Background

On 19 December 2024, The Stock Exchange of Hong Kong Limited (Exchange) published a consultation paper (Consultation Paper) in relation to the proposals to optimise the price discovery process for IPOs, with a particular aim to minimise situations where the final offer price being set significantly differ from the actual trading price upon listing, and to review open market requirements, including public float requirements and free float requirements, with an aim to attract more high quality new listing applicants to consider listing in Hong Kong.

The Consultation Paper was published following discussions with relevant stakeholders, including representatives from investment banks, institutional investors, private equity firms, retail brokers, and both prospective and existing listed issuers. The Exchange has considered the key views and comments made by the stakeholders during these discussions when coming up with the proposals set out in the Consultation Paper.

The consultation period will end on 19 March 2025.

Key proposals

Calculation of public float

Public float percentage calculation: Currently, when an issuer calculates its public float percentage, the percentage of shares held by the public is determined using its total number of issued shares as the denominator, regardless of whether such shares are listed on any regulated market or not. Separately, for PRC issuers whose A shares are listed on a PRC stock exchange, such A shares, which are typically in the same class as its H shares, are also included in the numerator when calculating the public float percentage, despite such shares are not fungible with the H shares listed on the Exchange.

To better reflect the shares that contribute to an open market in Hong Kong, the Exchange proposes to revise the basis for calculating the minimum prescribed percentage of public float by aligning with international standards, while ensuring the amount of shares sought to be listed in Hong Kong is sufficiently large to represent a meaningful proportion of all shares in issue and to attract a critical mass of investor interest:

- In general, the public float percentage will be calculated by reference to the total number of securities of the class that is listed only.

- For PRC issuers which have A shares listed on a PRC stock exchange which are in the same class as the H shares to be listed, such A shares will only be included in the denominator, but not the numerator.

- For issuers with other share class(es) listed overseas, the public float percentage will continue to be calculated by reference to the total number of issued shares of all classes, while only shares of the class for which listing is sought in Hong Kong will be included in the numerator.

Definition of “the public”: The Exchange proposes to amend the definition of “the public” under both the Rules Governing the Listing of Securities on the Exchange (Main Board Listing Rules) and the Rules Governing the Listing of Securities on the GEM of the Exchange (GEM Listing Rules, together with the Main Board Listing Rules, the Listing Rules) to exclude any person whose acquisition of shares has been financed directly or indirectly by, or at the instructions of, the issuer itself from the definition.

Initial public float

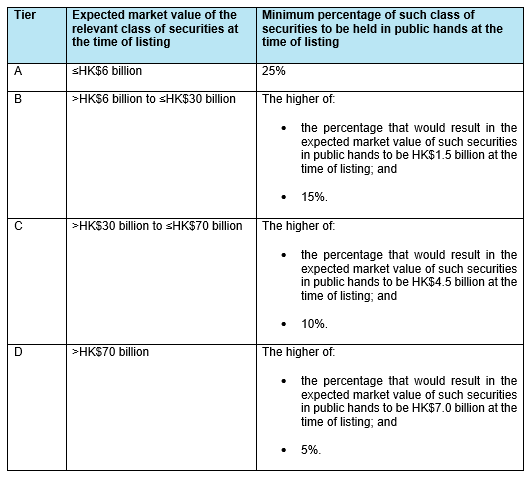

Tiered initial public float thresholds: The Exchange recognises that the existing initial public float thresholds are relatively high compared to other major international stock exchanges, which may drive away some potential applicants from choosing Hong Kong as their listing venue. The Exchange is also concerned that the existing case-by-case waiver approach may present uncertainties to new listing applicants, especially for mega cap issuers. The Exchange therefore proposes to replace the existing initial public float thresholds with the following tiered structure:

Ongoing public float

Ongoing public float requirements and OTC market: The Exchange notes that some other major international stock exchanges have in play ongoing public float thresholds that are less stringent than those they require at initial listing. In general, the ongoing public float thresholds adopted by these counterparts are also lower than that of the Exchange. It is recognised that the current ongoing public float requirements may unduly restrict transactions, even in situations where such transactions would be in the interests of the issuer and its shareholders. To mitigate the potential adverse effects including costly public float restoration obligations borne by the issuers and the shareholders’ deprived ability to trade in situations where trading is suspended due to breaches of the ongoing public float requirements, the Exchange is seeking feedback on:

- whether the ongoing public float requirements should be less stringent than the initial public float requirements;

- whether the existing regulatory approach of suspending trading of issuers which breached the ongoing public float requirements should be maintained; and

- whether an OTC market should be established in Hong Kong to allow the trading of delisted securities.

Ongoing public float disclosure: The Exchange proposes to require listed issuers to disclose in their annual reports:

- their public float percentage; and

- the composition of ownership of the relevant class of shares listed on the Exchange, with the groups of shareholders being identified using public information that is available to the issuers and within the knowledge of their directors.

Free float requirement

Initial free float requirement: Currently, the Exchange has no requirement for issuers to ensure that a certain portion of its shares are free from disposal restrictions. Despite the existing initial public float requirement, the Exchange recognises the risk that some issuers may have a low free float percentage which limits the liquidity of their shares. The Exchange proposes to align with the major international stock exchanges and introduce an initial free float requirement for new listing applicants to ensure that their free float in public hands either:

- represents at least 10% of the number of shares in the relevant class for which listing is sought, with an expected market value of at least HK$50 million; or

- has an expected market value of at least HK$600 million at the time of listing.

Proportion of shares A+H issuers must list in Hong Kong

Initial minimum percentage and market value of shares: The Exchange proposes to lower the threshold for the initial minimum percentage of shares to be listed on the Exchange in terms of the issuer’s total number of issued shares,

- for a new applicant that is a PRC issuer with other listed shares, H shares for which listing is sought on the Exchange must, at the time of listing, either (i) represent at least 10% of the total number of shares in the class to which H shares belong (excluding treasury shares), or (ii) have an expected market value of at least HK$3 billion;

- for a new applicant that is an issuer with other share class(es) listed overseas, the class of shares for which listing is sought on the Exchange must, at the time of listing, either (i) represent at least 10% of the total number of issued shares (excluding treasure shares), or (ii) have an expected market value of at least HK$3 billion.

Cornerstone investment

Regulatory lock-up on cornerstone investment: The Exchange recognises that regulatory lock-up requirement on cornerstone investors are unique from international standard. It is explained in the Consultation Paper that the Exchange believes that there is a need for a regulatory lock-up requirement such that the cornerstone investors can demonstrate to other potential investors their confidence in the IPO issuer. In order to mitigate the potential share price volatility upon lock-up expiry, the Exchange is seeking feedback on whether:

- to retain the current lock-up period of at least six months upon listing for cornerstone investors; or

- to allow a staggered lock-up release arrangement such that 50% of the IPO securities placed to cornerstone investors could be released after three months upon listing, with the remainder being released after six months upon listing.

Allocation of IPO securities

Minimum allocation to the placing tranche: To optimise IPO price discovery and mitigate the chances of mispricing, the Exchange proposes to:

- introduce a requirement that at least 50% of the total number of shares initially offered in an IPO prior to the exercise of any over-allotment option or offer size adjustment option be allocated to investors in the bookbuilding placing tranche; and

- remove the guideline that there should not be less than three holders for each HK$1 million of the placing, with a minimum of 100 holders in an IPO placing tranche.

Allocation to the public subscription tranche: The Exchange proposed to replace the existing minimum allocation of offer shares to the public subscription tranche, of which it considers no longer strongly justified in light of the change in investor composition in the Hong Kong market which shows that retail investors are only contributing a small proportion of cash market activity now, with the following requirements. A listing applicant would be allowed to adopt one of the two mechanisms below:

- a fixed initial allocation of 5% of offer shares to the public subscription tranche, with clawback mechanism which could increase such allocation to up to 20%; or

- a minimum initial allocation of 10% of offer shares to the public subscription tranche with no clawback mechanism.

Pricing

Pricing flexibility mechanism: The Exchange proposes to provide more pricing flexibility by allowing an issuer to adjust the final offer price upward, to up to 10% above the indicative offer price or the top of the offer price range, without being required to first cancel its IPO and relaunch it at the revised price alongside a supplemental or new prospectus. The Exchange also seeks feedback on, if a listing applicant adopts the pricing flexibility mechanism proposed above, whether the applicant should:

- continue to be able to set the top of the initial offer price range at not more than 30% of the bottom of that range; or

- narrowing down the range of which it can set to a price at not more than 20% of the bottom of that range.

Conclusion

The Exchange’s initiative reflects a strategic move to enhance Hong Kong’s competitiveness as a global financial hub by proposing adjustments to the IPO framework and ongoing market requirements. By suggesting a pricing flexibility mechanism that allows upward adjustment of the final offer price without necessitating a relaunch of the IPO, and by revising the allocation mechanisms for IPO securities to better accommodate current market dynamics, the Exchange seeks to foster a more dynamic, transparent, and efficient market. These proposed changes, open for consultation until 19 March 2025, aim to mitigate the risk of significant price variation post-listing, ensure a meaningful representation of shares in the public’s hand, and enhance the overall liquidity and attractiveness of the Hong Kong stock market to both issuers and investors.