Introduction

Foreign investors in Dutch companies benefit in certain circumstances from an exemption from Dutch dividend withholding tax (statutory rate of 15%) in respect of Dutch dividends. Since 2018 this exemption applies, broadly, where companies based in the EU/EEA or a treaty country, hold at least 5% of the shares in the Dutch company and there is no abuse. The withholding tax exemption is important because the dividend withholding tax regularly forms a final cost to investors and therefore reduces their return on investment.

When will there be abuse? In brief, this will be the case if the shareholder: (1) holds the interest in the Dutch company with the principal purpose or one of the principal purposes being to avoid tax (subjective test) and (2) holds the interest in the Dutch company as part of an artificial arrangement or transaction (objective test). The abuse test must be interpreted in accordance with Dutch and EU law.

The objective test is of great importance when setting up investment structures and is one of the topics of an important judgment of the Amsterdam Court of Appeal of 2 June 2022. The ruling has been appealed to the Supreme Court, so we are still awaiting a final judgment in this case.

Amsterdam Court of Appeal

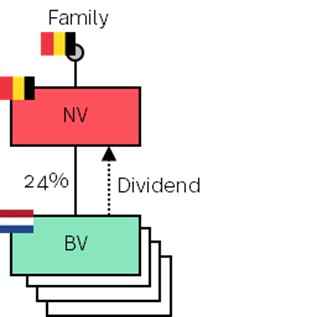

The case involved a Belgian investment company ("NV") owned by a Belgian family and which holds approximately 18 minority and majority interests, including a 24% interest in a Dutch company ("BV") (see the diagram below). NV holds its interest as a parallel investor alongside a private equity fund.

In 2018, NV received a dividend from BV. The board of NV received a management fee for (management) activities in respect of its shareholdings. Salary and other expenses incurred by one of the shareholders in respect of legal and administrative services rendered to NV were charged to the NV. NV has neither an office nor its own staff. Work on behalf of NV is performed from a dedicated room in the home of one of the shareholders.

NV claimed to be entitled to the withholding tax exemption in relation to the 2018 dividend. The inspector disagreed, but the (lower) Court agreed with NV: NV is incorporated in the country of the ultimate shareholders and, given the scope of its activities and the associated management costs, it runs an enterprise to which the interest in BV also belongs. This led to the conclusion that there is no artificial structure.

The Court of Appeal of Amsterdam arrived at a different conclusion and found that the Court wrongfully applied an overall approach with regard to the objective test: the Court should not have looked at the (management) activities that took place for all participations as a whole, but specifically at the relationship between NV and the 24% minority interest in BV. NV did not perform any (management) activities specifically (considered in isolation) with respect to the 24% interest (it merely holds the shares). The Court of Appeal therefore concluded that NV was artificially interposed between the Belgium family and the BV. Consequently, the objective test was met and NV was not eligible for the withholding tax exemption.

Observations

The Court and the Court of Appeal based their conclusions on the same case law and regulations, but reached different conclusions. NV in this case constitutes for the family an investment platform from which, in a general sense, management activities with respect to (a number of) participations are carried out. One of the questions now, in the context of the objective test, is whether the specific relationship between NV and BV should indeed be considered in isolation or whether it is sufficient that, overall, there are business or commercial activities. It remains to be seen how the Supreme Court will rule on this issue.

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)