Tax rates and allowances for 2020/2021

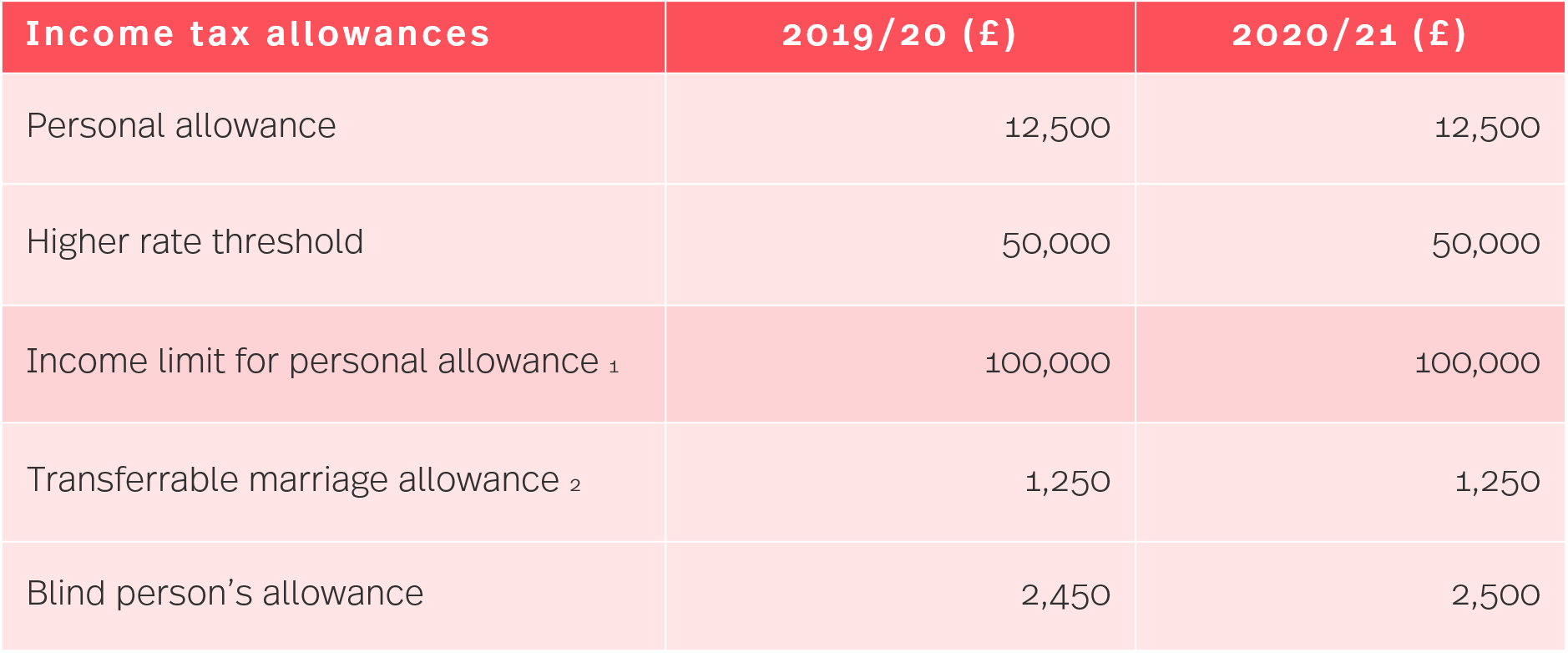

1 The individual’s personal allowance is reduced where their income is above this limit. The allowance is reduced by £1 for every £2 above the limit.

2 The marriage allowance cannot be transferred to a recipient spouse liable to income tax at the higher or additional rate.

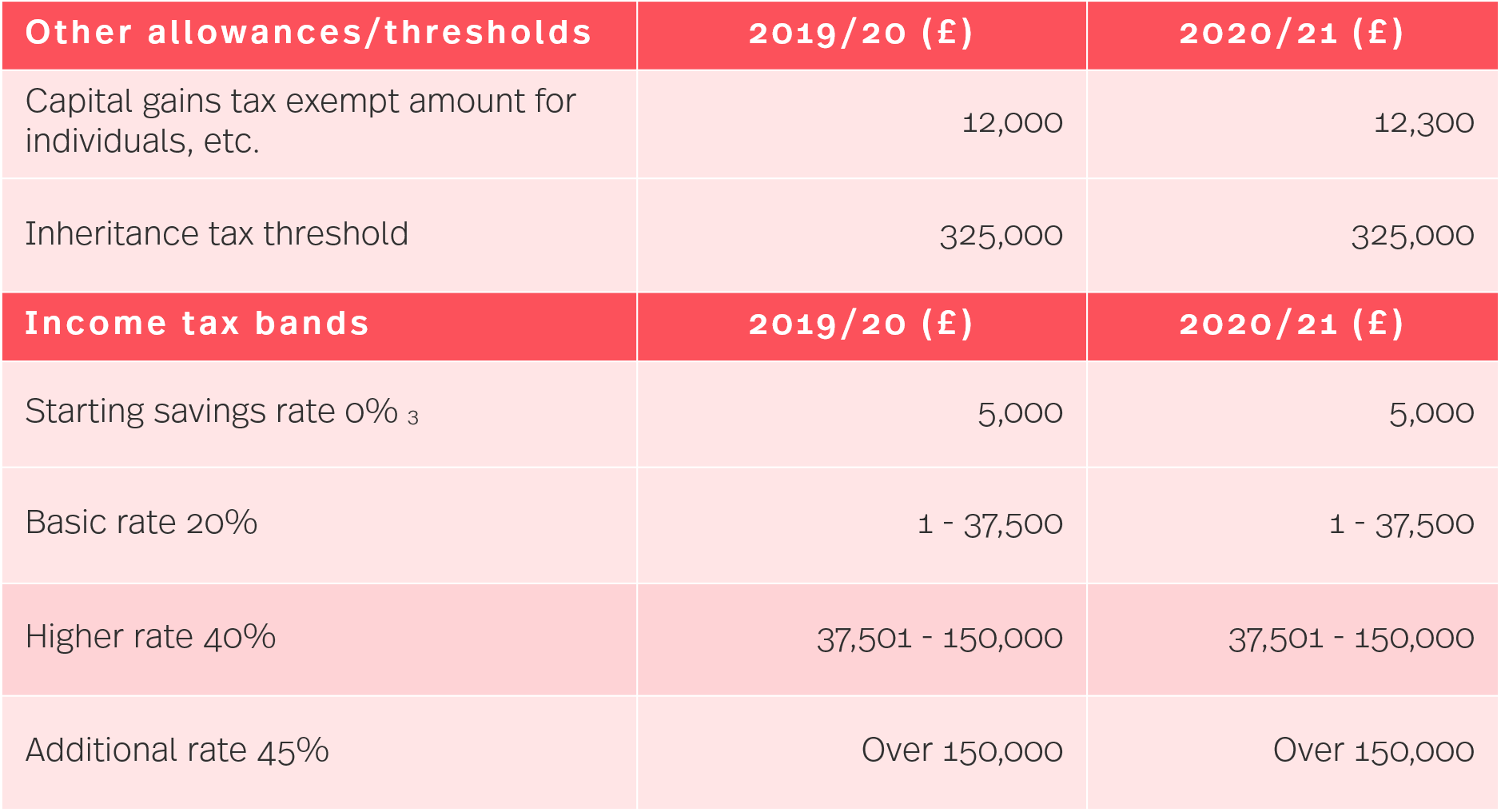

3 If savings taxable income exceeds the starting rate limit, the starting savings rate will not apply to savings income.

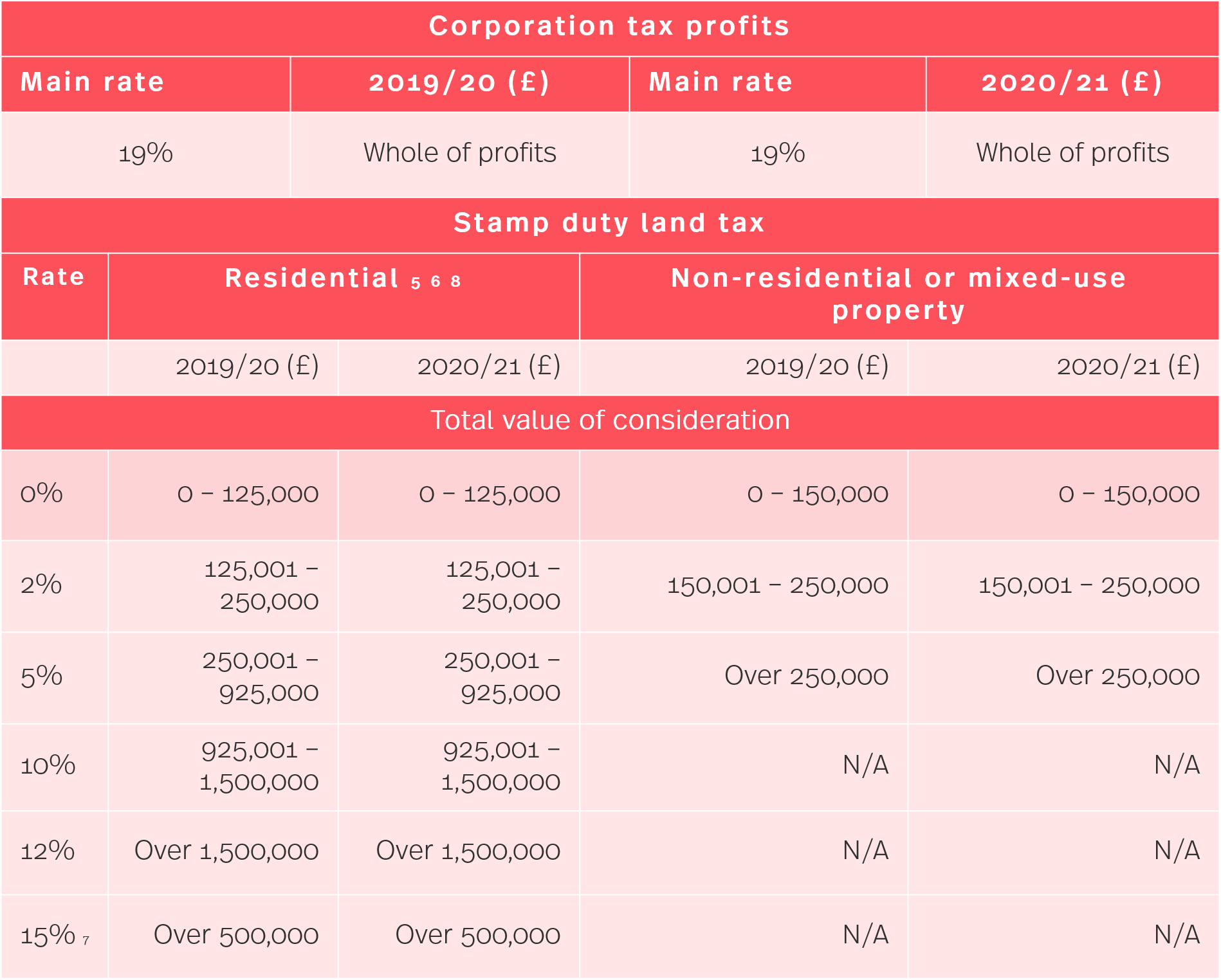

5 Stamp duty land tax is charged at a rate of 3% above the current stamp duty land tax residential rates from 01 April 2016 on purchases by individuals of additional residential properties (such as second homes and buy-to-let properties), and by non-natural persons (companies, partnerships including companies or collective investment schemes) of a residential property, even if they do not own another residential property.

6 For purchases by first-time buyers of property worth £500,000 or less from 22 November 2017, the stamp duty land tax rate for a property valued £0 – 300,000 is 0% and for a property valued £300,001 – 500,000 is 0% on the consideration up to £300,000 and 5% on the remainder.

7 The 15% rate applies to certain acquisitions of residential property by “non-natural persons” (a company, a partnership including a company or a collective investment scheme).

8 A 2% surcharge will take effect from 01 April 2021 on non-UK residents purchasing residential property in England and Northern Ireland.

Key contacts

If you have any questions, contact a member of the HMRC tax rates and allowances for 2020/21 team for assistance: