Background

The Stock Exchange of Hong Kong Limited (Exchange) published a consultation paper on 26 September 2023 proposing to introduce listing reforms for GEM (Proposed Reforms) and to request market feedback on proposed changes to the Exchange's Main Board and GEM Listing Rules (Listing Rules). The consultation period will end on 6 November 2023.

The Proposed Reforms were made in response to decreasing capital raising activities on GEM, where the number of new listings and the funds raised have seen significant decline. The Exchange cited that a broad range of stakeholders have reflected that the existing GEM listing regime is not favourable for small and/or medium-sized enterprises (SMEs). It has been generally considered that the cost of GEM listing is particularly high for SMEs when compared with the funds raised at listing and the continuing obligations of GEM issuers are onerous and accordingly discouraging. The positive cash flow requirement has further prevented companies with high research and development (R&D) expenses from listing on GEM.

Key Features of the Proposed Reforms

In view of the above, the Exchange under the Proposed Reforms proposed the following three major revisions for GEM, namely to introduce (i) a new alternative financial eligibility test for GEM listing, (ii) a new streamlined transfer mechanism to the main board of the Exchange (Main Board), and (iii) alignment of continuing obligations for GEM issuers with those for Main Board issuers.

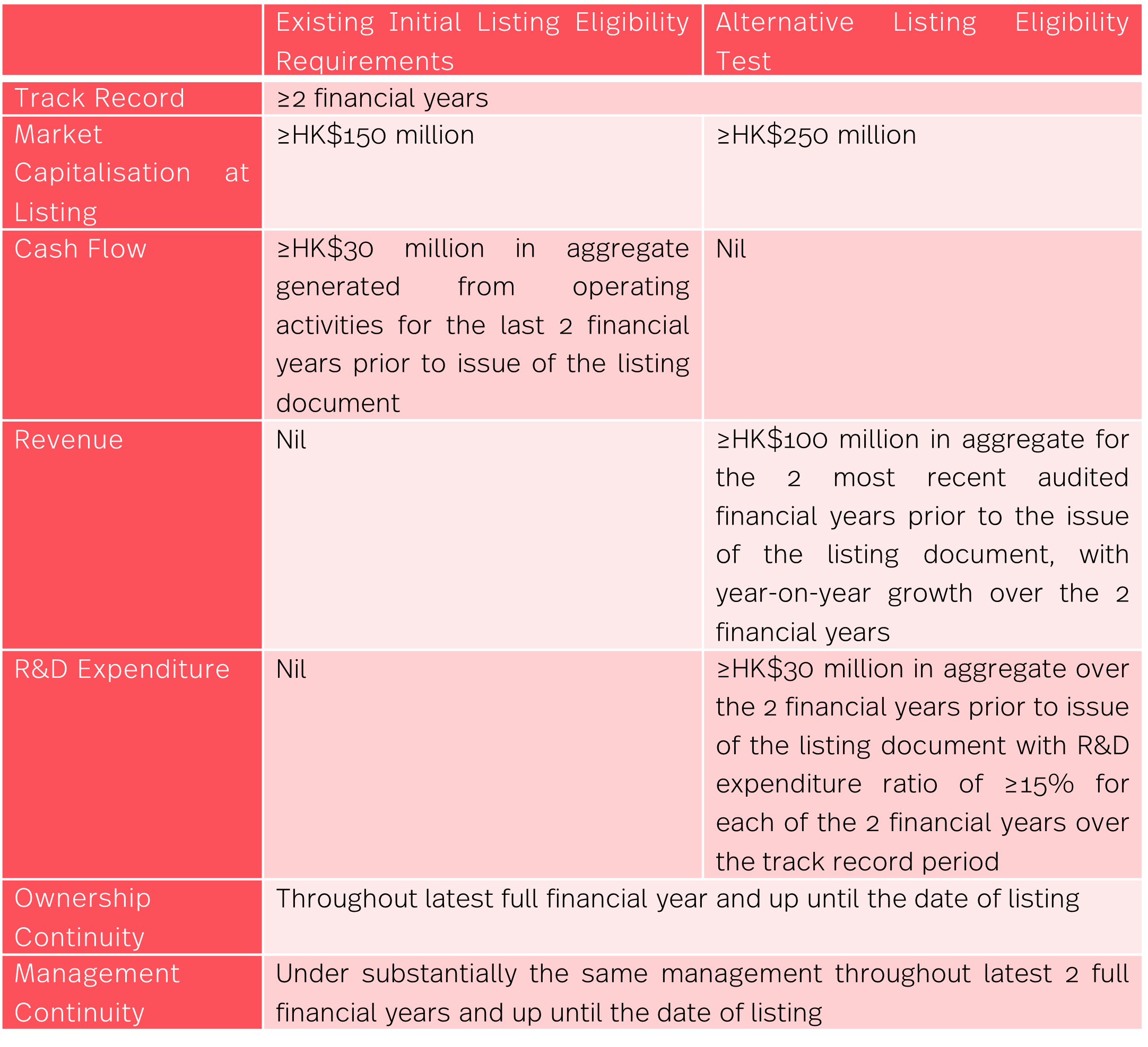

Alternative Financial Eligibility Test

The Exchange recognises that the existing listing eligibility requirements may prevent the listing of research-intensive businesses which engage heavily in R&D activities because of their lack of a track record of positive operating cash flow. In this connection, the Exchange proposes to introduce a new pathway to listing with an alternative financial eligibility test, as set out in the table below:

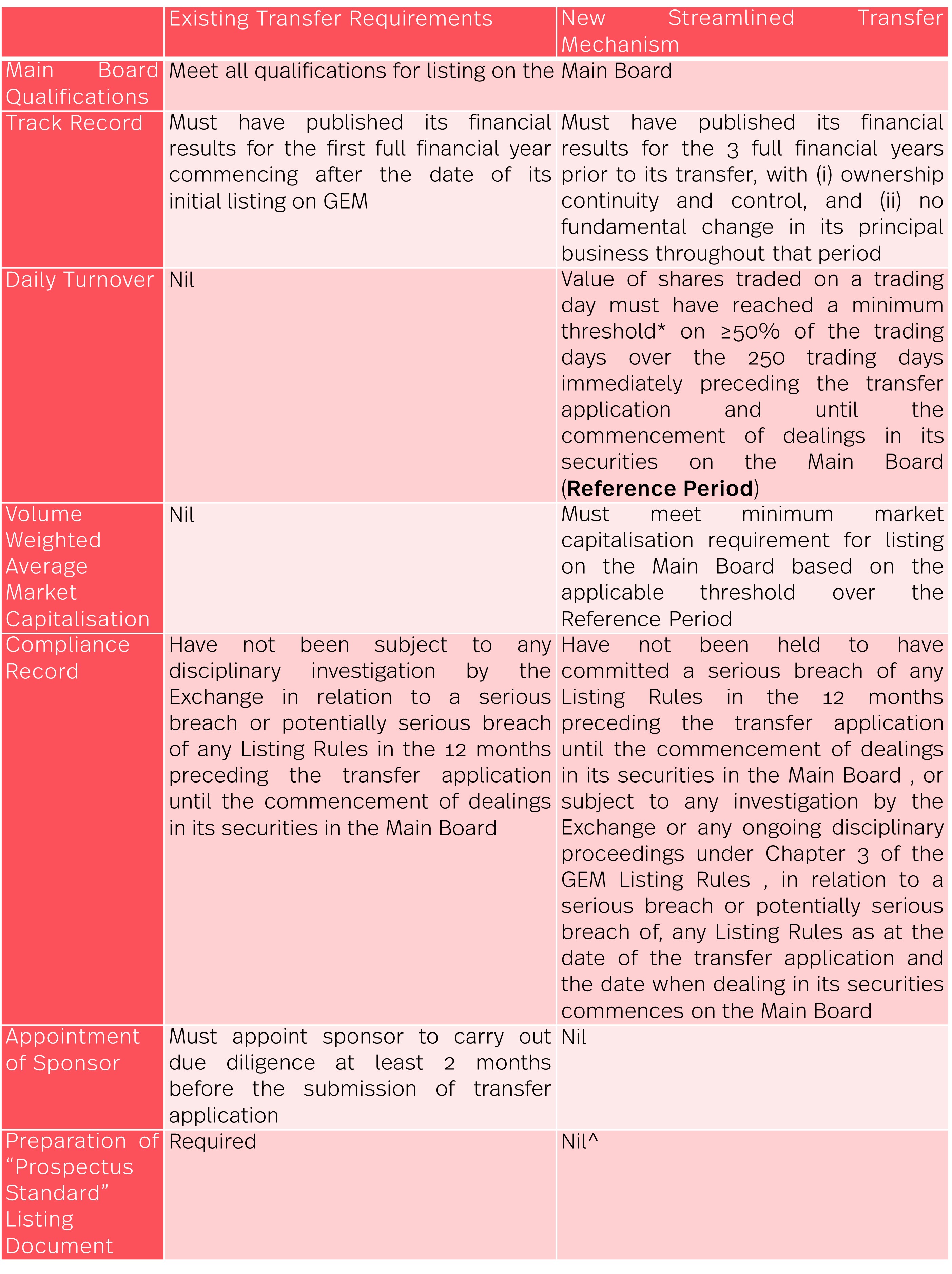

New Streamlined Transfer Mechanism

The Exchange proposes to re-introduce a streamlined transfer mechanism for the transfer of GEM issuers to the Main Board (New Streamlined Transfer Mechanism), with modifications from the predecessor streamlined process which was abolished in 2018. The requirements of the New Streamlined Transfer Mechanism are set out below:

*The threshold is proposed to be set at either HK$50,000 or HK$100,000.

^A transfer applicant will instead be required to submit (i) a formal application for listing, (ii) an advanced draft public announcement of the transfer for pre-vetting by the Listing Division, and (iii) a working capital sufficiency statement with relevant supporting information.

Under the Proposed Reforms, GEM issuers that cannot meet the requirements of the New Streamlined Transfer Mechanism must apply for transfer pursuant to the current requirements.

Continuing Obligations

The Exchange proposes to bring the continuing obligations of GEM issuers in line with those for Main Board issuers. Major proposed changes in continuing obligations include:

- Removal of quarterly reporting requirement: GEM issuers will instead be required to comply with semi-annual reporting obligations. Quarterly financial reporting will instead be a recommended best practice in GEM's Corporate Governance Code; and

- Revised timeframe of annual reports, interim reports and preliminary announcements of results for first half of financial year: (i) annual reports are to be published not later than 4 months after the end of each financial year; (ii) interim reports to be published not later than 3 months after the end of the first 6 months of each financial year; and (iii) preliminary announcements of results for the first 6 months of each financial year to be published not later than 2 months after the end of that 6 month period.

Conclusions

The Proposed Reforms mark the Exchange's effort in revitalising GEM and its commitment to SMEs in providing a platform for their fundraising. With the expected cost efficiency and the availability of the new alternative eligibility pathway, it is believed that the Proposed Reforms would increase the attractiveness of GEM to SMEs and provide broader investment options for investors, whilst maintaining market quality and investor protection.

.jpg?crop=300,495&format=webply&auto=webp)