A far-reaching election

The result of the UK general election has potentially significant and far-reaching implications for its citizens and for all those engaged in business within its borders.

With the Labour Party winning a commanding majority, financial markets have remained sanguine since the announcement of the election date, reflecting perhaps the careful positioning of the self-styled “changed” Labour Party as business-friendly.

The ripples of this election could extend far beyond the UK's domestic social agenda. They could affect a wide range of topics, from economic growth and financial market regulation to taxation and transfer pricing; the UK's evolving relationship with Europe; the conditions for inward investment to the UK; funding the substantial investment needs of net zero and other strategic initiatives; reforming the UK's infrastructure provision, its healthcare system, and of course, its role in developing AI and other new technologies.

Over the course of the campaign we produced a number of insights analysing Labour's policy platform on this page, which together form a useful primer on the direction of the new government. With the election over, we are continuing to track the development of policy on regulation, investment and more over Labour's first 100 days in office. Click here for our analysis.

Podcasts: hear from our experts

Watch on-demand

Our panel of experts give their immediate response to the election outcome.

The new government: first 100 days

Key policy themes

We've organised our articles and analysis by policy theme to help you understand the background to the issues at stake.

International relations

Tax

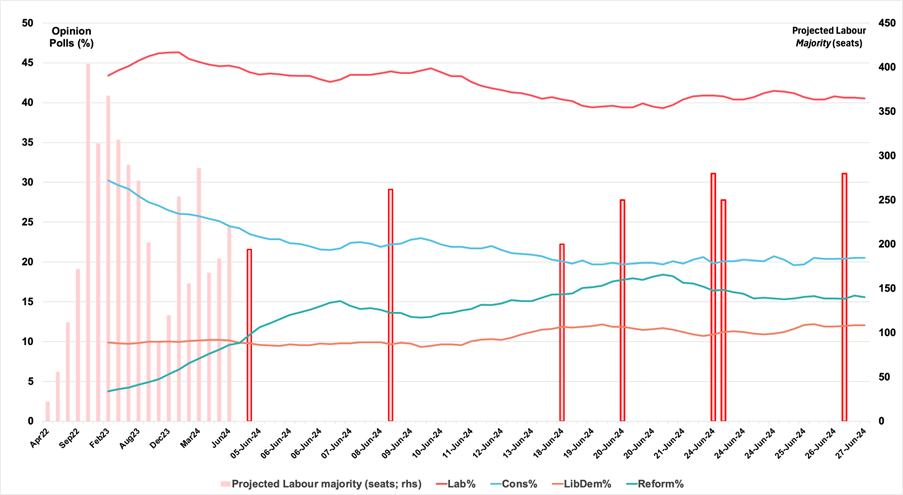

Opinion polls

UK General Election: Week 5

Another week, another projection of a commanding Labour majority. With less than a week to go to polling day the trends in the polls seem to have stabilised with the exception of the recent 2-odd percentage point decline in the trend for Reform following remarks by Mr. Farage regarding NATO and President Putin.

So much political capital just to stand still

Indeed, the story of the campaign since the starting gun was fired on 22 May may turn out to be just how much energy (and money) has been spent largely just to stand still. For sure the Labour Party standing in the opinion polls has eased back by some 5% (shared between Lib Dems and Greens) but so too has that of the Conservative Party (going to Reform), thus maintaining the gap between the two.

All else equal, that might have maintained the projected majority for Labour around the sub-200 seat level at the start of the campaign period. The reason it has risen to now over 250 is buried in the combination of Reform’s rise in the polls and the arcana of the UK’s First Past The Post (FPTP) election system.

Except for the ‘Farage effect’ – a reverse-Johnson for the Conservative Party

Without that, Labour’s projected majority, on our calculations, could be reduced to somewhere close to or within hung-parliament territory with the Conservative Party projected to get a few more MPs than the Labour Party had in the Parliament just dissolved (197). The ‘Farage effect’ appears to be just as potent for the Conservative Party as was Mr. Johnson’s in 2019 – but in the opposite direction!

Financial services outperform a sanguine UK market

So too, again, the UK’s financial markets have remained largely unmoved. As we’ve noted in previous weeks, sterling has drifted a little lower over the campaign (less than 1% vs the US dollar) and the FTSE100 by less even than that. At sector level it is a little more nuanced, with the financial services sector modestly outperforming and in-line with its global counterpart. It may be that hopes for further rate cuts and signs of growth are helping to lift all financial boats and maybe also that international investors have also accommodated to the idea of a Labour government whose manifesto includes phrases such as “financial services are one of Britain’s greatest success stories (and we will) … support innovation and growth in the sector”; helped too perhaps by the knowledge that Labour has huge need for private sector investment facilitated through the financial services industry.

Outriders to ‘incrementalism’

But with just a week to go it is worth reflecting on some of the outriders to the general picture of an incrementalist campaign leading to an incrementalist Labour administration.

An IPSOS poll earlier this week suggests that over 30% of the UK electorate still “Do Not Know” which way they will vote; although most of those appear to break for Labour DNKs are almost by definition persuadable one way or the other.

Elsewhere comes news as reported in the FT that Labour is diverting activists away from Lib Dem target seats, mainly in the South of England. Given that some opinion polls place the Lib Dems ahead of the Conservative Party, Labour’s tactic could help promote the LibDems to the status of forming His Majesty’s Loyal Opposition and relegating the Conservatives to third place.

We have noted before that any last-minute deal between the Conservative Party and Reform could see projections of a Labour super-majority collapse into hung-parliament territory (see above)

Perhaps the strongest opposition to a Labour ‘super-majority’ in the House of Commons might come from its own backbenches. Two issues have appeared in recent press that may test Mr. Starmer if he does become Prime Minister: a rebellion to secure the lifting of the current 2-child benefit cap; and a possible insistence by the EU on allowing youth movement and the UK participation in the Erasmus scheme in return for facilitating what Rachel Reeves has describes as “ditching the fixation on divergence” as part of Labour ambitions to improve working and trade relations with the EU.

We explored some of those issues in the latest of our UK General Election podcasts (see links below) and will return to explore another major one – ESG and sustainable finance – in the last of these to come next week.

The next edition of this publication is due on ‘the morning after’ the election and will likely have morphed by then into our exploration of the First 100 Days… for whoever secures the keys to Number 10.

Andy Hartwill

Client Insights Lead

In focus this week...

Time to ditch divergence?

We need to chat about... GPT

UK General Election: Week 4

Today is solstice day - when the sun reaches its highest zenith in the northern hemisphere and its lowest in the southern; for each region it marks the height of summer and the depths of winter respectively. In the political firmament the latest Sky/YouGov poll suggests similarly polarised fates for the Labour and Conservative parties. But financial markets continue generally to march to a different beat set by the Fed. And in the political firmament – as with the celestial - the gap between the zeniths can close.

The opinion polls

Our chart (above) tracking the current state of the parties has been updated to include the latest of the so-called MRP polls (see Week One’s commentary) which we reference as historically the more accurate of the polling techniques; their values are outlined in red above.

It shows two things of significance: the projected majority for Labour of 200 seats and the trends in the opinion polls continuing their respective trajectories. The first contains the data also showing projections of a record high number of MPs for Labour and record low for Conservatives.

The second shows the opinion poll ratings continuing to ease back for both major parties while those for the ‘challenger’ parties continue to rise. Of those the trend for the Reform party is worth watching closely. If it collapses, perhaps as a result of a late deal with the Conservative Party or otherwise, and Reform voters switch to Conservative then so too would the projected lead for the Labour Party collapse. As we have written before, on our calculations that scenario could put the outcome firmly back into 'hung parliament' territory with everything still to play for in the closing stages of the election campaign.

Political/Market matters

To whatever extremes the opinion polls currently point for the outcome of the election, the UK financial markets – as with others – continue to march to a different beat: the expectations for interest rates. Since the election was called, sterling has drifted a little lower against the USD, so too the FTSE100 and the FTSE250 compared to their global counterparts. The differences are small but if there is any nuance to be drawn from them it may be that investors are taking a modestly more cautious view of the outlook for the domestic UK economy than for its international components.

As for interest rates, the Bank of England’s decision to hold steady this week was largely anticipated (a cut might have risked its requirement for political neutrality during an election campaign) and in any case likely secondary to the Fed’s guidance last week towards (at least?) one cut later this year. Markets are currently pricing a cut from the BoE in August. Meanwhile the Swiss central bank cut its interest rates for the second time this year following the ECB’s first cut earlier this month. The trend to lower western interest rates in 2024 is underway but later and more shallow than had been expected.

Back in the UK political arena, one of the more eye-catching developments of this week for us was the interview given by shadow chancellor Rachel Reeves to the FT. Under the headline of wishing to seek 'improved' UK-EU trade terms if Labour wins the election she "accepted" the Office of Budget Responsibility’s "assessment (that) Brexit would lop 4 per cent off (the UK’s) productivity potential" – an unusually direct use of the B-word and its impact. She spoke also of 'tackling head on the “adversarial” Conservative post-Brexit relationship' and of 'ditching (the) fixation on regulatory divergence'. So striking is that ambition that we have made it the subject of our next election podcast. Watch this space!

Andy Hartwill

Client Insights Lead

In focus this week...

The Labour manifesto: What’s in it for real estate?

Labour pledges new equal pay legislation in manifesto

UK General Election: Week 3

A momentous week for manifestos; another miss for markets

This was ‘manifesto week’ in the run-up to the General Election on 4 July. And while the major parties and several others did their level best to impress the electorate, none of them moved the dial for the financial markets.

For sure those drifted lower in the UK (equity and bond prices – the latter pushing yields higher) but so it was in most of the major western country markets. It may be frustrating – or even humbling - for political leaders in the UK to discover that financial markets seem more focussed on the US Federal Reserve than on their plans to “make Britain great again” but that appears to be the judgement of the past week. The Fed left interest rates unchanged, in anticipation of which, investors – mostly in the US – made their biggest weekly withdrawal since December 2022. According to London Stock Exchange Group data (as reported by Reuters) they sold a net almost $15 billion of equities.

But the UK election is proving just as record-breaking in political circles and, by inference, among parts at least of the electorate. The trends which we have been tracking since the start of the campaigns (see chart above) have continued as before – and although those trends, like the financial markets, appear so far unmoved by the manifestos, they have reached what seems to be a potentially tectonic tipping point… maybe two.

The first of those is the seemingly inexorable rise in the popularity of the Reform Party, now polling within a couple of points of the Conservative Party whose decline is so far undisturbed by its manifesto launch. But the vagaries of the UK’s first-past-the-post (FPTP) election system mean that the surge in Reform’s poll performance does not translate into a surge in the likely number of MPs it would win at the election: most projections put that number around five MPs at best.

Of course there is a scenario where, given those projections, a deal of some description is somehow done between the Conservative Party and Reform, resulting in Reform’s voters switching back to Conservative: running that through the models of election outcome suggests it could collapse the Labour majority back towards hung-parliament territory leaving everything to play for in the final weeks of the campaign.

The second potential tipping point is for the Liberal Democrats: they appear to be eating into Labour’s opinion poll lead and this time the vagaries of the FPTP system seem to be working more in their favour: projections show them closing the gap on the number of Conservative MPs – a couple even show them gaining more MPs than the Conservatives. If that were to be the result on 5 July then the LibDems would become the official opposition party to the Labour Government. A truly tectonic shift in their fortunes.

As for the manifestos themselves, my colleagues and I are producing a series of summaries/explainers, all of which are available via the links from this page. One of the features of that schedule this week was the podcast recorded yesterday, the day of the Labour Party manifesto, in which our Tax Partner Martin Shah and I look at its tax and spending plans alongside those of the other parties. There’s a summary of its key points below.

Looking ahead the main scheduled event next week is likely to be the Bank of England’s Monetary Policy Committee meeting on Thursday 20 June. It too – like the Fed - has been widely expected to begin rate cutting sometime soon. Like the Fed – but for very different reasons – it too may disappoint lingering hopes. Although arguably the UK economy is less strong and therefore more in need of a rate cut than the US economy the BoE will, by custom, be wary of changing rates in the middle of an election campaign, lest it be seen to be making a political judgement. The cut may have to wait until the meeting in August.

Andy Hartwill

Client Insights Lead

Here's a summary of our podcast "Policies, Pounds and Politics" where we looked at the tax and spend proposals of Labour and the other major political party manifestos published this week. Follow the link to the actual podcast for much more of the colour and detail.

Key Points

The UK is facing a general election in three weeks, with opinion polls predicting a significant lead for the Labour Party and a potential massive working majority of around 200 seats.

However, there are other scenarios where the Conservative Party and Reform Party could do a deal, with regained support for the Tories from Reform voters, collapsing Labour's lead, or the Liberal Democrats could become the official opposition.

Labour Party Manifesto

Labour promises huge investment plans across various sectors like the NHS and green energy, with only small increases in borrowing.

Their fiscal plan is described as "non-negotiable," aiming for a balanced current budget, covering day-to-day costs through revenues, and reducing debt as a share of the economy by the fifth year.

Major revenue-raising measures (forecasts for 2028/29) include:

- £5.2 billion from closing non-dom loopholes and reducing tax avoidance

- £1.5 billion from removing private schools' VAT and business rates exemptions

- £565 million from carried interest taxation

- £40 million from a further 1% SDLT surcharge on non-residents' property purchases

On tax administation, Labour aims to spend £900 million in 2028/29 to recover a gross £4.8 billion from narrowing the tax gap, though achieving such a narrowing has historically been challenging.

Four major spending programs (including reducing NHS waiting lists and green energy plans) are predicated on two key tax measures (non-dom reforms, windfall tax on oil/gas), leaving little headroom for setbacks.

Conservative Party Manifesto

The Conservatives propose immediate measures like the "Triple Lock Plus" for pensioners and continuing to cut employee National Insurance contributions.

They aim to raise approximately £6 billion from tackling tax avoidance, spending it on their national service proposals and the "Triple Lock Plus."

Aspirations include abolishing self-employed National Insurance by the end of the next parliament.

Liberal Democrat Manifesto

The Lib Dems focus more on using taxation to drive behavioural change, targeting areas like banks, tech giants, and greening of the economy including air travel.

Both the Tory and Lib Dem proposals could lead to a significant increase in spending, and hence impact the overall tax burden, exceeding Labour's plans but still materially lower than proposed in Labour’s 2017 and (particularly) 2019 manifestos.

UK-EU Relations

The Labour manifesto has minimal references to Europe (14 mentions, mostly regarding Ukraine/NATO), with only a quiet ambition to improve trade relations and champion UK financial services.

Substantial changes seem likely to be deferred until the scheduled 2026 review of the UK/EU Trade and Cooperation Agreement, with Labour perhaps keeping its powder dry until then.

Labour plans for incremental moves initially, potentially becoming bolder if re-elected in 2028/29, envisioning a 10-year investment plan over two terms.

In focus this week...

Policies, Pounds and Politics

Manifesto tax pledges

UK General Election: Week 2

Markets

Another relatively calm week on UK financial markets despite the heat, thunder but no light from the tax row which grabbed the headlines after the first TV debate between Sir Keir Starmer and PM Rishi Sunak earlier in the week.

The FTSE 100 index drifted sideways while European and US equities eked out modest gains and the more domestically focussed FTSE 250 held on to the performance gap it opened up against its more international counterpart last week.

Perhaps more significantly UK 10-year gilt yields followed the lead downwards set by US bonds – a move suggesting that bond investors may be less moved by the tax row and its implications than the sometimes breathless headline writers in media newsrooms.

We may get a little more actual light next week with the expected publication of the Labour Party manifesto thought to be scheduled for Thursday 13th and likely the Conservative Party one around the same time.

Opinion polls

The chart above (at the top of this section) shows two sets of related data : the poll-of-polls average score for each of the four main parties shown on the left-hand scale and, on the right-hand scale, the projected majority for the Labour Party in Parliament based on those opinion polls – but applied at constituency level, not applied as a uniform swing nationally. That latter qualification refers to a polling technique called MRP which has proved more accurate than most in recent elections.

The implication remains as for last week and for some considerable time prior – long enough for markets no longer to be surprised: the polls continue to point to a record majority for Sir Keir Starmer’s “changed” Labour Party… now over 200 on this latest reading.

There is one new feature buried within the detail: since that last MRP update Mr Nigel Farage announced (on June 3rd) that he will - after all - stand as a candidate for the Reform Party. The effect on national polling was electric: a snap YouGov poll put the Reform Party on 17%, just 2 percentage points behind the ruling Conservative Party. If that result were to be projected onto the composition of Parliament it would cannibalise the government party numbers and produce an even greater majority for the Labour Party of over 300 seats!

But there is a flip-side to that same observation: in a fantasy scenario where a deal is done between Reform and the Conservative Party so that Reform effectively stands down all of its candidates and, in that same fantasy, that all reform voters then switch to Conservative then those same projection-algorithms point to a collapse in the Labour majority to around 20 MPs… not too far away from the hung-parliament territory that would give Mr Sunak everything to play for this far out from the actual election. To paraphrase an old adage: keep your fantasies close and your realities closer.

Andy Hartwill

Client Insights Lead

UK General Election: Week 1

It’s hard to believe that it has been only a little over a week since the UK general election was called - but then, they say a week’s a long time in politics and this first week is no exception. Party leaders were keen to hit the airwaves and photoshoots even at the risk of gaffes, defections and continuing rumblings from disaffected quarters of the main parties.

But for all of the unintended consequences, even here - in the foothills of each party’s campaign - the process is doing what it’s intended to do: to elucidate, if only a little, some of the details in as yet unpublished manifestos. So now we know for example that the Conservative Party, if re-elected, will increase modestly the tax-free state pension allowance (a so-called Triple Lock Plus); a Labour government, if elected, would not increase VAT - except on private school fees; the LibDems would extend free school meals to all primary school children; and Reform would increase national insurance rates for “foreign workers”.

Meanwhile financial markets remain broadly unmoved by the announcement or by the first week of campaigning. The UK’s FTSE100 index has eased back but then so too has an index of global equities where the concern seems more about possible further delays to cuts in interest rates from the USA, UK and EU. That said, the FTSE 250 index of more UK-focussed business performed a little better than it’s big brother global counterpart suggesting perhaps that investors take a more sanguine view over domestic UK prospects beyond the election.

That in turn would be in part a reflection of the commanding poll lead enjoyed by the Labour Party for some time now - certainly long enough for financial markets to factor into their forward pricing to some degree the scenario of a Labour government. Current polling continues to point to a Labour Party lead of over 20 percentage points and to a projection of a commanding Labour majority of almost 200 seats - bigger even than that of Mr. Tony Blair back in 1997.

As part of our continuing endeavours to offer clients our own elucidation of the policy proposals of and differences between the main political parties, Week 1 saw our flagship webinar, still available on demand, and the publication of a deep dive into how employment law might change under a Labour government committed to strengthening worker rights.

.

The webinar looked at a wide range of possible implications through a number of different lenses including those for financial markets, the UK energy market/ net zero and other infrastructure and a lens trained on the UK digital business landscape under Labour including of course AI.

Andy Hartwill

Client Insights Lead

In focus this week...

Labour commits to strengthening workers' rights

Global Insights: General Election 2024

Leasehold and Freehold Reform Act 2024

UK General Election: Week 0

It was the election announcement that was expected, sooner than expected: this week UK Prime Minister Rishi Sunak announced on the steps of Downing Street that the country would hold a general election on 4 July.

"Week 0" of the election saw a rush to pass a few final pieces of legislation before Parliament is prorogued and purdah rules take effect. Many bills that had been in the works for some time have had to be shelved, and it remains to be seen which if any will return after the election.

Of course, it was known well in advance that there would be a general election called at some point this year, and we have been examining the progression of UK government and opposition party policy through this lens for some time. Our tax experts have been tracking the development of the Labour Party's tax policies; Client Insights Lead Andy Hartwill has been producing his usual incisive analysis of recent fiscal events; and our Financial Institutions sector experts are keeping tabs on the progress of the Edinburgh Reforms, which form a key plank in the current government's economic policy prospectus.

In focus this week...

Labour's tax plans

Budget 24: Market View

The Edinburgh Reforms

Further analysis

Global Insights call

Interested in what the UK election means for the global economy? Listen back to our Global Insights call from 29 May.

Meet Searchlight

Simmons experts track upcoming legislative and regulatory change so you don’t have to. Book your Searchlight demo today.

Key contacts

If you have any questions, contact a member of the UK General Election 2024 team for assistance: