Overview

The Secondary Credit Market Act, which was announced on 29 December 2023, implements the European Directive on Credit Servicers and Credit Purchasers. 1

With a few exceptions, the law will come into force on 30 December 2023 or 1 January 2024.

The Secondary Credit Market Act is intended to simplify the trading of non-performing loans (NPLs) on the secondary market and open up the German market to European trading. It also includes related amendments to existing laws such as the Banking Act, the Act Establishing the Federal Financial Supervisory Authority and the Act on the Recovery and Resolution of Credit Institutions.

Current status of the European NPL market

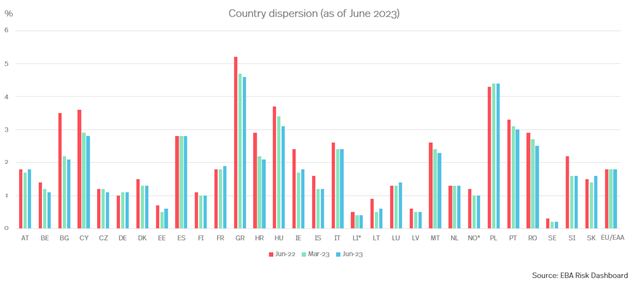

Statistics from the European Banking Authority as of June 2023 continue to show a consistently low NPL ratio of 1.8% in the EU (see details in the country dispersion below). However, it is also pointed out that demand for loans has already slowed significantly due to higher interest rates and weak economic growth and is likely to continue to deteriorate. At the same time, banks have tightened their lending standards in response to the increased macroeconomic uncertainty. Against this background, some countries have already reported an increase in NPL volumes. It should be noted in particular that portfolios with certain assets may deteriorate more quickly due to increased sensitivity to rising interest rates (e.g. consumer loans and property-related exposures).

Essential legal content

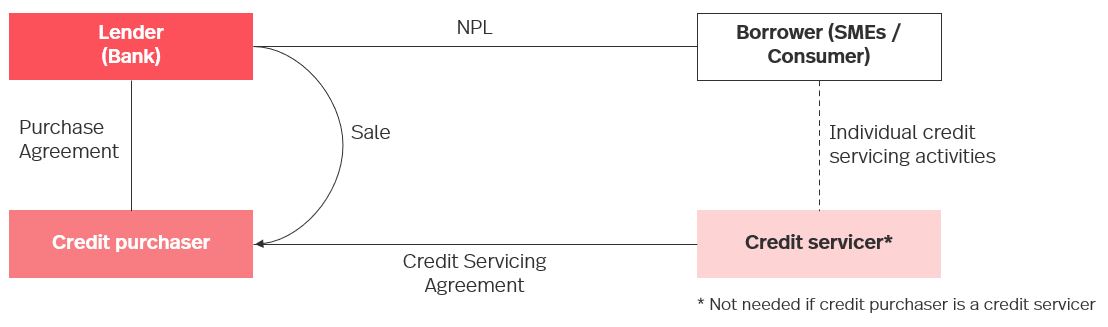

The main content of the Secondary Credit Market Act is the creation of an authorisation procedure for providers of credit services for non-performing loans in Germany as well as access for European providers to this secondary market. Such a credit servicer must be commissioned by the credit purchaser if a credit purchaser has purchased non-performing loans that were previously concluded with a natural person or micro, small and medium-sized enterprises (SMEs).

In addition, the Secondary Credit Market Act provides for extensive information, reporting and organisational obligations for participating credit purchasers, credit institution and credit servicers to safeguard the secondary market. Failure to comply can be sanctioned with withdrawal of the licence, but also with imprisonment or fines. The Federal Financial Supervisory Authority (BaFin) is responsible for supervising the secondary market and implementing the authorisation procedure. In addition, credit purchasers and sellers are also required to provide information to the Bundesbank. The Federal Ministry of Finance is authorised to issue extensive ordinances.

For example, the obligations introduced by the Secondary Credit Market Act include the following:

Provision of information by the credit institution on non-performing loan agreements to potential credit purchasers to assess the economic viability and risks and notification of BaFin and the Bundesbank of the information provided.

Appointment of an intermediary credit servicer by credit purchasers who are not credit servicer to handle the trading of non-performing loan agreements originally concluded with natural persons or SMEs.

If a credit servicer is commissioned, the credit purchaser must inform BaFin and the Bundesbank comprehensively about this servicer.

Credit purchasers must inform BaFin and the Bundesbank every six months about transactions carried out.

Credit service provider must ensure proper business organisation through professionally suitable and reliable managers.

European passport

In addition to extensive obligations for credit purchasers and sellers, the Secondary Credit Market Act also introduces a new register of authorised credit service providers. Finally, a so-called European passport will be introduced to grant access to European providers, which will enable "passporting" both domestically and abroad. This enables providers that are authorised in other EU countries to provide their credit services in Germany without having to hold a German licence. Providers from third countries must appoint a representative from an EU member state. This representative does not have to be an authorised credit service provider. Rather, the representative merely serves as a point of contact for the parties involved and, alongside the credit purchaser, is responsible for the fulfilment of the credit purchaser's obligations under the Secondary Credit Market Act. However, the representative must appoint an additional credit servicer for the purchase of any non-performing loans - i.e. not only loans with natural persons or SMEs as borrower - if the representative is not a credit servicer themselves.

What's next? - Transitional arrangements and tight deadlines

The Secondary Credit Market Act provides for transitional regulations and deadlines from the date of entry into force, some of which trigger an immediate need for action by all parties involved.

In principle, providers that were already providing credit services before the Secondary Credit Market Act came into force may continue to operate in the market without a licence for up to six months after it comes into force. If the intention is to continue operating beyond this date, the providers must notify BaFin within seven weeks of the Secondary Credit Market Act coming into force. At the same time, an application for a licence must be submitted to BaFin within the same period. After the timely submission of that application (i.e., by 16 February 2024 at the latest), BaFin will accept the submission of supporting documents and information by 5 April 2024 at the latest. 2 If an provider that is already active fails to comply with the above in due time, BaFin shall set a separate deadline of four weeks for the provider to make up the notification or submit the documents required for the granting of a licence.

Conclusion

In some cases, the Secondary Credit Market Act leads to an immediate need for action on the part of the respective parties involved. Credit purchasers should inform themselves immediately about the new regulatory environment with regard to the purchase of non-performing loans in Germany in order to avoid liability traps. Credit service providers are required to obtain a licence within the specified deadlines. It remains to be seen whether the Secondary Credit Market Act will actually bring an easier access to a regulated secondary market for non-performing loan agreements. What is certain, however, is that the large number of extensive regulations will create a considerable need for advice. For German credit service providers, the tight deadline for obtaining the necessary licence from BaFin is particularly important. Particularly in view of the introduction of a European passport, it remains to be seen whether future activities in the market in a less regulated member state may not be a recommendable alternative to a German licence.

1 Directive (EU) 2021/2167 of 24 November 2021.

2 Credit Secondary Market Act: BaFin points out changed submission deadlines

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)