to “kickstart economic growth”.

But to understand the impact of this budget on the UK’s growth trajectory we must first untangle the crossed wires created by the same circumstances that created the ‘black hole’ Ms Reeves discovered on taking office. Those circumstances were summarised in an open letter from the Chair of the OBR (Richard Hughes) to the Chair of the Treasury Select Committee (Dame Meg Hillier MP) today. In it, Mr. Hughes says that his team’s recent review of those circumstances showed that “in the run up to the March 2024 Budget, the Treasury had information about £9.5bn of net pressures on departments’ budgets in 2024/25 which it did not share with us (and, had it done so) we would have reached a materially different judgement about ... spending in 2024-25”.

To allow for that “materially different judgement” and intervening events (including Ms Reeves settling large public-sector pay awards), the OBR produced a set of “pre-measures” forecasts ahead of the Budget announcement. It is against those forecasts that we judge the impact of the Budget today. And as far as growth is concerned the result is at best disappointing.

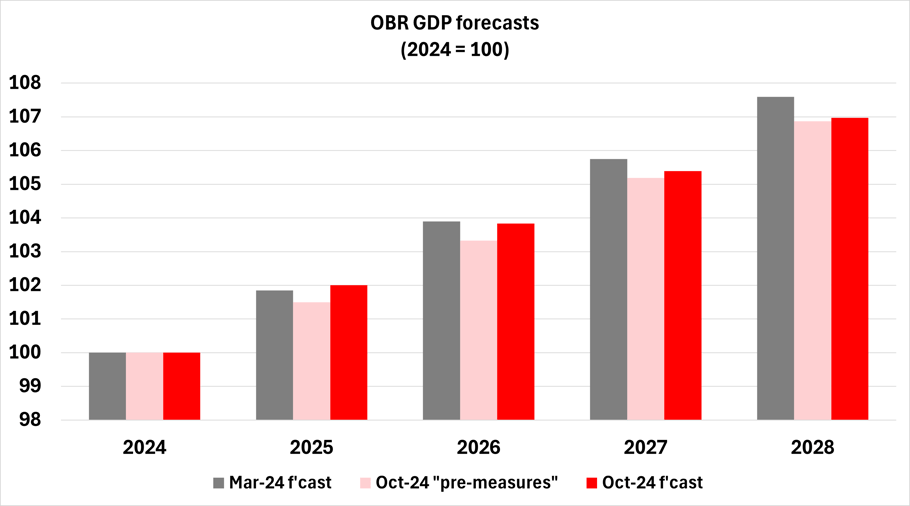

The chart above shows the cumulative level of UK GDP as forecast by the OBR on three separate occasions: at March 2024, in its “pre-measures’ forecasts and reflecting the impact of the measures themselves in the official October 2024 forecasts.

Given the uncertainties created by the circumstances of the March 2024 forecast (see reference to the Richard Hughes letter earlier) the only legitimate comparison is between pairs of columns ie compare the March 2024 forecast to the October “pre-measures” one and compare that one to the official OBR October 2024 forecast.

The first comparison shows that the original March 2024 forecast was materially more optimistic than the October “pre-measures” forecast despite UK GDP getting upgraded in the meantime. That tends to support the suggestion made by some that the March 2024 forecast might have been materially lower had the OBR possessed full information at the time it was making those forecasts.

But the second comparison shows that Chancellor Reeves’ first Budget barely moves the dial on growth compared to the new baseline of the OBR “pre-measures” forecast. Today’s measures produce something of a boost in the near-term but that fades significantly in cumulative effect as we get closer to the end of this parliament. Not much of a kick-start to the UK economy.

Over the horizon

In its latest update, (World Economic Outlook (WEO), Oct ’24), the IMF has modestly upgraded its estimate for UK GDP growth in the current year to 1.1% (previously 0.7%) and projects 1.5% for 2025 and beyond, easing modestly to 1.3% in 2029.

But those forecasts were made before today’s Budget and the accompanying OBR forecasts. And as we note above Ms Reeves’ budget barely shifts the dial on the UK’s growth trajectory. The IMF or other independent forecasters may be in no great hurry to upgrade their UK GDP forecasts on the basis of today’s Budget.

A Hallowe’en Haunting?

There is one policy announcement that will have come too late for OBR consideration but is likely to haunt the Chancellor for the remainder of this parliament: during a TV interview just days before the Budget (on 27 October), the Labour Party felt obliged to clarify that its manifesto pledge not to raise the three principal sources of taxation (income tax, Employee NICs and VAT) applied for the remainder of this parliament.

That is a quite remarkable commitment for any Chancellor given that, taken together, those taxes represent over 70% of annual Treasury tax receipts making it extraordinarily difficult to fund any significant increase in spending that might be necessary to fulfil the government’s ambitions. History is not kind to such pledges. Previous attempts at a similar lock (David Cameron’s 2015 manifesto and Boris Johnson’s 2019 manifesto) saw those promises abandoned or fudged within a couple of years. Time will tell for Chancellor Reeves.

Multi-year departmental spending reviews

But her statement today contained references to other and equally consequential announcements: in particular the proposed multi-year departmental spending review to be completed by the spring of next year. Such spending reviews effectively set the budget for each of the spending departments for subsequent (rolling) periods of several years. They give departmental heads and ministers sensible time over which to achieve their objectives rather than the ‘stop-go’ so often associated with one-year horizons.

It will be the next spending review (beyond that for the current year) which will need to do the ‘heavy lifting’ to redress at least some of the cuts to (unprotected) departmental spending since 2010 eg 20% cuts in the Justice Department, 40% in DWP and 60% in Housing and Communities (see the IFS analysis here) as well as providing for the Government’s ambitious programmes, including to deliver net zero electricity by 2030 and achieve the highest sustained economic growth rate in the G7.

US Presidential Election

But in the short-term, there is one other event over which neither the Chancellor nor anyone else in UK government has any control – the US Presidential election. The IMF’s latest WEO (see above) describes a “plausible downside alternative to the current baseline” - ie a risk scenario – in which there is a global increase in tariffs starting in mid-2025. While candidate Harris has described tariffs as a “sales tax on the American people”, candidate Trump has threatened to raise them significantly.

The IMF estimates that such moves and some related ones including lower migration would cut global GDP growth by 1.6% by 2026 ie the global growth rate would fall to half the current forecast rate. That would represent a powerful headwind for the UK government as well for others.

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)