07 September 2026Event

Legal Professional Privilege (LPP) in Tax Matters

Explore how legal privilege applies to tax investigations in Europe

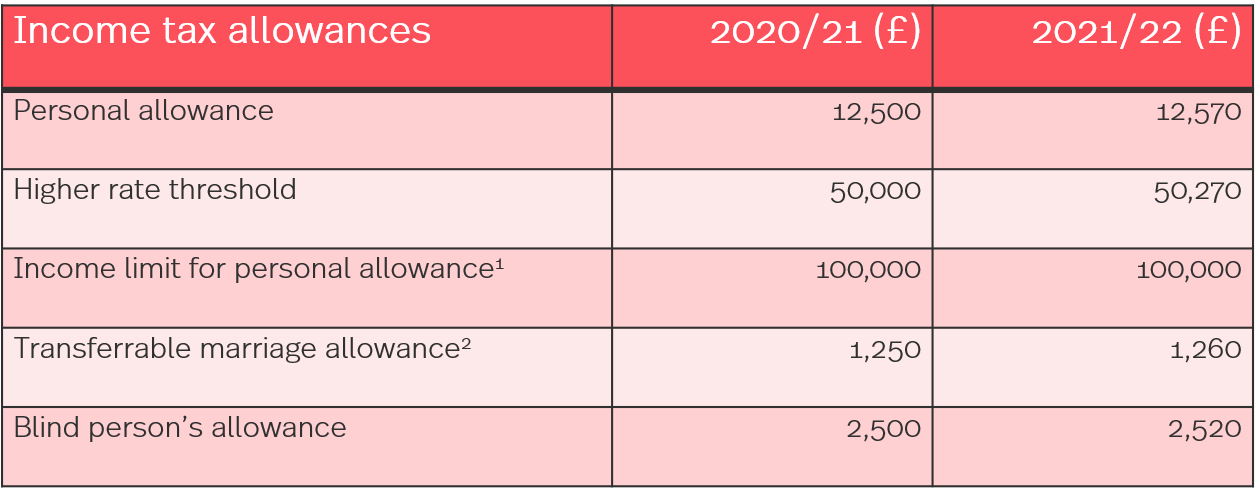

1 The individual’s personal allowance is reduced where their income is above this limit. The allowance is reduced by £1 for every £2 above the limit.

2 The marriage allowance cannot be transferred to a recipient spouse liable to income tax at the higher or additional rate.

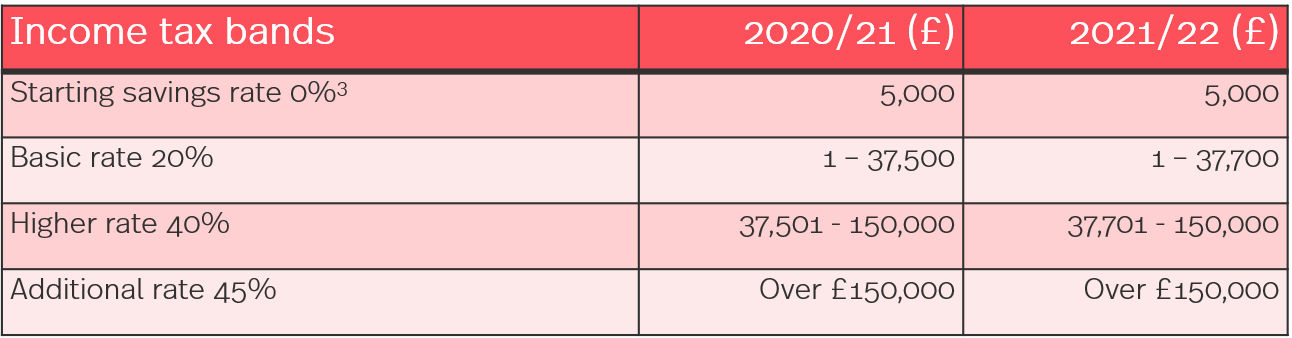

3 If non-savings taxable income exceeds the starting rate limit, the starting savings rate will not apply to savings income.

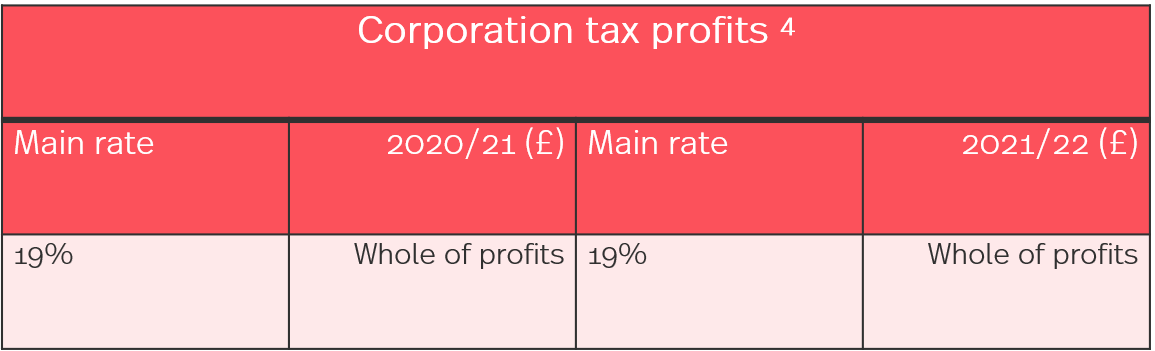

4 From 01 April 2023, the main rate of corporation tax will increase to 25% for profits in excess of £250,000. From the same date, a ‘small profits rate’ of 19% will apply to profits up to £50,000. For businesses with profits between £50,000 and £250,000, corporation tax will be charged at the main rate, subject to marginal relief provisions which will provide a gradual increase in the effective corporation tax rate.

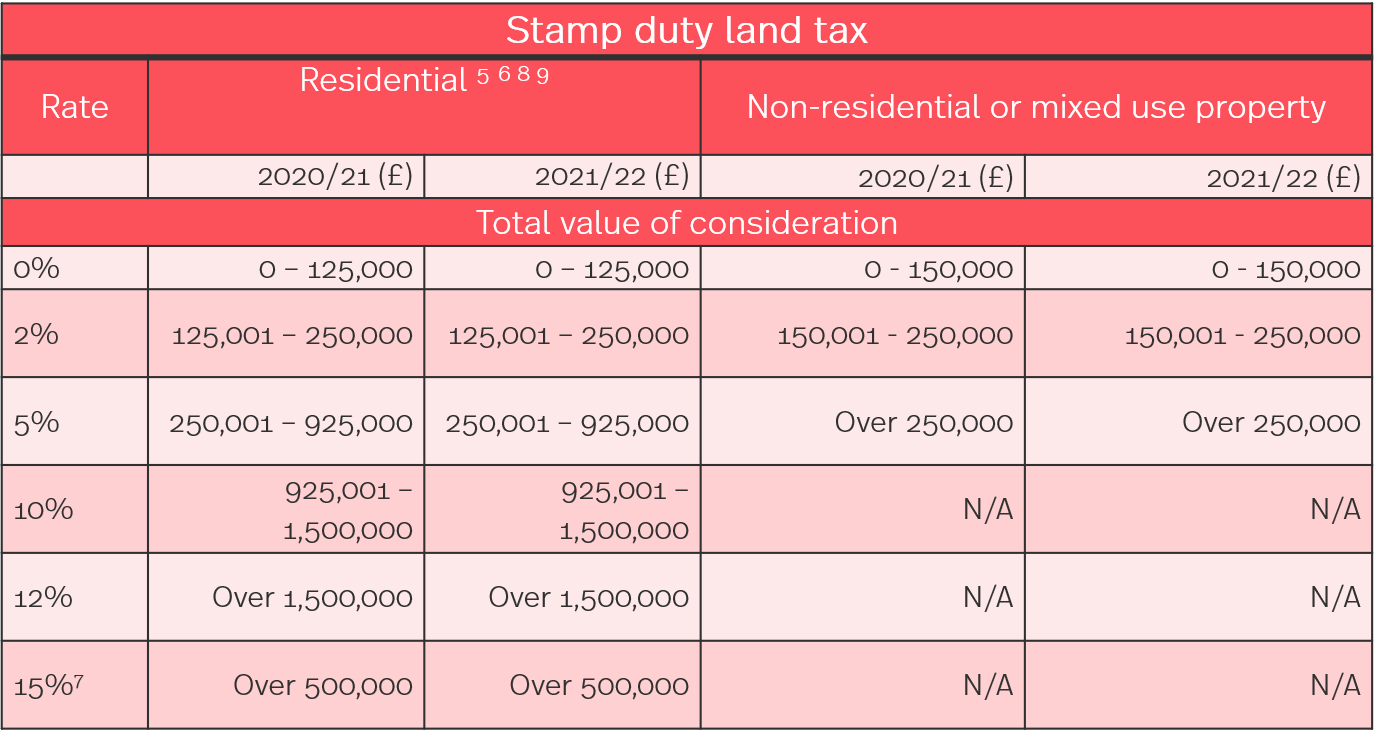

5 Stamp duty land tax is charged at a rate of 3% above the current stamp duty land tax residential rates from 01 April 2016 on purchases by individuals of additional residential properties (such as second homes and buy-to-let properties), and by non-natural persons (companies, partnerships including companies or collective investment schemes) of a residential property, even if they do not own another residential property.

6 For purchases by first-time buyers of property worth £500,000 or less from 22 November 2017, the stamp duty land tax rate for a property valued £0 – 300,000 is 0% and for a property valued £300,001 – 500,000 is 0% on the consideration up to £300,000 and 5% on the remainder.

7 The 15% rate applies to certain acquisitions of residential property by “non-natural persons” (a company, a partnership including a company or a collective investment scheme).

8 A 2% surcharge will take effect from 01 April 2021 on non-UK residents purchasing residential property in England and Northern Ireland.

9 A temporary reduction in SDLT applies to purchases of residential property between 8 July 2020 and 30 June 2021 pursuant to which a purchaser only pays SDLT on amounts above £500,000. Between 01 July 2021 and 30 September 2021, purchasers of residential property will only be required to pay SDLT on amounts above £250,000. SDLT will return to the above stated rates from 01 October 2021. This relief temporarily replaces the relief for first-time buyers (see note 6 above).

This document (and any information accessed through links in this document) is provided for information purposes only and does not constitute legal advice. Professional legal advice should be obtained before taking or refraining from any action as a result of the contents of this document.

If you have any questions, contact a member of the HMRC tax rates and allowances for 2021/22 team for assistance:

07 September 2026Event

Explore how legal privilege applies to tax investigations in Europe

_11zon.jpg?width=380&width=380&format=webply&auto=webp "Article")

07 May 2026 Publication

A round up of the Simmons & Simmons insights on VAT developments over the last month.

30 April 2026 Event

Join us for an informal breakfast to connect and network with fellow tax professionals in a relaxed and welcoming setting.

14 April 2026 Publication

Welcome to our Data Dive podcast series, where we explore the world of Data Centres.

09 April 2026 Publication

A round up of the Simmons & Simmons insights on VAT developments over the last month.