ESG: UK sets out its roadmap on sustainable finance

The UK Government has published a roadmap setting out its plans to develop a new Sustainability Disclosures Regime and Green Taxonomy.

Earlier this week, the UK Government published its Greening Finance: A Roadmap to Sustainable Investing (the Roadmap).

The Roadmap sets out its long-term ambition to "green" the financial system and align it with the UK’s world-leading net-zero commitment in advance of COP 26. The proposals include plans to develop a new Sustainability Disclosures Regime (SDR) and Green Taxonomy.

The roadmap envisages the following 3 phases:

1. Informing – ensuring decision-useful information on sustainability is available to financial market decision-makers.

2. Acting – mainstreaming this information into business and financial decisions.

3. Shifting – financial flows across the economy shifting to align with a net-zero and nature-positive economy.

Sustainability Disclosures Requirements

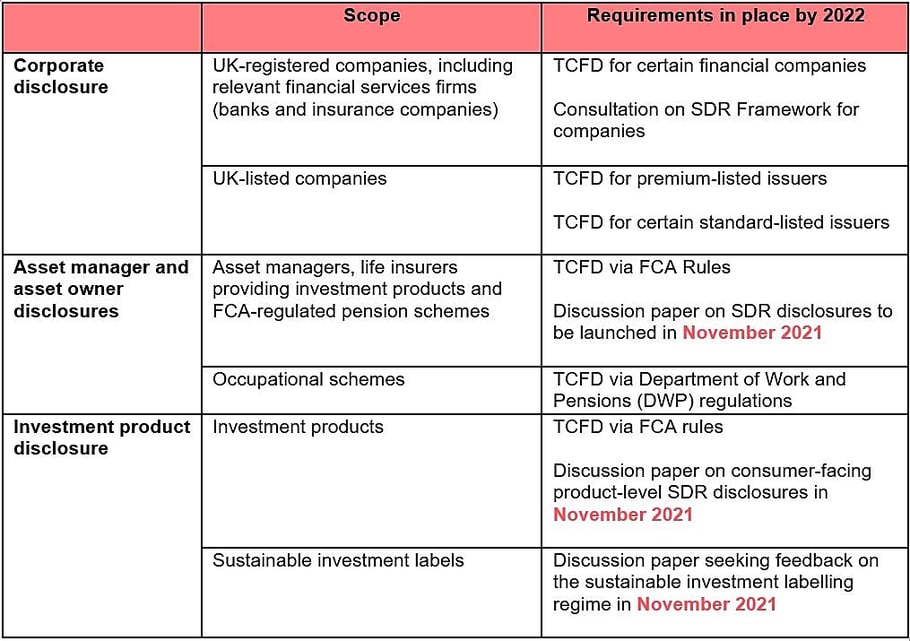

The first phase will be delivered through the economy-wide SDR. The SDR will build on the UK’s Task Force on Climate-Related Financial Disclosures (TCFD) implementation and will cover three types of disclosure:

(1) Disclosure by corporates:

new requirements for companies (including those in the financial services sector) to make sustainability disclosures in accordance with international standards and using the proposed UK Green Taxonomy;

(2) Disclosure by asset manager and asset owners:

new requirements for asset managers and asset owners to disclose how they take sustainability into account; and

(3) Investment product disclosure:

new requirements for creators of investment products to report on the product’s sustainability impact and relevant financial risks and opportunities.

This information will form the basis of a new sustainable investment labelling regime.

Disclosures across the three regimes will centre around the four key themes identified by the TCFD Recommendations. These themes are (i) governance; (ii) strategy; (iii) risk management; and (iv) metrics and targets.

SDR will also introduce a comply or explain requirement for transition plans, under which firms must either

- publish transition plans which align with the government’s net zero commitment; or

- provide an explanation as to why they have not done so.

SDR will use the same framework and metrics across the economy to ensure a clear and direct link from investors, through the financial system to the businesses they are invested in and their relationship with the environment. Metrics will be drawn from international standards, where they exist, to support international compatibility.

Discussion papers on the three SDR regimes are expected to be published in November 2021:

UK Green Taxonomy

Much like the European Taxonomy, the UK Green Taxonomy (the UK Taxonomy) is intended to set out the criteria which specific economic activities must meet to be considered environmentally sustainable and therefore, Taxonomy-aligned. Reporting against the UK Taxonomy will also form part of SDR disclosures.

The UK Taxonomy will borrow the six environmental objectives provided under the EU Taxonomy, namely:

(1) Climate change mitigation

(2) Climate change adaptation

(3) Sustainable use and protection of water and marine resources

(4) Transition to a circular economy

(5) Pollution prevention and control

(6) Protection and restoration of biodiversity and ecosystems

As with the EU Taxonomy, each environmental objective will be underpinned by technical screening criteria which identify how that activity can make a substantial contribution to the environmental objective.

The Taxonomy will also include Enabling Activities to recognise activities which currently support the transition by enabling substantial contributions to environmental objectives in other sectors, but which are not yet sustainable themselves. This will include, for example, the manufacture of components for wind turbines.

The Government expects to consult on UK draft technical screening criteria for the first two objectives in the first quarter of 2022, ahead of the legislation coming into force by the end of 2022. The remaining four objectives will be consulted on in early 2023, ahead of an implementation date in late 2023.

The good news for firms is that based on the proposals in the Roadmap, the UK government appears to be basing the Taxonomy largely on the EU Taxonomy, which should make compliance with both regimes much easier.

We will be monitoring developments and preparing notes on the detailed proposals following publication of the discussion papers in November.

In the meantime, please do get in touch with the team should you wish to discuss any aspects of the Roadmap, or ESG compliance more broadly.

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)