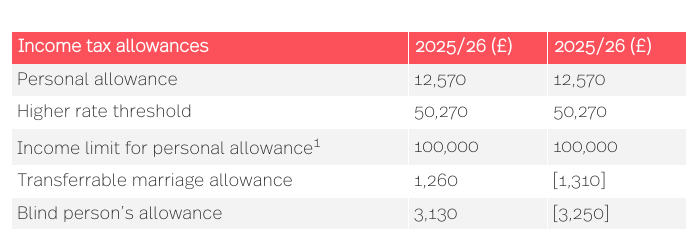

1 The individual’s personal allowance is reduced where their income is above this limit. The allowance is reduced by £1 for every £2 above the limit.

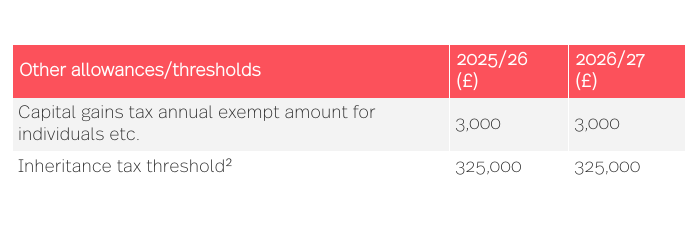

2 The inheritance tax threshold is increased to £500,000 where the estate includes a residence passed to direct descendants and the entire estate is worth less than £2 million.

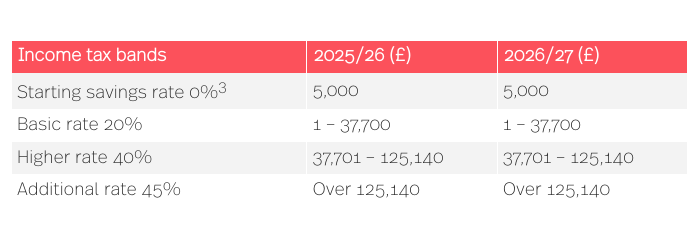

3 If non-savings taxable income exceeds the starting rate limit, the starting savings rate will not apply to savings income.

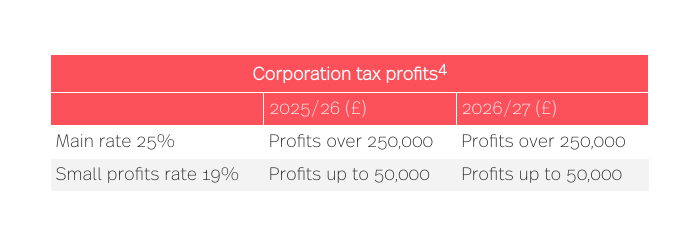

4 For businesses with profits between £50,000 and £250,000, tax is charged at the main rate, subject to marginal relief provisions which will provide a gradual increase in the effective corporation tax rate.

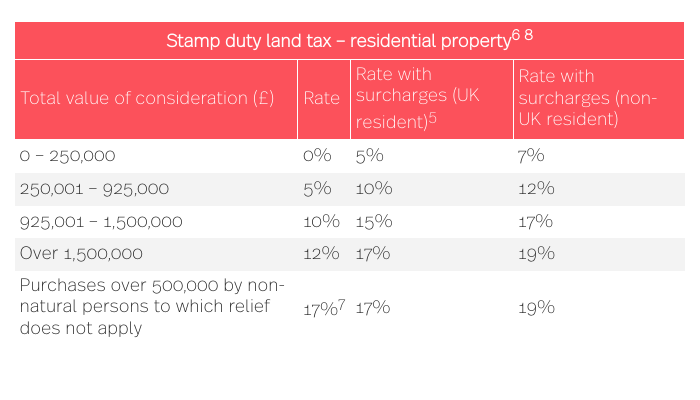

5 Stamp duty land tax is charged with a surcharge of 5% above the usual stamp duty land tax residential rates from 31 October 2024 on purchases by individuals of additional residential properties (such as second homes and buy-to-let properties), and by non-natural persons (companies, partnerships including companies or collective investment schemes) of dwellings, even if they do not own another dwelling.

6 From 1 April 2025, for purchases by first-time buyers of property worth £500,000 or less, the stamp duty land tax rate for a property valued £0 – 300,000 is 0% and for a property valued £300,001 – £500,000 is 0% on the consideration up to £300,000 and 5% on the remainder.

7 The 17% rate applies to certain acquisitions of dwellings worth more than £500,000 by “non-natural persons” (a company, a partnership including a company or a collective investment scheme), though in many cases a relief is available from this flat rate.

8 A 2% surcharge applies on purchases by non-UK residents acquiring dwellings in England and Northern Ireland (when combined with the additional 5% rate (see note 5 above), a 7% surcharge applies on non-UK residents purchasing additional residential properties).

This document (and any information accessed through links in this document) is provided for information purposes only and does not constitute legal advice. Professional legal advice should be obtained before taking or refraining from any action as a result of the contents of this document.

Key contacts

If you have any questions, contact a member of the HMRC rates and allowances team for assistance: