The new EU investment firm prudential regime - an overview

The EU is introducing a new prudential regime for non-systemic investment firms. This article gives an overview of its requirements and assesses its impact.

The EU has recently agreed a final compromise text on the new investment firm prudential regime. This client briefing provides an overview of what was agreed and considers its potential impact on your firm.

Executive summary

“IFD/IFR” is an abbreviation for the Investment Firm Directive and Investment Firm Regulation.

Systemic investment firms will either be reclassified as credit institutions or treated for prudential purposes as if they were credit institutions. Non-systemic investment firms will be prudentially regulated under a new regime, set out in the IFD/IFR.

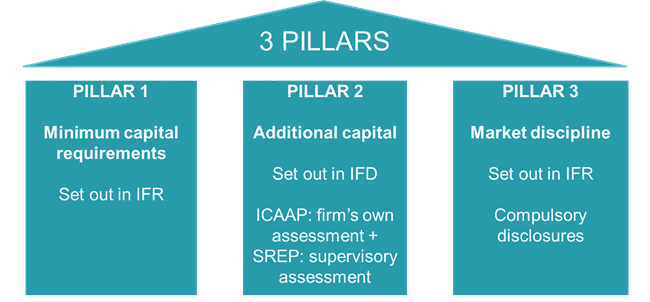

Like CRD4, the new regime will have a three-pillar structure. Pillar 1 represents the minimum capital requirement, Pillar 2 an ICAAP and SREP process with the possibility of capital add-ons and Pillar 3 imposes a compulsory disclosure regime.

The definition of capital in the new regime is based on CRD4. The new Pillar 1 capital requirement is the greatest of:

- a permanent minimum capital requirement of between €75k and €750k;

- a fixed overhead requirement equal to 25% of the previous year’s fixed overheads; and

- a requirement based on a set of “K-factors”. The K-factors are proxies or metrics for measuring the different kinds of risks to which an investment firm is exposed.

Each firm is likely to be impacted differently depending its circumstances and activities. However, we think that for most firms the IFD/IFR will probably increase Pillar 1 capital requirements. Some investment advisers might see significant increases in Pillar 1 capital requirements.

Besides the Pillar 1 capital requirement, investment firms must comply with the liquidity requirement: they must hold liquid assets equal to or greater than a third of their fixed overheads requirement (ie a twelfth of the previous year’s fixed overheads) plus 1.6% of any client guarantees given.

There are carve outs for small and non-interconnected firms.

The IFD/IFR is likely to apply (in the EU) from about Q4 2020 to Q2 2021. If it does not apply in the UK, we think the UK is likely to align closely to it.

AIFMs and UCITS Mancos with MIFID top-ups will probably have to apply the IFD/IFR in parallel with the capital requirements set out in the AIFMD or UCITS Directive.

Related client briefings

- Groups and consolidated prudential supervision: the regime under CRD5/CRR2 and the IFD/IFR.

- Remuneration under CRD5 and the IFD

- SRD2 – are you ready?

Why create a new prudential regime for investment firms?

Historically, most investment firms have been required to comply with the prudential requirements set out in CRD3 or CRD4. These requirements are derived from the Basel standards, which were designed for internationally active banks and hence focussed on the lending and deposit taking functions of credit institutions. Most investment firms have very different business models. To make prudential requirements appropriate for them, the current approach has been to adopt a labyrinthine system of exceptions and modifications. In EU law, there are currently 11 different prudential categories of investment firm, with further categories existing under national law.

The new EU investment firm prudential regime has been designed specifically with investment firms and their business models in mind. It is intended to provide investment firms with a simpler system of prudential regulation appropriate for their business models.

Where are we in the EU legislative process?

The IFD/IFR has its genesis in a requirement in CRD4 for the European Commission to review the prudential regime for investment firms. After a European Banking Authority (EBA) discussion paper and the European Commission review, the European Commission adopted a legislative proposal on 20 December 2017. The Council adopted a negotiating position on 09 October 2018 and the European Parliament on 03 October 2018. Informal negotiations (called trilogues) have taken place between the institutions, and a final compromise text was published on 19 March 2019. This text is now undergoing a “legal-linguistic revision”, where the drafting will be polished and the text translated into all the EU official languages. It is likely to be adopted in the summer or autumn of 2019.

Whilst we do not think there will be any further substantive changes, the numbering of the Articles is likely to change, and we have therefore not included any references to Article numbers in this briefing.

It seems that the IFD/IFR is intended to apply at the same time as, or after, the CRD5 package of legislation.

When will it come into force? And will it affect the UK?

In the EU, the main provisions of the new prudential regime are likely to apply in about Q4 2020 to Q2 2021.

The new regime would also apply in the UK if:

- the UK is still a member of the EU when the new regime applies in the EU; or

- the UK has left the EU before the new regime applies in the EU, but the IFD/IFR applies in the UK because of a transitional agreement between the UK and the EU.

In practice, we think the UK is likely to apply the new regime in domestic law even if it is not required to. This is because the IFD/IFR amends the third country regime in the Markets in Financial Instruments Regulation (MIFIR) to incentivise the UK to apply it. Under Article 46 of MIFIR, a third-country investment firm without a branch in the EU may provide investment services to professional clients and eligible counterparties based in the EU if it is registered in an ESMA register. ESMA may only register a firm if the European Commission has adopted an equivalence decision in respect of the third country under Article 47 of MIFIR. The IFD/IFR amends Article 47 to require the equivalence assessment to be “detailed and granular” if the third country investment firms are of systemic importance to the EU. This is likely to be the case for the UK and we suspect these amendments have been made with the UK in mind.

An overview of the IFD/IFR

The approach taken by the IFD/IFR is set out in the following map, which we will follow in this briefing.

The IFD/IFR also contain reporting requirements, but we have not covered these requirements in this client briefing.

What is an investment firm for the purposes of the IFD/IFR?

IFD/IFR defines investment firms by reference to MIFID2. An investment firm is a person whose regular occupation or business is the provision of one or more investment services to third parties or the performance of one or more investment activities on a professional basis. But the IFD/IFR do not apply to a firm which:

- falls into a derogation in Article 2 of MIFID2; or

- is not subject to MIFID2 because the Member State in which it is established has chosen not to apply MIFID2 to the firm in accordance with Article 3 of MIFID2.

This is an improvement on CRD4, where “investment firm” was defined slightly differently to MIFID2, and therefore created a trap for the unwary. That said, there is a possibility that some national regimes for the prudential regulation of firms falling into Article 3 of MIFID2 may remain in place. We think it likely that if the UK were to implement IFD/IFR, it would continue specialist regimes for such firms.

AIFMs and UCITS Mancos may have MIFID top-ups. If so, they will probably have to apply the IFD/IFR in parallel with the capital requirements set out in the AIFMD or UCITS Directive.

The new classification of investment firms

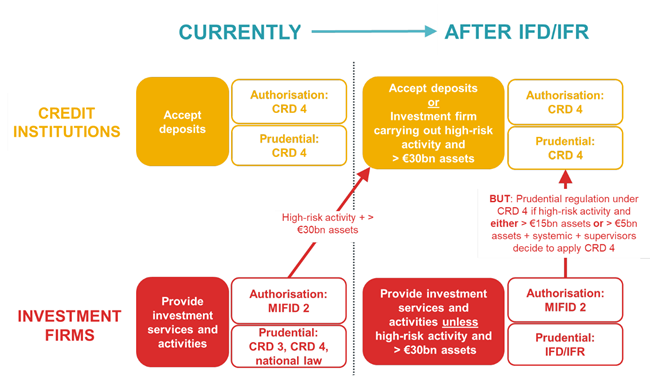

At present, credit institutions are firms with permission to accept deposits and are authorised and prudentially regulated under CRD4. Investment firms are firms with permission to provide investment services or carry out investment activities, and are authorised under MIFID2 and prudentially regulated under CRD4, CRD3 or national law. The IFD/IFR changes this and simplifies the prudential classification of investment firms.

Under the IFD/IFR, there will be three main categories of investment firms:

- Class 1: systemically significant investment firms

- Class 2: all investment firms not in classes 1 or 3

- Class 3: small and non-interconnected firms.

These classes were introduced in the EBA Discussion paper and used in the European Commission review. They are carried forward (with some amendment) into the final compromise text, but the text does not explicitly refer to “Class 1”, “Class 2” or “Class 3” firms as such. Nevertheless, we will use these labels in this briefing for convenience.

Class 1 firms will be undertaking similar activities to banks and therefore have comparable risk profiles. The IFD/IFR therefore treats them as banks, either by reclassifying them as credit institutions or applying CRD4 to them as if they were credit institutions. For CRD4 to apply, firms must carry on high-risk activities putting their capital at risk, namely dealing on own account, or underwriting or placing on a firm commitment basis. If a firm conducting high-risk activities has consolidated assets of more than €30bn, then the firm will be reclassified as a credit institution. If the consolidated assets are between €15bn and €30bn, then the firm will be required to comply with CRD4 for prudential purposes rather than the IFD/IFR (although its initial capital requirement will be set under the IFD). If they are over €5bn and the firm satisfies a test as to its systemic significance, then supervisors have a discretion to require the firm to comply with CRD4 for prudential purposes rather than IFD/IFR (although its initial capital requirement will be set under the IFD). When considering the thresholds of €30bn and €15bn, there are anti-avoidance provisions for groups. There are also carve-outs for commodity and emission allowance dealers, AIFs, UCITS and insurance undertakings.

The thresholds and tests can be summarised in the following flowchart:

The overall effect on how credit institutions and investment firms are authorised and prudentially regulated can be summarised as follows:

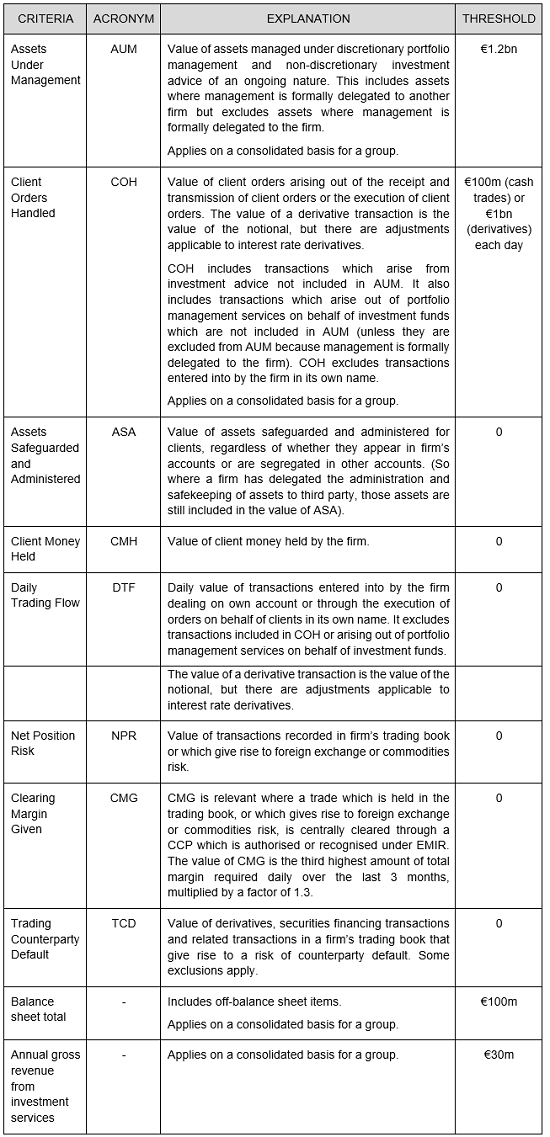

The classification of Class 2 and Class 3 firms depends on the activities they carry out. Table 1 below sets out the criteria and applicable thresholds. The criteria (except for balance sheet total and gross annual revenue) are also used as “K-factors” to calculate capital requirements for Class 2 firms. For example, assets under management (called “AUM”) is used as a criterion for distinguishing Class 2 and Class 3 firms, and a specified percentage of AUM is used to calculate the capital requirement for assets under management (called K-AUM).

If a firm exceeds any of these thresholds, it is a Class 2 firm.

Table 1

Please note that there is a slight ambiguity concerning NPR and TCD. The drafting could be read as requiring the calculation of the capital requirement (or K-factor) for NPR and TCD. However, we think this is unlikely to be what is intended, given the complexity of what would be required. We think the intention is to refer to the value of the underlying transactions rather than their capital requirement.

So far as AUM is concerned, the inclusion of non-discretionary investment advice is a little surprising and is a possible catch for the unwary.

As can be seen, any firm with a trading book, or which holds client money or safeguards and administers assets on behalf of clients, will therefore be a Class 2 firm.

The three Pillar approach

Although the IFD/IFR does not explicitly refer to Pillars, it adopts the same three Pillar approach used in the Basel standards and implemented in CRD4. Pillar 1 represents the minimum capital requirement applicable to all firms, Pillar 2 the supervisory discretion to impose capital add-ons and Pillar 3 a compulsory disclosure regime. This can be illustrated as follows:

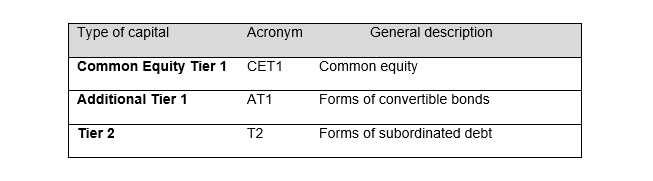

How is capital defined and what are the capital ratios?

The definition of capital and the capital ratios are derived from CRD4. The three tiers of capital are set out in Table 2:

Table 2

However, some of the deductions from capital have been modified for investment firms. In particular, investment firms will not need to deduct non-significant holdings of capital instruments in financial sector entities if those holdings are held in the trading book. This is to facilitate market making in those instruments. Also, the requirements for AT1 are modified so that the trigger event (converting AT1 into CET1) must be set out in the terms of the AT1 instrument itself. Supervisory approval for the reduction of own funds is also modified, so that it will be deemed to have been given where:

- the investment firm replaces the instruments being redeemed or repurchased with instruments of equal or higher quality at terms which are sustainable for the income capacity of the firm. This must occur before or at the same time as the redemption or repurchase; or

- for redemptions of AT1 or T2 instruments within five years of issue, there is a regulatory change or tax change event.

This should make it easier to reduce capital.

For Class 3 firms, or where a firm is not a body corporate, supervisors may permit the use of other instruments or funds to satisfy the capital requirement.

Common Equity Tier 1 capital must comprise at least 56% of the firm’s capital requirement, with Additional Tier 1 not exceeding 44% and Tier 2 not exceeding 25%. These are the same ratios as in the CRR but expressed differently. For example, the CRR requires capital of 8% of total risk-weighted exposures with at least 4.5% of that 8% being Common Equity Tier 1. Therefore, Common Equity Tier 1 must amount to at least 4.5/8 x 100% = 56% of capital, which is the threshold adopted in the IFD/IFR.

The Pillar 1 minimum capital requirement

The Pillar 1 minimum capital requirement is the greatest of:

A permanent minimum capital requirement – between €75,000 and €750,000, depending on the investment services and activities provided by the firm. The permanent minimum capital requirement for firms operating an MTF or OTF (which does not deal on own account) has been lowered from €730,000 to €150,000 to reduce barriers to entry.

A fixed overhead requirement – of 25% of the firm’s fixed overhead in the previous year. Full details will be set out in an RTS, but we think this will probably follow the current approach in the CRR.

A K-factor requirement – based on “K-factors” which are proxies or metrics for measuring the different types of risk to which a firm is exposed.

But a Class 3 firm (a small and non-interconnected firm) is not required to comply with the K-factor requirement.

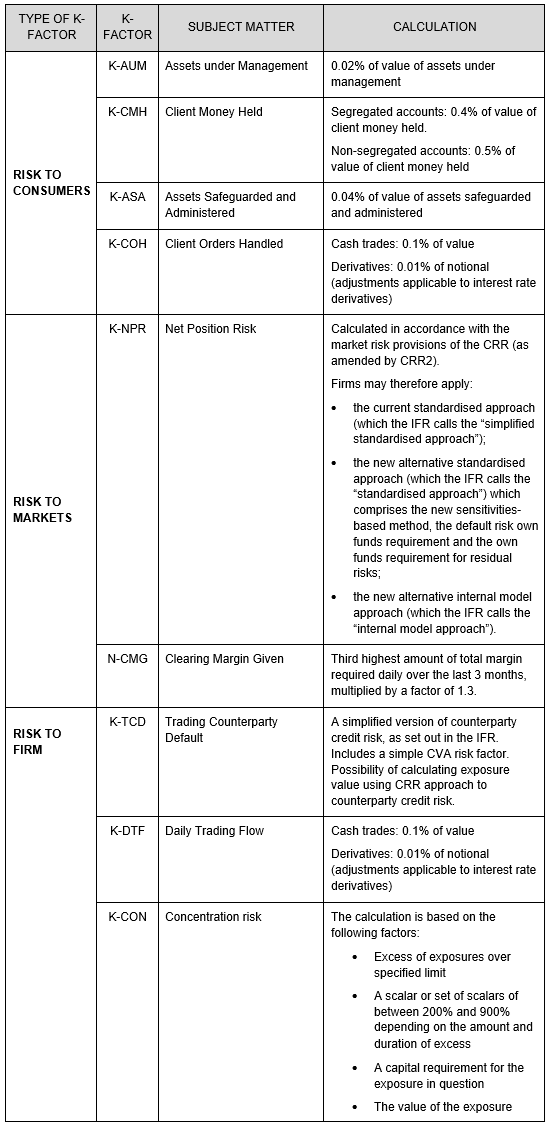

What is the K-factor requirement?

The K-factor requirement represents the real novelty of the IFD/IFR, so it is worth examining in more detail.

The risk-to-consumer K-factors are the K-factors for Assets Under Management (K-AUM), Client Money Held (K-CMH), Assets Safeguarded and Administered (K-ASA) and Client Orders Handled (K-COH). The definition of Assets under Management (AUM), Client Money Held (CMH), Assets Safeguarded and Administered (ASA) and Client Orders Handled (COH) is set out above in Table 1, where these amounts are used to distinguish Class 2 from Class 3 investment firms. The K-factors are calculated by applying a specified percentage to each of these amounts. For example, K-AUM is equal to 0.02% of AUM. All four of these K-factors are summed to give the total risk-to-consumer K-factor component.

The risk-to-market K-factor is either the K-factor for Net Position Risk (K-NPR) or the K-factor for Clearing Margin Given (K-CMG). A combination of the two K-factors is also possible. Net position risk (NPR) and Clearing Margin Given (CMG) are defined above in Table 1. A firm must obtain permission from its supervisor before applying K-CMG instead of, and in combination with, K-NPR.

The risk-to-firm K-factors are the K-factors for Trading Counterparty Default (K-TCD), Daily Trading Flow (K-DTF) and Concentration Risk (K-CON). Trading Counterparty Default (TCD) and Daily Trading Flow (DTF) are defined above in Table 1. K-CON is new: it is relevant where a firm exceeds the prescribed limits on concentration risk (see below). All three of these K-factors are summed to give the total risk-to-firm K-factor component.

The calculation of each K-factor is set out in the Table 3.

Table 3

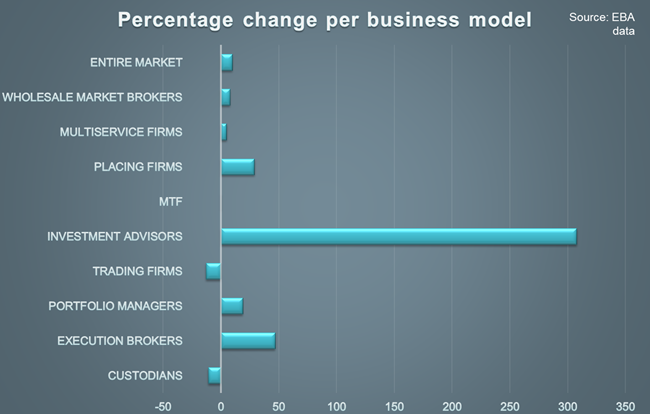

What is the likely impact of the new approach to Pillar 1 capital?

EBA investigated the impact of the new Pillar 1 requirements on firms. This was in the context of the original Commission proposal, but we think it is still roughly indicative of the impact of the final text. Here is a graph showing EBA’s conclusions:

The data shows a general increase in Pillar 1 capital requirements, with a particular impact being felt by investment advisers and execution brokers. The European Commission state that the large increase for advisory firms is because:

- there are several larger investment advisers in the EU currently subject only to an initial capital requirement, and

- K-AUM applies to assets managed under advisory arrangements.

The final compromise text cuts back on the scope of K-AUM slightly by requiring the advisory arrangements to be of an “ongoing nature”. However, it is not clear whether that will cushion the impact of the IFD/IFR on investment advisers.

The increase in capital requirements is perhaps not surprising. In very general terms, the IFD/IFR replicate the market risk and the fixed overhead requirements found in the CRR. They omit capital requirements for credit risk (except for counterparty credit risk which becomes the K-TCD), but many investment firms are not exposed heavily to credit risk, so the impact would be minimal. The IFD/IFR introduce new capital requirements for risks to consumers, although larger investment firms might already hold some capital for those risks under the operational risk requirements of the CRR. It seems plausible therefore that certain types of investment firm will face increased capital requirements under the IFD/IFR.

However, if one considers total capital requirements (Pillar 1 and Pillar 2), it is possible that the more embracing nature of the new Pillar 1 regime and the fact it is tailored specifically to investment firms, will lead to fewer and lower Pillar 2 capital add-ons.

Pillar 2 capital add-ons

The IFD/IFR preserve the ICAAP and SREP process with which most investment firms will be familiar. The Internal Capital Adequacy Assessment Process (ICAAP) is the firm’s own process for ensuring it has adequate levels of internal capital and liquidity. In particular, firms are required to monitor the value of their K-factors for any trends which could leave them with a materially different capital requirement for the next reporting requirement and notify their regulator of that capital requirement. The Supervisory Review and Evaluation Process (SREP) is a supervisory review of whether the firm complies with the IFD/IFR and whether all risks to the firm are adequately captured. Supervisors must also review firms’ permission to use internal models on a regular basis, and in any event at least every three years.

However, there is a carve out for Class 3 firms, unless the supervisor decides to impose it.

Supervisors can require firms to hold more capital, or adjust the capital and liquid assets a firm is required to hold if there are material changes to a firm’s business. They can also give “capital guidance” to ensure that cyclical economic fluctuations do not lead to a breach of the IFR or threaten the ability of the firm to wind down and cease activities in an orderly manner. “Capital guidance” is therefore a requirement to hold more capital and it assumes some of the functions of the capital buffers in CRD4.

Liquidity requirements

An investment firm must hold liquid assets equal to or greater than its liquidity requirement.

Firms may treat the following assets as liquid assets:

- The high-quality liquid assets referred to in Articles 10 to 13 and 15 of Delegated Act on the Liquidity Coverage Ratio. However, there is a threshold of €50m rather than €500m for the assets referred to in Article 15 (shares or units in collective investment schemes).

- Financial instruments trading on a liquid market (subject to a haircut of 55%).

- Unencumbered short-term deposits at credit institutions

- For Class 3 firms and firms not dealing on own account, underwriting or placing on a firm commitment basis, receivables for trade debtors and fees and commissions receivable within 30 days, subject to certain conditions being satisfied.

The liquidity requirement is equal to the sum of:

- A third of the firm’s fixed overheads requirement (so a twelfth of the firm’s fixed overheads in the preceding year), and

- 1.6% of the value of any customer guarantees given by the firm.

As part of the Pillar 2 process, supervisors can require investment firms to hold more liquid assets.

There is a derogation available for Class 3 firms.

Limits on concentrations and K-CON

The objective of these provisions is to protect the firm from exposures to a single client or group of connected clients which is large in proportion to the size of the investment firm, and which therefore presents an increased risk to the investment firm. They serve the same purpose as the large exposure requirements in CRD4.

The limits apply to exposures arising from:

- net positions in the trading book, which are hence already subject to K-NPR. (A firm calculating K-CMG must calculate K-NPR for these purposes), or

- derivatives, securities financing transactions and other related transactions which are already subject to K-TCD.

However, some exposures are excluded, such as exposures deducted from own funds, exposures to central governments and exposures to CCPs.

Where the exposures mentioned above are exposures to a single client or a group of connected clients (eg parent and subsidiary undertakings), then they must not exceed:

- 25% of the firm’s regulatory capital, unless the excess is capitalised through K-CON and the supervisor is notified (the rules are modified for exposures to credit institutions or other investment firms)

- 500% of the firm’s regulatory capital for a period of up to or including 10 days after the 25% threshold has been breached, and

- in aggregate, 600% of the firm’s regulatory capital where an excess over the 25% threshold has persisted for more than 10 days.

Corporate governance

The IFD/IFR imposes corporate governance requirements on Class 2 firms. These cover internal governance, country-by-country reporting, treatment of risks, risk factors and remuneration.

Remuneration will be the subject of a separate client briefing - please see our client briefing on “Remuneration under CRD5 and the IFD”

Pillar 3 disclosures

The IFR impose disclosure requirements on:

- Class 2 firms, and

- Class 3 firms which issue AT1 capital instruments.

As with the Basel standards, the disclosure requirements are intended to impose market discipline on the firm to ensure it remains well capitalised.

The disclosure requirements for Class 2 firms cover its risk management objectives and policies, corporate governance, own funds, capital requirements, the firm’s remuneration and investment policies, and environmental, social and governance risks (called ESG risks). In particular, certain larger investment firms are required to disclose information about voting rights and voting behaviour in respect of shareholdings of more than 5% in companies traded on a regulated market. This is in addition to the requirements imposed on investment firms in relation to shareholders’ rights – for more information, please see our article on “SRD2 – are you ready?”

Our client note on “Remuneration under CRD5 and the IFD” provides more information about the remuneration disclosures.

Levels of application

In general, the IFD/IFR apply on both a solo and consolidated basis. However, there are a range of derogations that can apply. Investment firms which are members of a banking group may be subject to the requirements of CRD4 imposed on a consolidated basis.

Group and consolidated prudential supervision are considered in more detail in our related client briefing: “Groups and consolidated prudential supervision: the regime under CRD5 and IFD”.

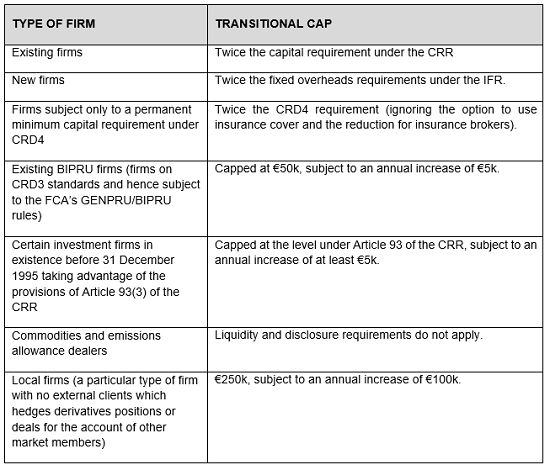

Transitional provisions and derogations

The IFD/IFR create a five-year transitional period. During that period, the following transitional caps will apply:

Table 4

Where investment firms are required to calculate K-NPR, the IFR/IFD requires them to apply the market risk provisions of the CRR as amended by CRR2. Given the uncertainty created by ongoing changes to the Basel standards arising out of the Fundamental Review of the Trading Book, the IFD/IFR permits firms to apply the market risk provisions of the CRR until five years after the application date of the IFR and the application date of CRR2, whichever is the later.

Finally, Class 1 investment firms (that is, systemic firms) with consolidated assets greater than €15bn remain subject to CRD4. Where a firm has consolidated assets greater than €30bn and hence will be reclassified as a credit institution, it must make an application for authorisation as a credit institution within a year and a day after the coming into force of the IFD (about summer 2020).

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)