Solidarity Tax on high net-worth individuals

The Spanish government has approved a controversial new tax complementary to Wealth Tax.

The Spanish government has approved a new tax complementary to Wealth Tax, the so-called Temporary Solidarity Tax for High Net-Worth Individuals. Those impacted by this new tax will be taxed in 2023 on their 2022 net wealth.

Background

Spain is the only country in the EU1 that taxes the worldwide net wealth of individuals when it exceeds certain thresholds, through the Wealth Tax. However, this tax is managed by the Spanish regions (the autonomous communities) which can increase or decrease the rate of the Wealth Tax. In this context, Madrid has traditionally maintained a full exemption from Wealth Tax. In September 2022, Andalucía joined Madrid approving a full exemption from Wealth Tax.

In the context of the tax campaign initiated by the Socialist/communist coalition against the banking and energy sector, the government reacted to the announcement made by the Andalucian president (from the conservative party) by approving a new tax with the purpose of subjecting to tax mainly those high net-worth individuals residing in Madrid and Andalucía2.

Temporary Solidarity Tax on high net-worth individuals

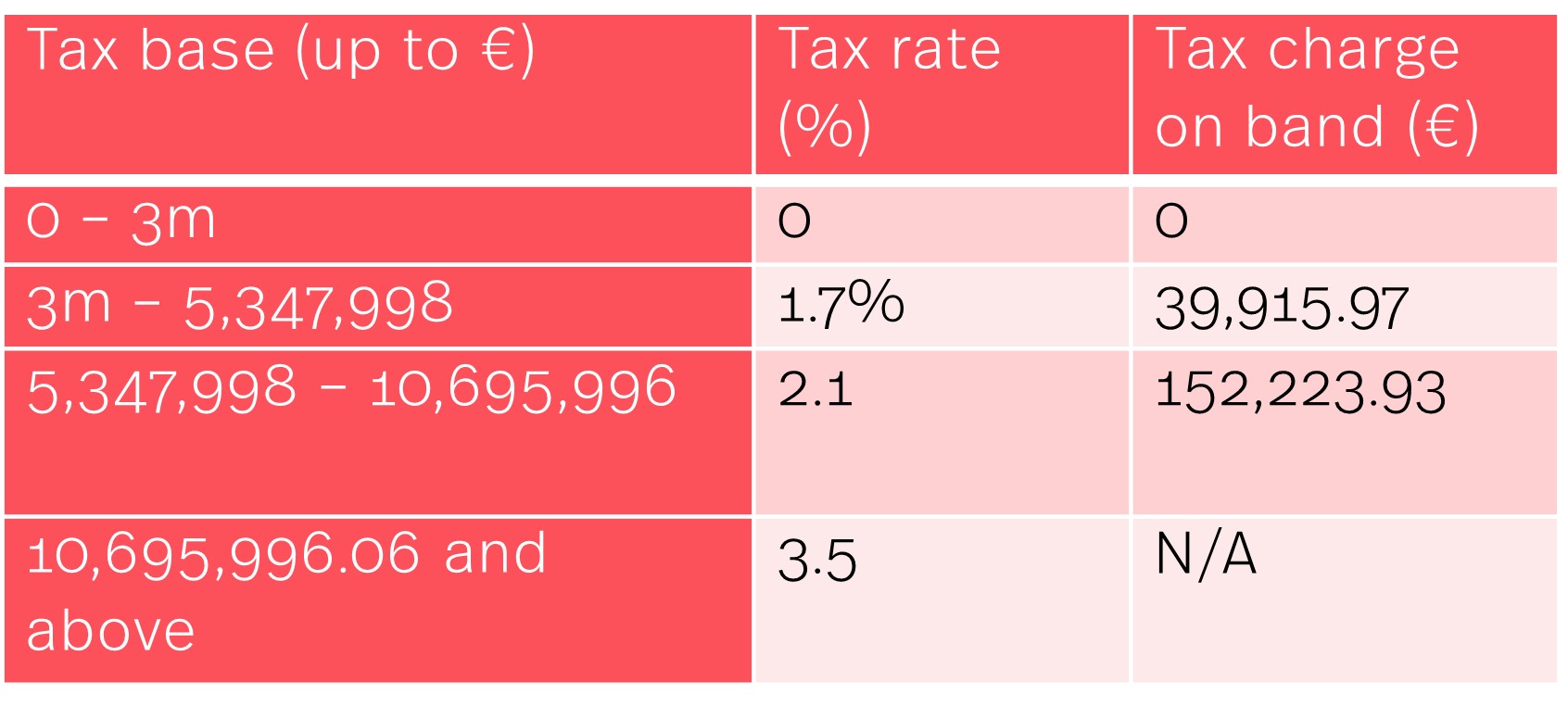

The new tax is, in principle, temporary (for two years, 2022 and 2023), complementary to the Wealth Tax and will be charged on the net wealth of individuals exceeding EUR 3m. The rates, exemptions and other detailed rules of this new tax are based on the Wealth Tax Law. To avoid giving rise to double taxation, the new tax will be deductible for Wealth Tax purposes (this way the main impact will be borne by individuals residing in Madrid and Andalucía).

Broadly, Spanish tax residents benefit from a general tax exemption on the first EUR 700,000 of net wealth, in addition to an EUR 300,000 exemption for the residential property considered the main residence. As a result, most Spanish tax residents (those owning their own residential property) would be taxed on net wealth above EUR 4m (as the first EUR 3m is subject to a zero rate) in accordance with the following table:

In the case of non-resident individuals, they will be subject to this new tax on their rights and assets located/exercised in Spain, but they do not have access to the general tax exemption of EUR 700,000 nor to the EUR 300,000 exemption for main residence (since it would be located abroad). Hence, non-residents are taxed on their net wealth located in Spain above EUR 3m. This new tax also impacts individuals subject to the expatriate tax regime (the Beckham law).

In addition, the amendment to extend Wealth Tax to non-residents with indirect holdings of real estate assets (see article the modification on Wealth Tax) should also be carefully considered. The new Solidarity Tax, together with the amendment to the Wealth Tax Law will have the result that non-residents with direct or indirect holdings of assets located in Madrid or Andalucía will be subject to the new Solidarity Tax, with potential significant tax leakage. For assets located in other regions, the impact of Solidarity Tax should be minor (if any) but only because the tax impact will be at the level of Wealth Tax. Taxpayers benefit from a joint limit for Personal Income Tax, Wealth Tax and Solidarity Tax but this should be carefully analysed.

Comment

Non-residents should carefully review their existing assets located in Spain and the holding structure for these assets.

It should also be noted that there are sound arguments to consider this new tax contrary to the Spanish Constitution, as the Bill used to incorporate this new tax may be in breach of the provisions included in the Spanish Supreme Law regarding the approval process for the creation of new of taxes. Also, this new tax could also breach the competences of the autonomous communities, as it is clearly intended to subvert the policy followed by Madrid and Andalucía under their legal competences.

Finally, EU based non-residents may be able to claim that the failure to extend the general tax exemption of EUR 700,000 available to Spanish residents to non-residents is in breach of the EU fundamental freedoms.

The potential impact of the new Solidarity Tax for high net-worth individuals should be carefully addressed on a case-by-case basis, and ultimately non-residents will need to be aware of possible procedures for making protective claims that may arise as a result of these new developments.

1 France, Italy and Belgium tax certain assets, such as real estate wealth in France, in Italy real estate and financial investments owned outside Italy, and Belgium investment accounts. None of them tax global net wealth as in Spain.

2 It should be noted that individuals residing in Galicia, Cataluña, Murcia, Asturias, Cantabria and Balearic Islands would also be impacted (depending on their net wealth) as the regional rates of Wealth Tax are lower than the new Solidarity Tax.

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

_(1)_11zon.jpg?crop=300,495&format=webply&auto=webp)