Update: On 3 October, the now former Chancellor, Kwasi Kwarteng, announced that the proposed cut to the additional rate of tax would no longer be introduced. In addition, on 14 October, Jeremy Hunt was appointed Chancellor of the Exchequer after Kwasi Kwarteng agreed to step down and the Prime Minister announced that the increase in the corporation tax rate enacted in Finance Act 2021 to 25% would now go ahead after all. Jeremy Hunt is now expected to deliver a further fiscal statement together with a full OBR report on 31 October.

The new Chancellor, Kwasi Kwarteng, has formally announced a raft of tax cuts and other measures in a special fiscal announcement on Friday 23 September dubbed The Growth Plan 2022. The aim of the measures is to boost growth in the economy and represents a sea change in approach from the government following the election of Liz Truss as the new Conservative Party leader and, hence, Prime Minister. Headline measures formerly announced by Rishi Sunak, including the increase in corporation tax to 25% and the health and social care levy (and the related temporary NIC increases) will be scrapped, marking a significant departure from the more cautious approach to government borrowing (and eventually paying it back) previously adopted. But the Chancellor went further by cutting the basic rate of income tax a year early and abolishing the 45% additional rate of tax, rolling back changes to the IR35 system that have been unpopular with businesses and cutting stamp duty.

The focus is now very much on growing the economy to alleviate the long-term burden of government borrowing – and tax cuts are regarded as an integral measure in achieving this boost.

A further (full) Budget is still expected to take place later this year – in November or maybe December – where the broader fiscal implications of these changes (together with the government’s measures to alleviate the energy price crisis) will be commented on by the Office for Budget Responsibility (OBR), whose duty it is to examine and report on the sustainability of the public finances. In the meantime, it is generally accepted that the government’s approach involves a significant gamble in cutting the government’s tax receipts at a time when government borrowing is set to increase both at an unprecedented rate and just as it becomes more expensive to do so.

The tax cutting measures are just one part of the Growth Plan, which also includes measures relating to planning, financial services, business regulation, immigration, industrial relations, childcare and the benefits system. However, in the longer term, the tax system is seen as key to delivering the annual 2.5% growth target set by the government. As such, it appears that the tax announcement made today will just be the first of potentially many to come to tailor the system to deliver growth. To this end, the Growth Plan commits the government to conducting a review to identify where it can go further to reform the tax system to ensure it supports growth, whilst also being simpler and better for families. The Chancellor will report on this in 2023.

Business taxes

The rate of corporation tax was due to rise to 25% from April 2023. That increase will now be scrapped and the rate will remain at 19%. This will require new legislation as the 25% rate was enacted in Finance Act 2021.

There will be a number of implications resulting from the change beyond the mere rate of corporation tax. The scrapping of the rate increase will also have knock-on implications for the rate of diverted profits tax, which was due to rise to 31% but which will now remain at 25%. In addition, the bank surcharge, which was due to reduce from 8% to 3% from April 2023 will now remain at 8% - whilst the profit threshold from which it applies will still increase from £25m to £100m with a view to increasing competitiveness in the banking sector and fuelling the growth of “challenger” banks.

It is unclear exactly what this means for the increased rates of capital allowances for qualifying expenditure on plant and machinery put in place between April 2021 and March 2023 in part to offset the expected increase in the rate of corporation tax. The increased reliefs include a 'super-deduction' providing first-year allowances of 130% for new plant and machinery investments that ordinarily qualify for 18% main rate writing down allowances and a first-year allowance of 50% for new plant and machinery investments that ordinarily qualify for 6% special rate writing down allowances. However, the Growth Plan does indicate that the government will amend some of the technical provisions for the super-deduction as a consequence of the corporation tax rate being retained at 19% from 1 April 2023 to ensure that the relief continues to operate as intended, which suggests that these will not be wholly rolled back.

In addition, the Chancellor did announce that the Annual Investment Allowance threshold will be permanently set at £1m, rather than reverting to £200,000 from April 2023. This is a 100% capital allowance for qualifying expenditure on plant and machinery. The government is also currently consulting more widely on the future of the capital allowances system.

The government announced it will increase the availability of the Seed Enterprise Investment Scheme (SEIS) and Company Share Option Plan (CSOP). In addition, the government indicated that it remains supportive of the Enterprise Investment Scheme (EIS) and Venture Capital Trusts (VCT) and sees the value of extending them in the future.

- Seed Enterprise Investment Scheme (SEIS) – From April 2023, companies will be able to raise up to £250,000 of SEIS investment. To enable more companies to use SEIS, the gross asset limit will be increased to £350,000 and the age limit from 2 to 3 years. The annual investor limit will be doubled to £200,000.

- Company Share Option Plan (CSOP) – From April 2023, qualifying companies will be able to issue up to £60,000 of CSOP options to employees, double the current £30,000 limit.

Personal taxes

The Chancellor also announced that the increased rates of NICs applying during 2022 (in advance of the introduction of the health and social care levy from April 2023) would be scrapped from 6 November 2022. The health and social care levy will no longer be introduced from April 2023. In addition, the government will reverse the 1.25% increase in dividend tax rates from April 2023.

The government had previously announced plans to introduce a new health and social care levy at 1.25% from April 2023 in order to pay for increased spending on health and social care measures. As the first step leading to this new health and social care levy, the government temporarily increased the rate of NICs for one year from April 2022 for employees, self-employed and employers by 1.25%. In addition, taxes on dividends were also increased by 1.25% from April 2022 (dividends from shares are not subject to NICs (or the levy) and no doubt the Government was concerned that many business owners would simply choose to pay themselves increased dividends rather than salary in the absence of a matching increase).

The government had previously indicated its ambition to reduce the personal income tax rate to 19% in April 2024. The Chancellor has now announced that this reduced rate (down from 20%) will now be brought into effect a year early from April 2023. To deal with the consequences of this change, there will be transitional arrangements to enable basic rate tax relief to be claimed at the 20% rate by “relief at source” pension schemes for an extra year, and to keep the level of gift aid relief that can be reclaimed by charities at 20% for a transitional four year period.

In addition, the 45% additional rate of tax that currently applies to earnings over £150,000 will also be removed from April 2023. There will be further consequences of this change, including that former additional rate taxpayers will now become entitled to the personal savings allowance at £500 per annum. However, at this stage there is no indication that any changes will be made to the provisions reducing the personal allowance or limiting pension contributions by high earners.

Perhaps most surprisingly, the Chancellor announced that the 2017 and 2021 reforms to the off-payroll working rules (also known as IR35) will be repealed from 6 April 2023. These changes placed much of the burden of ensuring compliance with these rules on the hiring entity - first in the public sector and then in the wider private sector – as a means of seeking better compliance with the rules. From this date, workers across the UK providing their services via an intermediary, such as a personal service company, will once again be responsible for determining their employment status and paying the appropriate amount of tax and NICs.

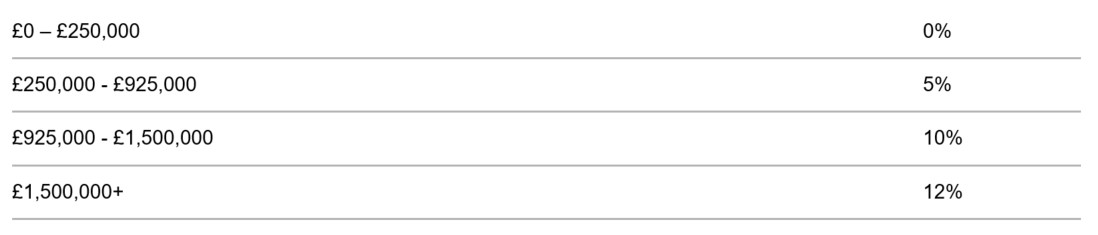

Stamp duty

As widely leaked in advance of the Chancellor’s statement, there will also be changes to rates of stamp duty in order to increase activity in the housing market. An active housing market is seen as one area that may boost growth generally as house moves generate greater economic activity.

To this end, the zero-rate band for stamp duty has been increased with immediate effect to £250,000 and the zero-rate allowance for first time buyers will be increased to £425,000, with the maximum value of the property eligible for first time buyers relief increasing to £625,000. These changes are not time limited, unlike the previous stamp duty “holiday” adopted during the pandemic. From 23 September 2022, the SDLT rates for residential property will be:

Other announcements

Abolishing the Office of Tax Simplification – Having pledged to simplify the tax system since a simple tax system is critical for growth, a somewhat surprising measure announced by the Chancellor was the abolition of the Office of Tax Simplification. The Chancellor’s thinking is that, instead of having a separate arms-length body to oversee simplification, the government will embed tax simplification into the institutions of government. It will therefore set a mandate to the Treasury and HMRC to focus on simplifying the tax code generally. Nevertheless, not having a body whose raison d’etre is to consider and make recommendations on tax simplification seems to be a backward step in this regard. It is also unclear what will happen to existing OTS projects, including the recently announced review of hybrid and distance working as well as consultations on reforming capital gains tax and inheritance tax.

VAT free shopping for overseas visitors - The government has announced that it will introduce a modern, digital, VAT-free shopping scheme, with the aim of providing a boost to the high street and creating jobs in the retail and tourism sectors. A consultation will gather views on the approach and design of the scheme to be delivered as soon as possible. The new VAT-free shopping scheme for non-UK visitors to Great Britain will enable them to obtain a VAT refund on goods bought in the high street, airports and other departure points and exported from the UK in their personal baggage.

New Investment Zones – Hot on the heels of the government’s recently introduced Freeports, the government will now expand the scope of tax incentivised business areas to newly created Investment Zones. These will benefit from a range of tax and other incentives as yet to be finally determined.

From a tax perspective, they will benefit from a range of time-limited tax incentives over 10 years. The tax incentives under consideration are:

- 100% relief from business rates on newly occupied business premises

- 100% first year allowance for companies’ qualifying expenditure on plant and machinery assets for use in tax sites.

- enhanced Structures and Buildings Allowance; accelerated relief to allow businesses to reduce their taxable profits by 20% of the cost of qualifying non-residential investment per year

- zero-rate Employer NICs on salaries of any new employee working in the tax site for at least 60% of their time, on earnings up to £50,270 per year

- full SDLT relief for land and buildings bought for use or development for commercial purposes, and for purchases of land or buildings for new residential development.

Alcohol duty reform - The government is publishing its response to the Alcohol Duty Review consultation launched at Autumn Budget 2021, alongside the draft legislation for consideration. The reforms are intended to make the current system simpler, more economically rational and less administratively burdensome on businesses. The reforms will be implemented from 1 August 2023. The government is also freezing the alcohol duty rates from 1 February 2023.

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)