HKEX Proposes to Raise Main Board Profit Requirement

Consultation paper outlines proposals to increase profit requirement by 150% or 200% for new listings on Main Board.

Background

The Stock Exchange of Hong Kong Limited (Exchange) published a consultation paper on 27 November 2020 proposing to increase the profit requirement under Main Board Listing Rule 8.05(1)(a) (Profit Requirement) for new listings on its Main Board. The consultation period will end on 1 February 2021.

The Profit Requirement has remained unchanged since 1994, while the minimum expected market capitalisation at the time of listing under Main Board Rule 8.09(2) (Market Capitalisation Requirement) was increased from HK$200 million to HK$500 million back in 2018.

The Exchange has proposed to raise the Profit Requirement to align with the increased Market Capitalisation Requirement introduced in 2018. The Exchange also aims to distinguish between issuers listed on GEM and the Main Board to position the Main Board as the main market to attract sizeable companies that can meet high market standards. The Exchange also believes that the proposed increase will improve the overall quality of Main Board issuers.

The Exchange said that its proposal follows its observations after the increased Market Capitalisation Requirement, where it saw an increase in listing applications from small cap issuers with proposed market capitalisation upon listing of HK$700 million or less, but only marginally met the current Profit Requirement, resulting in relatively high historical P/E ratios as compared to those of their listed peers. In particular, many such small cap issuers failed to meet their profit forecasts post-listing, leading to regulatory concerns over the reasonableness of their valuations. The Exchange is particularly concerned that their valuations were not supported by genuine expectation of growth, but were simply reverse engineered to meet the Market Capitalisation Requirement to manufacture potential shell companies for sale after listing.

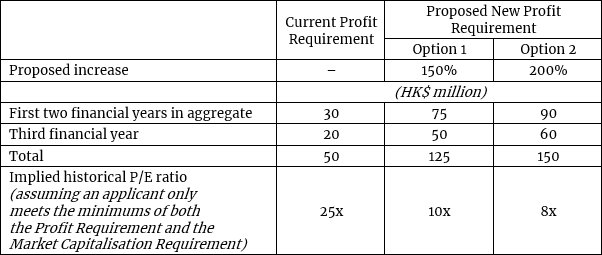

Proposal

The Exchange has proposed two options to increase the Profit Requirement:

Option 1: Based on the percentage increase in the Market Capitalisation Requirement, matching it by increasing the Profit Requirement by 150%.

Option 2: Based on the approximate percentage increase in the average closing price of the Hang Seng Index from 1994 to 2019, matching it by increasing the Profit Requirement by 200%.

The table below summarises two options for the proposed new Profit Requirement:

Temporary Relief

Considering that the businesses of many potential applicants may be adversely affected by market conditions in 2020, in particular the COVID-19 pandemic, the Exchange will consider granting temporary relief on a case-by-case basis from the proposed increased Profit Requirement if an applicant meets the following conditions:

its aggregate profit during the track record period meets the aggregate profit threshold (i.e. HK$125 million under Option 1 or HK$150 million under Option 2);

it had positive cash flow generated from operating activities in the ordinary and usual course of business before changes in working capital and taxes paid in the last financial year during the track record period;

it demonstrates that the conditions and circumstances leading to its inability to meet the profit spread in the increased Profit Requirement are temporary;

the track record period must have at least consecutive six months that fall within the calendar year 2020; and

adequate disclosure is made in its listing document, including:

the likelihood of continuance or recurrence of the circumstances leading to the applicant's inability to meet the spread of the increased Profit Requirement;

measures that were taken or will be taken by the applicant to mitigate the impact of those circumstances on future profitability;

a profit forecast covering the period up to the forthcoming financial year end date after the date of listing with detailed bases and key assumptions.

Transitional Arrangements

In addition, the Exchange recognises that some companies may already have commenced plans to apply for Main Board listing relying on the current Profit Requirement. To minimise impact on these applicants, it is proposed that the increased Profit Requirement will take effect no earlier than 1 July 2021. Main Board listing applications (including GEM Transfer applications) will accordingly be assessed under the existing Profit Requirement if submitted before 1 July 2021 and remain active (i.e. not lapsed, withdrawn, rejected or returned). Such applications will be allowed to be renewed once for continued assessment under the existing Profit Requirement, but any subsequent renewals will be assessed under the increased Profit Requirement (if adopted).

Conclusion

The Exchange acknowledges that by adopting either option, the bourse will have one of the most stringent financial eligibility tests as to profit requirement compared with other major markets. It believes that the proposal will enhance market quality, increase investor's confidence in the market and strengthen Hong Kong's position as an international financial centre.

If the proposal is adopted, companies that do not meet the increased Profit Requirement can still access the markets by listing on GEM (no profit requirement). Qualifying early development stage companies in the biotech sector will not be affected and may seek a Main Board listing under Chapter 18A of the Main Board Listing Rules.

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)