On 28 December 2019, the Standing Committee of the 13th National People's Congress approved the revision of the Securities Law of the People's Republic of China (New Securities Law), which has been officially implemented since 1 March 2020.

Widely regarded as a milestone in China’s capital market reform, the implementation of the New Securities Law is expected to have a substantial impact on China’s capital market and all its participants. The revision of the 2014 Securities Law by the legislators, and subsequent approval and implementation of the New Securities Law by the Standing Committee of the 13th National People's Congress, required more than four years to complete. Under the New Securities Law, 166 provisions have been updated from the previous 2014 Securities Law and 24 new provisions have been added. The New Securities Law now consists of 14 chapters, which outline the regulatory details for the issue and trading of securities, takeovers of listed companies, information disclosure and investor protection.

The New Securities Law establishes the legal basis for the adoption of a registration-based IPO system across the entire A-share market and provides tougher punishments for malpractice and insider trading. It has also enhanced the information disclosure mechanism and offers better protection for public investors.

The New Securities Law defines Securities to encompass stocks, corporate bonds, depository receipts ABS, asset management products, and when trading on an exchange, government bonds and securities investment funds, as well as other securities with similar nature. It remains to be seen whether the scope of “other securities with similar nature” will, by reference to the practice of certain overseas markets, be expanded to include ETFs and individual stock options, and the main constituent stocks of companies listed on NEEQ (ie China’s OTC board).

This article will specifically summarise the key changes brought by the New Securities Law to the existing share disclosure regime, and analyse the practical implications of the New Securities Law to domestic and foreign asset managers and their business related to the A-share market.

1. Key changes to the share disclosure obligations/requirements

We have included a diagram below to better illustrate the current position after the implementation of the New Securities Law.

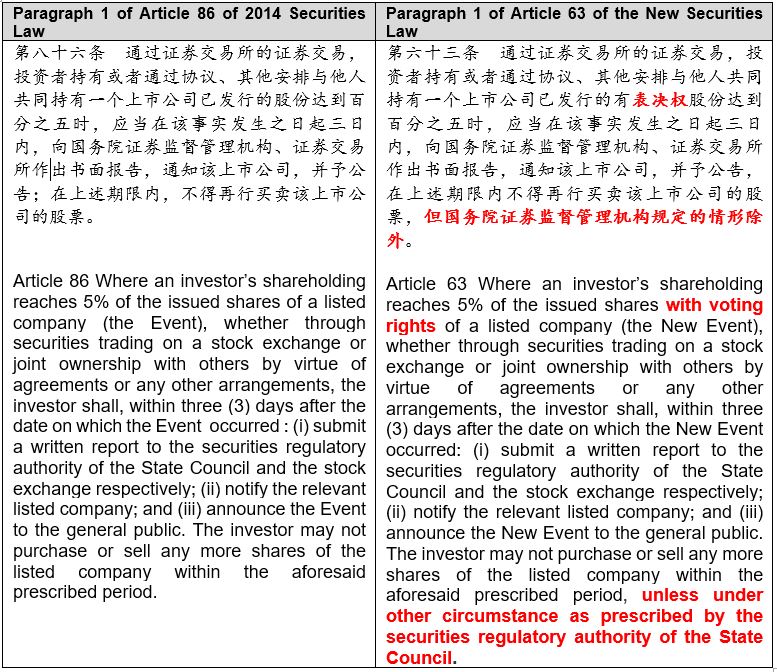

1.1. Where an investor’s shareholding first reaches 5%

The table below compares the changes made by legislators to the original provisions of the 2014 Securities Laws. The changes concern the type of situation upon which an investor’s shareholding first reaches 5%.

As shown in the table comparison, the two major amendments to the relevant rules on share disclosure under the New Securities Law are as follows:

- The 2014 Securities Law uses the shareholding percentage as the basis for calculating share disclosure obligations. The New Securities Law clearly states that the basis for calculating the share disclosure obligation is based on "shares with voting rights";

- Under the New Securities Law, the Chinese Securities Regulatory Committee (the CSRC) has granted certain exemptions in determining the information disclosure obligations and trading restriction period imposed on any investor holding 5% or more of shares in a listed company.

Under the New Securities Law, the term “shares with voting rights” does not simply refer to the shares registered under the investor’s name with statutory voting rights, but also includes those shares in which investors can exercise control over or under the investor’s disposal.

The New Securities Law appears to adopt a similar position as, and aligns with, the relevant rules in the Measures for the Administration of the Takeover of Listed Companies issued by CSRC on October 23, 2014, where interest of parties acting in concert will be aggregated.

With respect to the CSRC’s discretion to grant any exemptions, under the existing rules, multiple retail funds managed by the same fund management company are not required to be aggregated provided that each retail fund holds no less than 5% of the shares of the listed company in question. Such exemption is now consistent with this Article 63 of the New Securities Law. It is questionable whether the same exemption would be offered by CSRC to private securities funds and the industry is looking forward to CSRC giving more clarity on this issue.

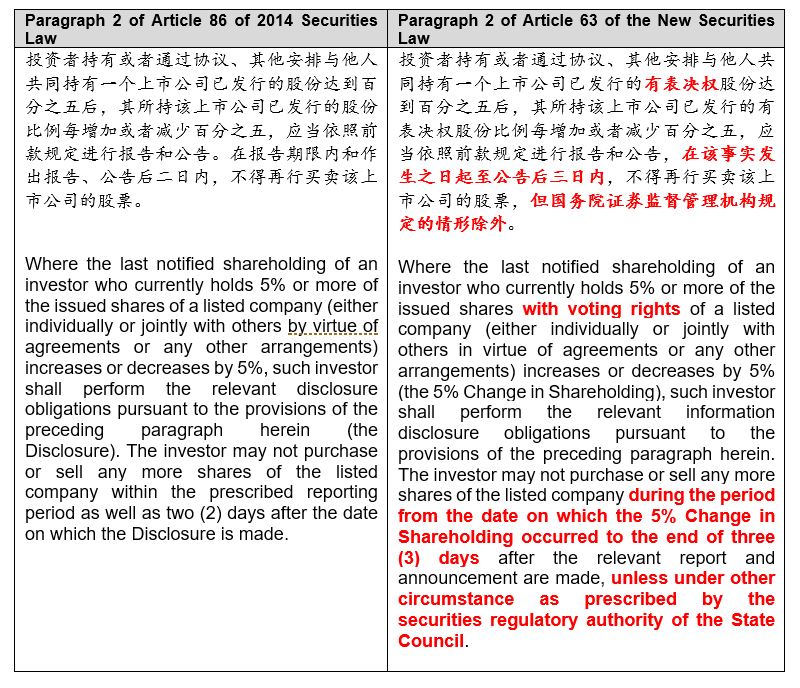

1.2 Where an investor’s shareholding increases or decreases by every 5% from the last notified shareholding

In September 2019, the CSRC clarified in its response to a query raised with respect to Article 13 of the Takeover Measures that the number of days of the reporting period refers to “a trading day” of stock exchange instead of a “calendar day”. Therefore, the number of days of the reporting period should be calculated from the next day when the relevant report is made. One may therefore expect the same principles to be applied to this change made by the New Securities Law.

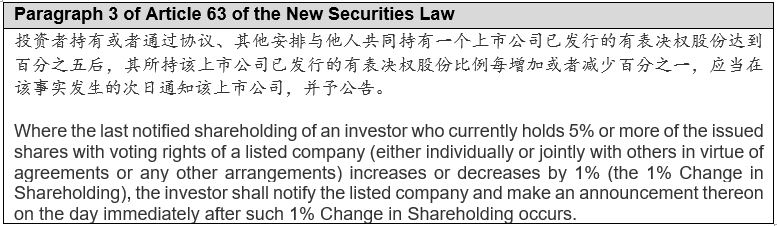

1.3 Where an investor’s shareholding increases or decreases by every 1% from the last notified shareholding

Paragraph 3 of Article 63 is a new requirement added by the New Securities Law. It should be noted that Paragraph 3 of Article 63 only requires investors to fulfill their disclosure obligations; it does not prevent investors from trading the shares of the listed company during the above reporting period.

We note that this is another change that the New Securities Law has absorbed from relevant exchange rules of Shanghai and Shenzhen. Prior to this new requirement, in April of 2019, stock exchanges in Shanghai and Shenzhen issued a consultation paper of updated disclosure rules, ie the Guidelines for the Information Disclosure of the Acquisition of Listed Companies and the Change of Equity Interests (《上市公司收购及股份权益变动信息披露业务指引》) (Guidelines for the Information Disclosure). The Guidelines for the Information Disclosure require that, if the shareholding exceeds 5%, then every 1% upward or downward fluctuation requires further disclosure.

This new requirement is also aligned with international standards.

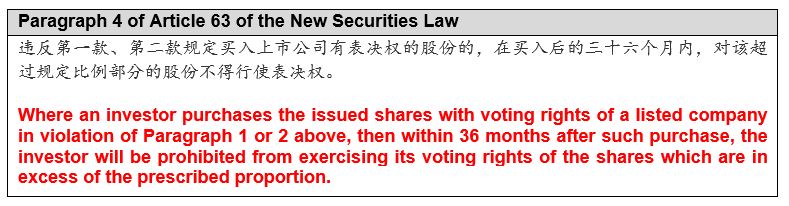

1.4 Consequences of non-compliance with suspension of trading after a share disclosure obligation is triggered

Another requirement imposed by the New Securities Law is in relation to the consequences of non-compliance with trading restrictions imposed by the CSRC during the reporting period. Compared to the 2014 Securities Law, the New Securities Law imposes a substantially tougher penalty for any violation of the foregoing provision. The penalties and the period of prohibition on the exercise of voting rights imposed by the New Securities Law are more stringent than those in the Takeover Measures.

For a long time, one of the best tactics for a listed company to fight against "barbarians at the gate" in the event of a hostile takeover, is to restrict the voting rights of the acquirer on the grounds of violation of share disclosure obligation. However, such protection could only be achieved through prolonged litigation and court rulings. With the implementation of the New Securities Law, the acquirer and the listed company will no longer need to resolve such dispute through litigation. If an investor does not follow proper share disclosure procedures, then within 36 months after purchasing such shares, such investor will be prohibited from exercising its voting rights of the shares which are in excess of the prescribed proportion.

2. Extraterritorial Jurisdiction

Article 78 of the New Securities Law suggests that the New Securities Law has certain extraterritorial jurisdictions, as the issuance or trading activities that occurred in an exchange or over the counter outside of the territory of PRC may trigger the relevant reporting obligations under the New Securities Law. Article 78 of the New Securities Law stipulates: “Where the securities are publicly issued or traded at the same time within or outside the territory of China, the information disclosed abroad by the obligor shall be disclosed at the same time within the territory of China.” We believe this is intended to capture certain disclosure issues in relation to the holding of a company that is dual listed in multiple jurisdictions, for example, A-share and H-share markets, where the holdings should be aggregated as a general principle.

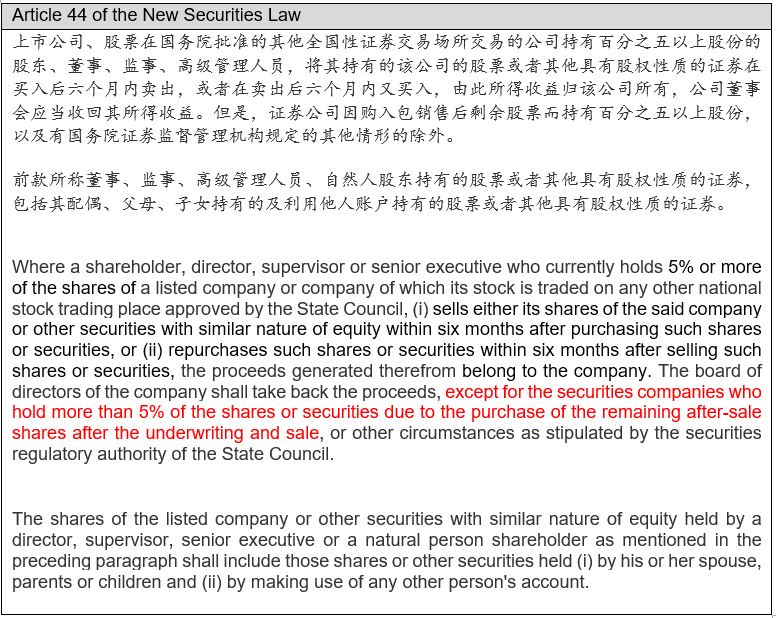

3. Short Swing Profit Rules

Under the 2014 Securities Law, shareholders holding more than 5% (among others) are subject to the short swing profit rules. According to the relevant rules, any person whose shareholding in a Chinese listed company exceeds 5% (or any other threshold imposed by the specific stock exchange) must disgorge profits generated from share transactions in said company so long as the sale (or purchase) occurs within six (6) months after the preceding transaction with a reverse direction. Proceeds generated from such transactions are incorporated into the profits of the listed company. Such restrictions on short swing profit are incorporated by the legislator to establish, prevent or deter insider trading.

Under the New Securities Law, the scope of application of such restrictions is expanded from shares or “other securities with similar nature of equity” to the shares held by the spouse, parents or children of the said shareholder, director, supervisor, and senior executive. This expansion indicates that the investors are now required to more heavily scrutinize the relationships of the shareholders, directors, supervisors and senior executives and exert greater effort in ensuring that the aforementioned restrictions are complied with.

Therefore, when making investments, investors shall prevent short swing profit not only for shares but also for other securities with similar nature of equity as a result of the expansion of the scope of “Securities”.

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)