Financial services regulation after Brexit

This briefing considers the impact of Brexit on financial services regulation, both during and after the transition period.

What is the Withdrawal Agreement and the European Union (Withdrawal Agreement) Act 2020?

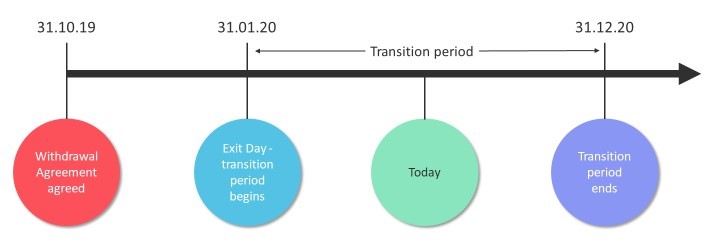

The Withdrawal Agreement is intended to ensure the UK’s smooth and orderly departure from the EU. The UK left the EU on 31 January 2020 (exit day). However, the Withdrawal Agreement creates an implementation period or transition period running from exit day to 31 December 2020. (Implementation period and transition period are synonymous so we will use transition period in the rest of this briefing). During the transition period, EU law will, for the most part, continue to apply in the UK. The Withdrawal Agreement also makes provision for a range of other matters, such as the status of EU nationals in the UK.

Although the Withdrawal Agreement has been agreed by the UK Government, it does not take effect automatically in UK law. This requires an Act of Parliament, and accordingly the European Union (Withdrawal Agreement) Act 2020 ratifies and gives effect to the Withdrawal Agreement in the UK.

This diagram illustrates the timeline:

What is the law in the UK during the transition period?

EU law continues to bind and have effect in the UK during transition period.

References to “Member States” in EU law will include UK, even though the UK is not actually a Member State. Existing EU law will continue to apply, so that EU Regulations which already apply in the UK (for example, EMIR) continue to apply and EU Directives which already bind the UK (for example, MIFID 2) continue to bind it. Accordingly, UK domestic regulations which implement directives remain in force (subject to possible very technical amendments to ensure they still work). New EU Regulations which apply during the transition period will also form part of UK law and the UK must implement new EU Directives if the transposition deadline falls within the transition period.

In terms of litigation and enforcement, the Court of Justice of the European Union continues to have jurisdiction in proceedings brought by or against the UK, or in references from UK courts for the interpretation of EU law, before the end of the transition period. EU institutions and agencies continue to be competent for administrative procedures initiated before the end of the transition period (for example, ESMA’s supervisory powers over credit rating agencies and trade repositories).

There are some exceptions to the above and some special rules. These either relate to areas of EU law which never bound the UK (for example, the Schengen Agreement enabling passport-free border crossing) or have limited relevance to financial services regulation (for example, standing as a candidate in elections).

So, is it business as usual then?

Unfortunately, not quite. Although the Withdrawal Agreement and the European Union (Withdrawal Agreement) Act 2020 assist greatly in ensuring that things carry on as before, they rely on glossing provisions (for example, treating references to "Member State" as if they included the UK even though the UK is not actually a Member State). The glossing provisions can only extend to EU and UK law. They do not necessarily extend further, for example to private contracts or third country law.

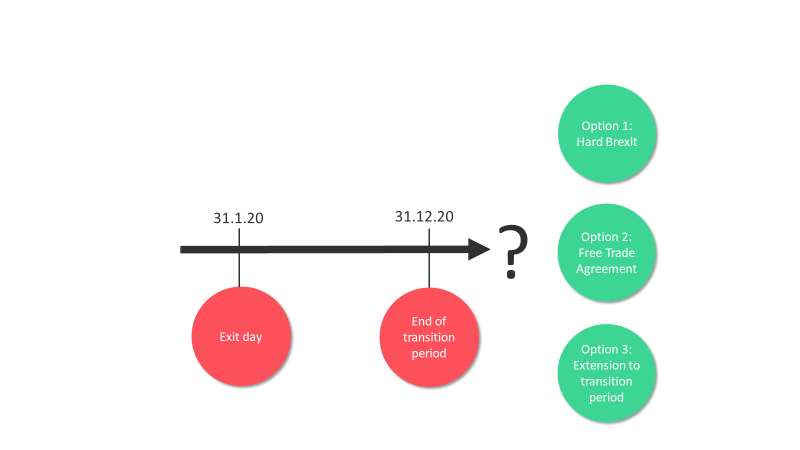

What happens after the end of the transition period?

There are three possibilities, as illustrated in the following diagram.

Option 1 is essentially a “hard Brexit” on 31 December 2020. This is the default option under the European Union (Withdrawal Agreement) Act 2020, and accordingly it heavily amends the European Union (Withdrawal) Act 2018. In essence, the Act will take a snapshot of EU law applying directly in the UK on 31 December 2020 and preserve it as UK law. The preserved law is subject to amendments to make it workable, as set out in the Brexit SIs. There is a glossing provision in the European Union (Withdrawal Agreement) Act 2020 which means that the Brexit SIs are commenced by reference to the end of the transition period (the Act calls this IP completion day) rather than by reference to exit day. The Government has made further provision in relation to temporary permission and transitional regimes. These have already commenced to enable the UK regulators and affected firms to begin preparing before exit day. These regimes need to remain in force during the transition period, but again, will only commence at the end of the transition period.

Option 1 presents significant uncertainty for firms. There are several EU Regulations which may only in part become part of UK law. So, for example, although CSDR would apply in the UK, the Settlement Discipline RTS may not, if its application date were extended to February 2021 as proposed by ESMA early in February 2020. Then there are others, the application date of which fall after 31 December 2020, which would only become part of UK law if expressly adopted. In this camp falls the important new IFD/IFR package.

Option 2 is that the UK and EU agree a free trade agreement. This would almost certainly require further legislation to implement. However, EU law is such an integral part of UK law that we would anticipate that much EU law would be preserved as UK law as with a hard Brexit.

Option 3 is that the transition period is extended. The UK and EU must both agree to any such extension by 1 July 2020. The European Union (Withdrawal Agreement) Act 2020 contains provision preventing the UK from doing so. However, nothing stops the UK Government introducing further legislation removing this prohibition. Ultimately, any extension must end either in a “hard Brexit” or a free trade agreement.

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)