Updates on the QFLP program in China

The QFLP pilot system has been playing an essential role in attracting the inflow of foreign capital and the opening up of the PRC financial markets.

Since the launch of the "Qualified Foreign Limited Partnership/Limited Partnership Enterprise" (QFLP) system first in 2010, the QFLP pilot system has been playing an essential role in attracting the inflow of foreign capital and the opening up of the PRC financial markets.

Unlike the traditional foreign direct investment model, foreign asset management institutions can establish foreign-invested equity investment management enterprises onshore (usually referred to as "Pilot Management Enterprises", together with the pilot fund usually referred to as "Pilot Enterprises") through the QFLP pilot system. Pilot Management Enterprises can establish equity investment funds or other closed-end private funds in the form of private placement. Such funds can accept domestic and overseas investors. Moreover, after obtaining the pilot qualification and foreign exchange settlement quota, the funds can flexibly convert the foreign investors' foreign exchange capital into Renminbi to participate in private equity investment in China. Not to mention that domestic private equity fund managers can also take advantage of the flexibility of the QFLP pilot system to directly accept subscriptions from foreign investors who invest through foreign currencies into their RMB funds.

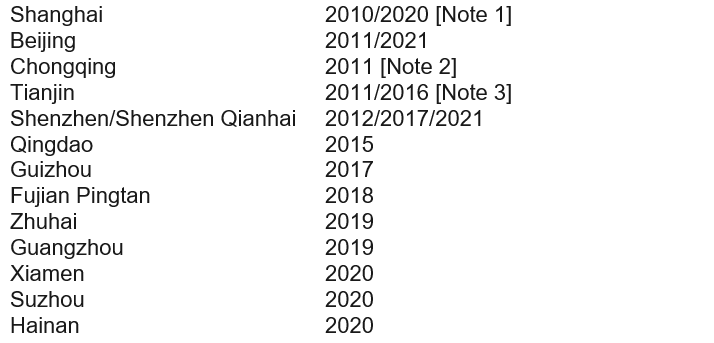

Since the first release of the QFLP pilot system in 2010 (implemented since 2011) in Shanghai, more than ten pilot cities in China have introduced their own QFLP pilot systems. On 28 April 2021, ten years since the introduction of the Beijing QFLP pilot system, the Beijing Financial Supervision and Administration Bureau (in Chinese北京市金融监督管理局) and the Beijing Market Supervision Administration Bureau (in Chinese北京市市场监督管理局) officially issued the "Interim Measures on the Commencement of the Pilot Program of Qualified Foreign Limited Partnership in the Municipality" (in Chinese《关于本市开展合格境外有限合伙人试点的暂行办法》). Throughout the last decade, a series of remarkable changes in China's foreign direct investment and capital account foreign exchange regulatory system, as well as the continuous improvement of the private equity fund industry regulations, have been observed. This article aims to provide a high-level review of the development of the QFLP pilot system as well as to briefly introduce the policy highlights of the Beijing QFLP pilot system.

Note 1: Shanghai, as the first batch of cities to launch the QFLP pilot system, has announced its plan to expand the management model and investment scope of QFLP Pilot Enterprises in 2020.

Note 2: Chongqing is among the first batch of cities to launch the QFLP pilot system. Nonetheless, since the key regulation "Opinions of the Chongqing Municipality on Commencing Pilot Work for Foreign-invested Equity Investment Enterprises" (Yubanfa [2011] No. 132) (in Chinese《重庆市关于开展外商投资股权投资企业试点工作的意见》(渝办发[2011]132号)) was abolished in 2015, no follow-up policies have been issued.

Note 3: Although Tianjin's key QFLP pilot program has ceased to be implemented in 2016, it still continues to accept applications for the establishment of Pilot Enterprises, and from a regulatory and practical perspective, relatively fixed and standardised rules have been formed.

In the following sections, we are going to review the development of the QFLP pilot policies being implemented in the past ten years, introduce the highlights of the Beijing QFLP system, and make some preliminary suggestions to both domestic and foreign managers on how to make the best out of the new policies and new plan.

1. Development of the QFLP pilot system in the past ten years

Looking at the different QFLP pilot systems in various regions in the past ten years, we observe the following commonalities with regard to their regulatory policies.

Emphasis on the size of pilot fund raised, and a progressive relaxation on the capital requirements of Pilot Management Enterprises

The early QFLP pilot policies set requirements not only on the size of the registered capital/subscribed capital, but also on the capital paid-in schedule, of the Pilot Management Enterprises. Nonetheless, with the advancement and reform of the foreign direct investment and the "at will" foreign exchange settlement system for capital accounts, these pilot cities have gradually relaxed their requirements and instead adopted other criteria that focus more on the qualifications (such as financial licenses and management teams, more of which would be discussed below) to improve the quality of the Pilot Management Enterprises.

That being said, a pilot fund, as an investment entity, is usually required to ensure that the size of its raised fund reaches the required threshold. This is to make sure the pilot fund is already beginning to take shape in utilizing its capital the moment the fund is being established.

Imposition of conditions on qualifications for Pilot Management Enterprises

For a successful asset management institution, its industry experience and core management team are of paramount importance, which we believe are even more critical than its size of capital. In this regard, almost all QFLP pilot policies across the nation have imposed conditions on the qualifications of the shareholders or partners of a Pilot Management Enterprise. Investors of Pilot Management Enterprises usually need to obtain a financial business license issued by the financial regulatory authority of the country or region in which they are located, and/or has a minimum AUM or net assets.

In addition, Pilot Management Enterprises usually need to have the necessary senior management personnel onboard. A more commonly imposed standard is that a management enterprise would need to have at least two senior management personnel with a certain number of years of experience in the private equity investment sector.

Restrictions on the investment scope of the pilot fund

For the earlier QFLP pilot policies, foreign funds, upon completing the requisite foreign exchange, are usually required to be used only for investing into the equity of non-listed companies. This reflects the primary market investment attribute of QFLP. The policies strictly prohibit foreign exchange funds from participating in transactions such as secondary market stock transactions, real estate transactions, and financial derivatives transactions. For some pilot policies, pilot funds are also prohibited from investing through the fund-of-funds (FOF) model.

With the gradual formation of the domestic private equity investment business model, the regulatory rationale has gradually been clearer. Since 2020, in terms of rulemaking and the implementations of the regulations, the investment scope of QFLP Pilot Enterprises in areas such as Shanghai, Tianjin, Hainan and Shenzhen has been greatly expanded. The investment business of Pilot Enterprises can be expanded to transactions such as PIPE deals that contain both primary and secondary features (in Chinese "一级半市场"), where the investment targets can also include mezzanine, private placement bonds, non-performing assets, etc., and gradually with more and more Pilot Enterprises gaining regulatory approvals to invest in the market as FOFs.

2. Innovations with the introduction of the new regime in Beijing

Unlike the systems in other pilot cities across the country, the QFLP pilot system introduced by Beijing this time has undoubtedly been at the forefront in terms of its ability in learning from the policies in other regions. The following policy highlights are noteworthy for the industry.

Expansion of investment scope

Shenzhen, Shanghai, Hainan and Tianjin have all already begun to gradually relax restrictions on the investment scope of pilot funds. The Beijing QFLP pilot policy expressly states that, under its regime, investments made by the pilot funds would be subject to the foreign investment negative list, but apart from that, the pilot funds can, on the condition that existing industry practices and current regulatory practices are being observed, invest in the following types of investment targets:

Transactions with both primary and secondary features.

This type of transactions includes non-public issues and trading of ordinary shares of listed companies (including private issues of new shares, block trading, negotiated transfers, etc.), preference shares that can be converted into ordinary shares, debt-to-equity swaps and convertible bonds. Here, the pilot funds can participate in share allotments as original shareholders of the listed companies.

Based on the existing industry practices, in addition to the traditional investment of the equity of unlisted companies, private equity investment funds are usually allowed in their fund contract to conduct stock investments to achieve privately negotiated transactions. From a regulatory perspective, the AMAC has also recognized that transactions such as private placement and negotiated transfers, can be included in the investment scope of equity investment funds. Therefore, this rule can enable pilot funds to better implement their investment objectives.

Mezzanine investment, private placement bonds, non-performing assets.

Both domestic and foreign private equity fund managers will seek to expand their asset management categories and establish a more extensive product line once their asset size reaches a certain level. Mezzanines, private placement bonds and non-performing assets, as important asset classes, have always been the focus of major asset management institutions, as well as investment hotspots in the domestic market. From a regulatory point of view, since 2020, various policies have been encouraging foreign financial institutions to enter into the domestic market, especially in areas such as the disposal of non-performing assets. By utilising the Beijing pilot system, foreign asset management institutions can implement diversified investment strategies under a more relaxed policy environment.

Domestic private investment funds

Both from a capital perspective and an asset perspective, it would be difficult for foreign asset management institutions to ignore the growth potential of the Chinese market. The Beijing regime allows pilot funds to invest into private investment funds, and provides channels for foreign asset management institutions to substantially participate in China's domestic asset allocation, FOF investment and PE secondary market transactions.

Of course, the policy also reiterates clearly that the investment scope of the pilot funds would be subject to the restrictions imposed by industry regulations on the investment scope of private equity funds. As an investment channel for foreign funds to participate in the domestic market, pilot funds are naturally not allowed to participate in any overseas direct investments.

Flexible management and operation

Under the Beijing QFLP pilot system, Pilot Enterprises can have a more flexible investment management structure, with high flexibility in the legal form of the fund, quota, and fundraising:

The pilot fund can be formed as a contractual fund, which allows more flexibility to asset management institutions in choosing the legal form of the fund, where they can take into proper consideration of their business needs and the types of their investment targets.

Quota granted to the Pilot Management Enterprises instead of the pilot funds. Pilot Management Enterprises can flexibly adjust the size of a single fund and allocate the quota among multiple pilot funds sponsored by them. Managers can more flexibly formulate fundraising plans for their multiple funds, and hence be able to respond quickly to investment opportunities and significantly minimise the administrative costs resulting from repeated application and approval processes.

Through the model whereby QFLP funds are set up for foreign investors by domestic fund managers (in Chinese "内管外模式"), domestic private equity investment fund management enterprises can accept foreign investors more easily.

Optimisation of the regulatory model

The Beijing QFLP pilot system stipulates that the Pilot Enterprises would need to go through the registration and filing procedures only when the AMAC rules require. The current prevailing self-regulatory practices indicate that, if the fundraising behaviour occurs overseas completely, or if there is no external fundraising behaviour, then there is no need to file with the AMAC. In fact, prior to this, similar relaxations have been observed in other regions, such as Tianjin and Shanghai. This time, Beijing is following the same approach and is not imposing additional registration and filing obligations on Pilot Enterprises beyond the self-regulations of the industry. As a consequence, asset management institutions can avoid excessive compliance costs due to unnecessary registration and filing obligations.

In the current ongoing trend of financial liberalisation and constant innovation of foreign investment management policies, it is important for asset management institutions to consider both asset-side and capital-side demands and to seek a balance among different commercial considerations.

_11zon.jpg?crop=300,495&format=webply&auto=webp)