Using the Netherlands in structuring Chinese outbound investments

This article explains the benefits of using the Netherlands in structuring outbound Chinese investments, in particular.

Introduction

The Dutch tax system has many features that make the Netherlands a favourable jurisdiction for establishing an international holding company. Examples include the participation exemption (where dividends and capital gains on the sale of shares in (foreign) subsidiaries are fully exempt from Dutch corporate income tax), the absence of withholding taxes on outbound interest and royalty payments, the possibility of obtaining Advance Tax Rulings (ATRs) and Advance Pricing Agreements (APAs) from the Dutch tax authority and an extensive double tax treaty network. In addition, the Dutch bilateral investment treaties (BITs) network can offer an important incentive for setting up an intermediary holding company in the Netherlands. These features make the Netherlands an attractive holding jurisdiction for the structuring of Chinese outbound investments.

Structure with Chinese investment through the Netherlands

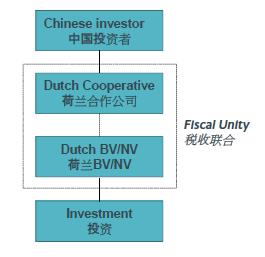

The first step towards taking advantage of the favourable Dutch tax regime is to incorporate a Dutch holding company (Dutch Holdco). In principle, there are three types of holding entities available: (i) a limited liability company (besloten vennootschap or BV); a public company (naamloze vennootschap or NV); or a Dutch Cooperative (coöperatie). Currently, a Dutch Cooperative is the most popular holding company entity in international structures given that any profit distributions made by a Dutch Cooperative are, if properly structured, not subject to dividend withholding tax in the Netherlands (whereas dividend distributions made by a Dutch BV/NV are, in principle, subject to 15% Dutch dividend withholding tax, unless reduced under a double tax treaty). The Dutch State Secretary of Financa has announced proposals to introduce new rules removing the difference in dividend withholding tax treatment between Dutch cooperatives an BV/NVs. The announced proposal is further discussed under the heading "Dutch Cooperative".

Under current application of the law, in certain circumstances, both a Dutch Cooperative and a Dutch BV/NV should be included in a structure. This is because certain double tax treaties only provide for the application of the lowest withholding tax rate where the capital of the recipient of the dividends is divided into shares (unlike a Dutch BV/NV, the capital of a Dutch Cooperative is not divided into shares). Further, if the Dutch Cooperative or Dutch BV/NV has profited from other activities (for example the granting of loans), this creates an additional opportunity for setting off withholding tax levied on income derived from such investment against the profits of either the Dutch Cooperative or the Dutch BV/NV. The investment structure can be illustrated as follows:

Dutch Cooperative

A Dutch Cooperative is an entity which has legal personality. Unlike a Dutch BV/NV, a Dutch Cooperative does not have owners or shareholders, but (at least two) Members which are entitled to a share of its profits. It is permissible for one of the Members to have a 99.99% economic interest in the Dutch Cooperative and for the other (eg a related entity of that Member) to have a marginal (eg 0.01%) economic interest in the Dutch Cooperative, so that, in practice, one Member is entitled to all income generated by the Dutch Cooperative. Generally, the Dutch Cooperative has full access to the Dutch participation exemption regime, the extensive Dutch double tax treaty network and the EU Directives.

To prevent abuse of the Dutch Cooperative, Dutch tax legislation contains anti-abuse provisions levying Dutch dividend withholding tax (DWT) on distributions made by Dutch Cooperatives where there are no sound commercial reasons for interposing the Dutch Cooperative as holding vehicle, and the main purpose or one of the main purposes of the Dutch Cooperative is to avoid the levy of DWT or foreign tax payable by another person.

On 20 September 2016 the Dutch State Secretary of Finance sent a letter to parliament in which he proposed to remove the different in DWT treatment between cooperatives and BV/NVs.

The letter proposes to introduce a new rule under which a profit distribution made by a so-called "holding cooperative" (broadly a cooperatives whose activities comprise holding participations or portfolio investments in or financing of related companies) to a member with a stake of 5% or more, will become subject to DWT at a rate of 15%. However, an exemption from DWT will be introduced where the relevant member of the cooperative is a resident of the EU or of a country which has concluded a double tax treaty with the Netherlands, provided there is no abuse (broadly, where there is an active business). This is in line with the starting point that profit distribution up the chain in active business structures should not be hindered by the levy of withholding tax.

The letter in addition suggests that an exemption from DWT tax will also be introduced for a profit distribution made by a public or private limited liability company to a shareholder with a 5% or greater shareholding, if the relevant shareholder is a resident of a country which has concluded a double tax treaty with the Netherlands and provided there is no abuse. As a result, the exemption from DWT tax will be extended to a profit distribution made by a BV/NV to a 5% shareholder resident in the People's Republic of China.

The letter states that any proposed changes are not intended to become effective before 01 January 2018. Accordingly, there should be sufficient time to anticipate any changes to Dutch dividend withholding tax affecting holding company structures in the Netherlands which involve a cooperative.

Favourable Dutch tax regime

Participation exemption

A Dutch Holdco is eligible for an exemption from Dutch corporate income tax (CIT) under the so-called participation exemption in respect of dividends received and capital gains realised upon the disposal of shareholdings in qualifying participations. This is of benefit to a Chinese investor as profits distributed by a subsidiary held through a Dutch Holdco are not subject to CIT in the Netherlands.

The participation exemption applies if:

- Dutch Holdco holds at least 5% of the nominal paid up capital of the (foreign) subsidiary, and

- the (foreign) subsidiary does not qualify as a "low taxed investment participation" (laagbelaste beleggingsdeelneming).

Participation in a company is not qualified as a low taxed investment participation if the (foreign) participation meets one of the following tests:

- the (foreign) subsidiary it is not held as a portfolio investment (the "motive test")

- the (foreign) subsidiary is subject to a profit tax resulting in an effective tax rate that is considered realistic judged by Dutch standards (ie 10%) (the "subject to tax test") or less than 50% of the assets of the (foreign) subsidiary comprise passive investments (the "asset test").

In addition to the benefits offered by the Dutch participation exemption regime, dividend, royalty and interest payments received by Dutch Holdco from subsidiaries within the European Union are generally exempt from withholding tax under the EU Parent Subsidiary Directive and EU Interest and Royalties Directive, subject to certain conditions being met.

Taxation of a substantial interest in Dutch Holdco

The Chinese investor is only subject to Dutch CIT on (certain forms of) Dutch source income. Taxable Dutch source income includes benefits derived from a so called "substantial interest" (ie an interest of 5% or more) in a Dutch Holdco, but only if "substantial interest" is being held to avoid the levy of DWT or foreign tax payable by another person, and there are no sound commercial reasons for interposing the Dutch Cooperative as holding vehicle. If properly structured, the Chinese investor should not be subject to Dutch CIT derived from a substantial interest in Dutch Holdco.

Double tax treaty benefits

The Netherlands has one of the most extensive double tax treaty networks in the world, comprising tax treaties with over 90 countries. These double tax treaties provide for (inter alia) a reduction, or even an exemption from, withholding tax levied on inbound dividend, interest and royalty payments. The Netherlands itself does not levy any withholding tax on outbound interest and royalty payments.

On 01 January 2015, a new tax treaty between China and the Netherlands has entered into force. The new treaty reduces the DWT rate from 5% provided that the shareholder is the beneficial owner and directly holds at least 25% of the capital in the company paying the dividend. A 0% DWT rate applies if the beneficial owner is (in)directly state-owned.

Advance tax rulings/advance pricing agreements

Chinese investors can generally obtain an ATR from the Dutch tax authority which provides Chinese investors with advance certainty about their (future) Dutch tax position in relation to international structures. For example, it is possible to obtain an ATR confirming that income (including capital gains) from shareholdings held by a Dutch Holdco in (foreign) subsidiaries is exempt from Dutch corporate income tax under the participation exemption. In addition, Chinese investors can obtain advance certainty in the form of APAs that transactions between related entities are considered at arm’s length for Dutch tax purposes. Note that on 01 January 2017, new legislation will enter force that allows the Dutch tax authorities to automatically exchange certain ATRs and APAs with other EU-member states.

Bilateral investment treaties (BITs)

In addition to the extensive Dutch double tax treaty network, Chinese investors who interpose a Dutch Holdco in their structure may benefit from multiple BITs concluded by the Netherlands with other countries. These BITs safeguard cross-border investments made through a Dutch Holdco within the country of the relevant BITs partner(s). Furthermore, Dutch BITs typically provide for free transfer of funds, fair and equitable treatment, protection against discriminatory treatment and an entitlement to compensation in the event that an investor’s assets are expropriated by a foreign government. Other major advantages of BITs include (in principle) direct access to international arbitration. In the Dutch BIT with China, investors may opt for either the International Centre for the Settlement of Investment Disputes (ICSID) or ad hoc arbitration under the United Nations Commission on International Trade Law (UNCITRAL) arbitration rules.

Summary

The Netherlands is an attractive jurisdiction through which Chinese investors can route their investments. A Dutch Holdco benefits from the favourable Dutch tax regime, including the participation exemption, the absence of withholding taxes on outbound interest and royalty payments, the possibility of obtaining an ATR and APAs from the Dutch tax authority and the extensive Dutch double tax treaty network. Furthermore, investments through a Dutch Holdco may be protected by BITs depending on the jurisdiction the investment is made in.

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)