Taxonomy Regulation – Article 8 Delegated Act Published

The key performance indicators to be disclosed under the Taxonomy Regulation have been published in the OJ and will be effective from 1 January 2022.

On 10 December 2021, a Commission Delegated Regulation (the Article 8 Delegated Act) setting out Level 2 measures under the Taxonomy Regulation was published in the Official Journal.

Its provisions, along with those in the Commission Delegated Regulation published the previous day (on which we reported here), will take effect on 1 January 2022.

The new Delegated Regulation sets out the details of the Key Performance Indicators (KPIs) to be used by non-financial and financial undertakings when making disclosures under Article 8 of the Taxonomy Regulation.

Background

In addition to setting out harmonised criteria for determining whether an eligible economic activity qualifies as environmentally sustainable, the Taxonomy Regulation is also a transparency tool.

In particular, Article 8 of the Taxonomy Regulation imposes a disclosure obligation (the Article 8 disclosure obligation) for entities which are already required to include a non-financial statement in their management report under the Non-Financial Reporting Directive (In-scope Entities). These are:

- large undertakings which are public-interest entities with more than 500 employees or

- public-interest entities which are parent undertakings of a large group with more than 500 employees.

The Article 8 disclosure obligation

- requires In-scope Entities to include information on how and to what extent their activities are associated with taxonomy-aligned economic activities in their non-financial statements or consolidated non-financial statements and

- applies to both financial undertakings (i.e., asset managers, credit institutions, investment firms, insurance undertakings or reinsurance undertakings) and non-financial undertakings that qualify as In-scope Entities.

Although Article 8(2) of the Taxonomy Regulation requires non-financial undertakings to disclose information on the proportion of the turnover, capital expenditure and operating expenditure of their activities related to assets or processes associated with environmentally sustainable economic activities, it does not specify equivalent KPIs for financial undertakings.

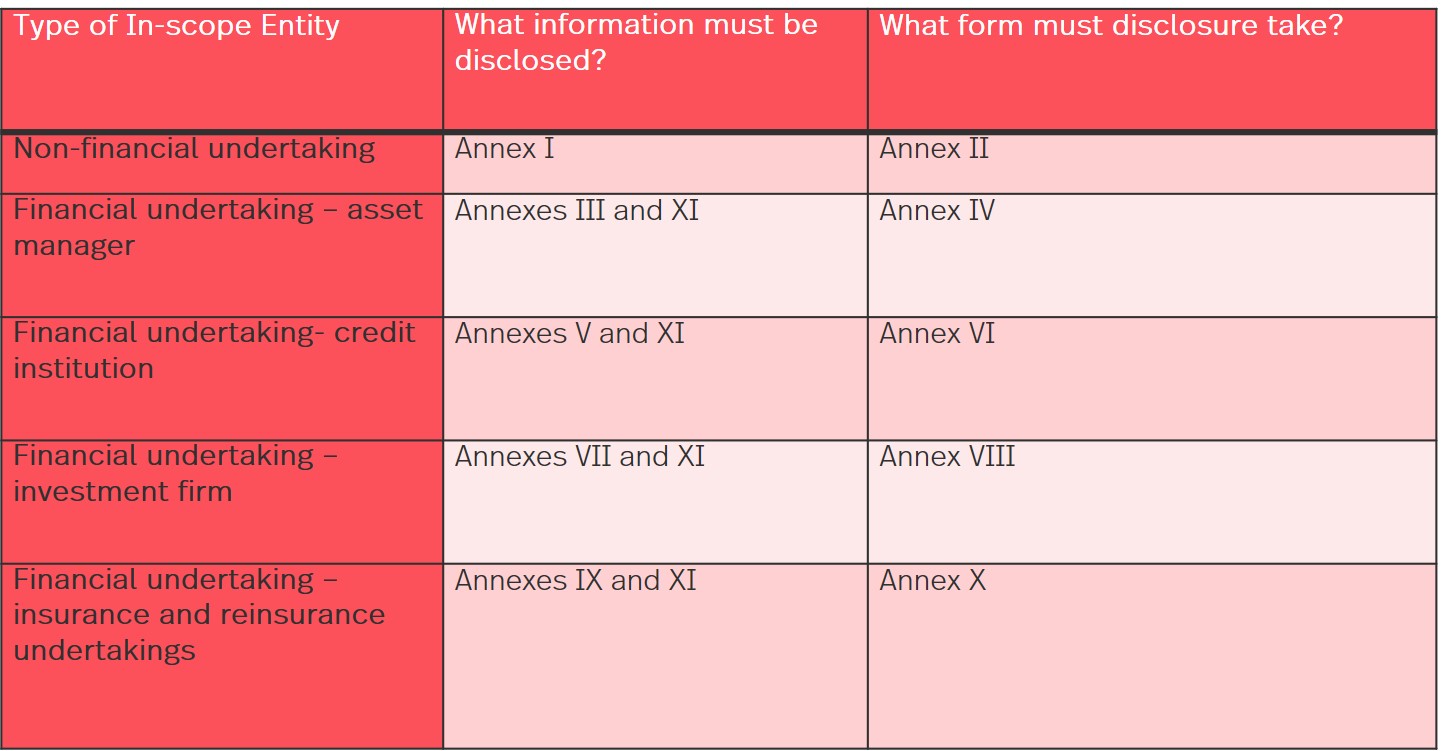

Therefore the Article 8 Delegated Act sets out the different key performance indicators or KPIs and forms of disclosure to be used by the various types of In-scope Entities, depending on whether they are a non-financial or financial undertaking and on the type of financial undertaking they are.

What does the Article 8 Delegated Act contain?

The Article 8 Delegated Act sets out the detailed rules for complying with the Article 8 disclosure obligation, with the content and presentation of the KPIs being set out in a number of Annexes:

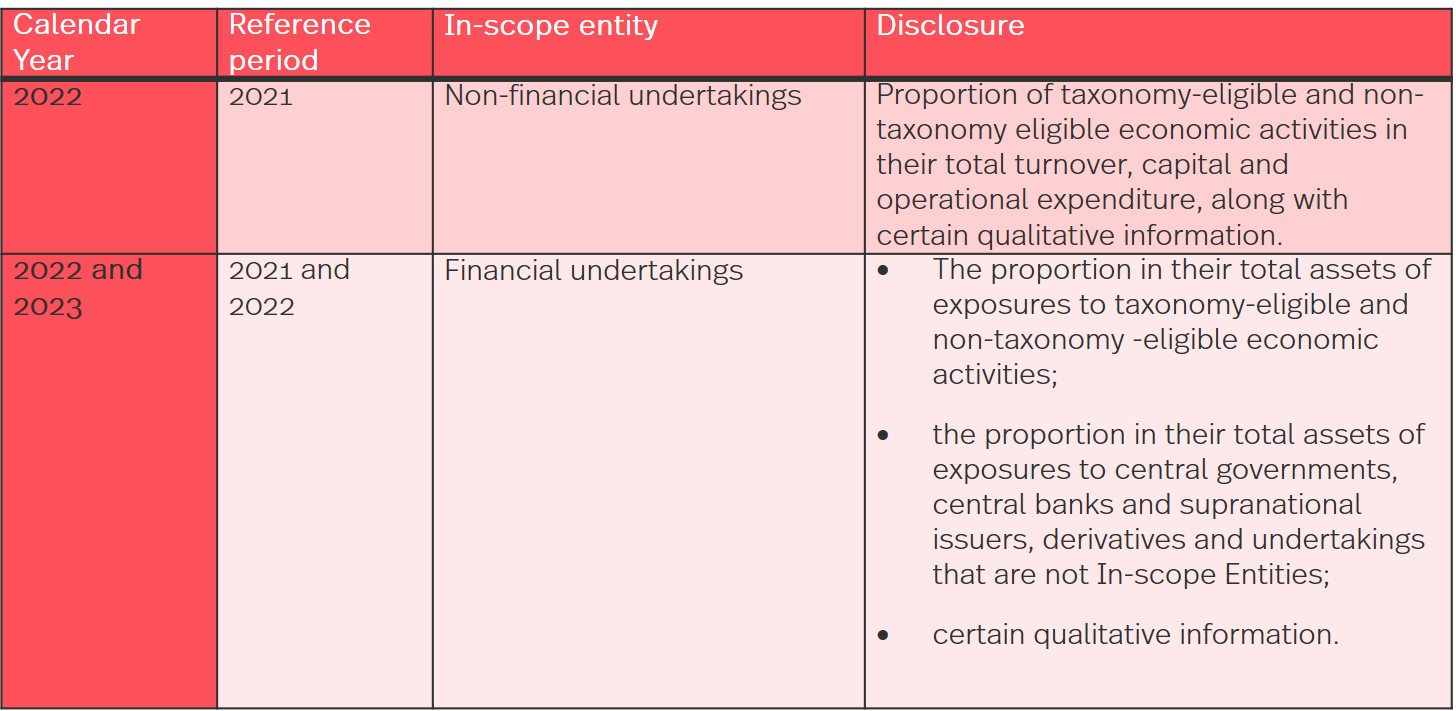

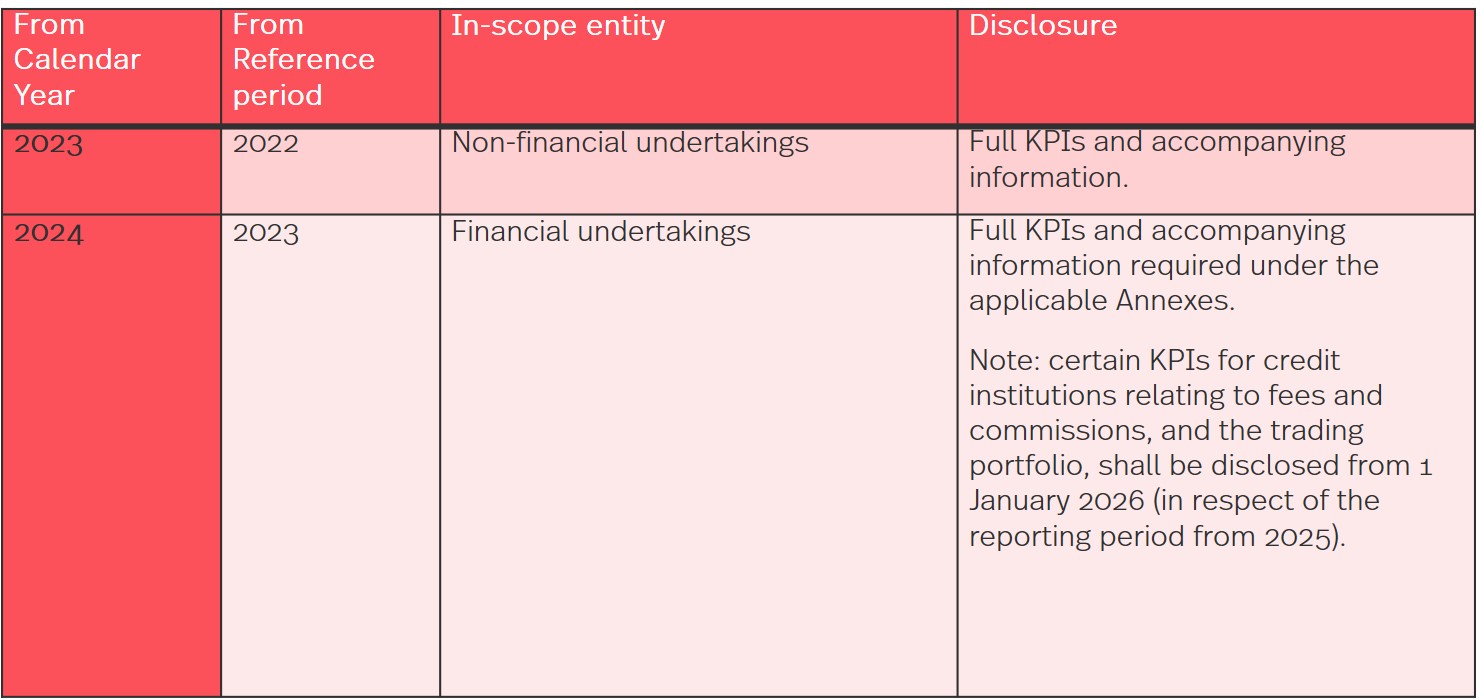

Phased implementation of the Article 8 disclosure obligation

The Article 8 disclosure obligation will focus first on Taxonomy eligibility rather than alignment, and will become effective on a phased basis as follows:

Phase 1 - disclosure of taxonomy eligibility

Phase 2 - disclosure of KPIs to evidence taxonomy alignment

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)