FCA Consumer Duty consultation

Principle 12: four outcomes, three cross-cutting rules, two months to respond and a brand new Consumer Duty.

The FCA’s second consultation paper CP 21/36 was published on 7 December 2021. The FCA intends to raise standards and expectations with the introduction of the new Consumer Duty. The FCA wants a “reset” around a new Principle (#12), backed up by assertive supervisory and enforcement action.

Find out how we can help you implement the FCA’s consumer duty.

Key Elements

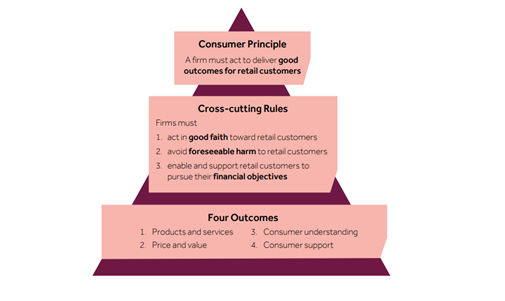

The Consumer Principle will be FCA Principle 12 that “a firm must act to deliver good outcomes for retail customers”

Principles 6 and 7 will be disapplied when Principle 12 applies

There will be a new Individual Conduct Rule 6 in COCON requiring conduct rules staff to act to deliver good outcomes for retail customers, together with guidance on the new rule

There is a tripartite structure with the Principle, Cross Cutting Rules and Four Outcomes.

There is a concept of reasonableness which runs through the Duty. – it is the standard that could reasonably be expected of a prudent firm:

- carrying on the same activity in relation to the same product or service; and

- with the necessary understanding of the needs and characteristics of its customers

The need for “all reasonable steps” has been deleted from the Cross-cutting Rules.

The perimeter of regulated advice is unchanged - where a customer has a non-advised service, the FCA would not expect firms to provide advice.

There will be no Private Right of Action (for now….)

A firm’s governing body is required to receive a report at least annually on compliance with the Duty and to agree any actions required

Timing

Comments are requested by 15 February 2022 with a final Policy Statement and new rules to be published by 31 July 2022, in line with the requirements of the Financial Services and Markets Act 2021.

The proposed implementation period is 9 months, giving firms until 30 April 2023 to implement the new Consumer Duty in full. This is likely to be far too short for some firms and the FCA is keen to hear views on the appropriate length of the implementation period. There is also a suggestion that implementation will be “iterative” with the FCA giving further guidance as it sees firms take steps to implement the Duty, although it is not entirely clear when this would start or end.

Scope

Some good news is that, having taken on board feedback, the FCA proposes to align the scope to existing modules of the Handbook. Broadly speaking, the scope of the Duty will follow the respective application positions (and any specific exclusions) in modules such as ICOBS, MCOB, BCOBS etc.

This means that firms’ existing retail product mapping can be used.

It also means that, for example, certain financial promotions to high net worth customers will be out of scope. But, generally, the Duty will apply to dealings with high net worth customers.

Territorially, the Duty will apply to activities carried on with retail customers located in the UK unless another applicable rule or onshored regulation which is relevant to the activity has a different territorial scope, in which case that different territorial scope applies. Again, this seeks to align scope to existing perimeters.

The FCA also proposes to exclude primary market activities in relation to “real economy securities” (ie plain vanilla equity and debt issuances to retail by corporates).

The back book

The Duty will apply, on a forward-looking basis, to existing products and services which are still being sold or renewed. Such products and services will have to be brought into the new, expanded product governance processes.

It will also apply, on a forward-looking basis, to existing products/services that are “closed” (ie no further sales or renewals) where the products/services are not meeting the cross-cutting rules, in which case firms may need to take action to mitigate any harm.

Firms will therefore need to assess and monitor their back book.

However, the FCA would not expect firms to apply rules that are not relevant for “closed” products or services. For example, there would be no need for manufacturers to identify a target market or develop a distribution strategy.

The Consumer Duty structure

The overall tripartite Structure remains unchanged, but the wording of the Principle has been determined, the wording of the Cross-cutting Rules has been revised and the Four Outcomes have been re-ordered and partly renamed.

Data and management information

It will not be possible to implement and live with the Consumer Duty unless supported with appropriate data-gathering and management information. This reflects the FCA’s own Transformation Programme into becoming more data-led.

Data will underpin almost every aspect of the Consumer Duty and the FCA gives a list of examples in the CP of the kinds of data an MI that are likely to be needed. To quote the FCA (emphasis added):

“Firms would need to assess and evidence the extent to which and how they are acting to deliver good outcomes.”

This is likely to mean that many firms will need to review their data-gathering and record-keeping arrangements. Ultimately a firm’s compliance with the Consumer Duty will stand or fall on the basis of what it can demonstrate in terms of evidence, data and records.

Further information

We have prepared a briefing on more detailed aspects of the CP, in particular the Cross-cutting Rules and the Four Outcomes, as well as on the likely shape of implementation and the practical considerations that arise out of the second CP.

Please contact us if you would like to discuss these aspects.

_11zon.jpg?crop=300,495&format=webply&auto=webp)